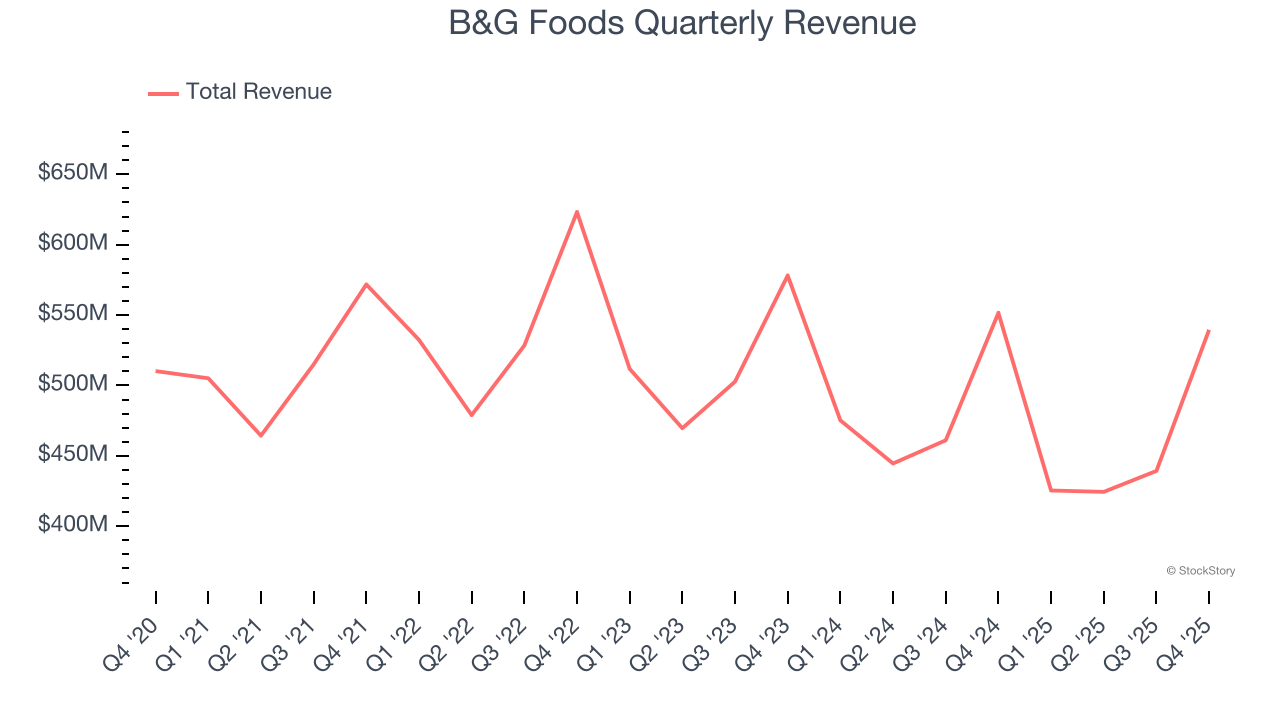

Packaged foods company B&G Foods (NYSE: BGS) announced better-than-expected revenue in Q4 CY2025, but sales fell by 2.2% year on year to $539.6 million. On the other hand, the company’s full-year revenue guidance of $1.68 billion at the midpoint came in 5.6% below analysts’ estimates. Its non-GAAP profit of $0.28 per share was 7.1% below analysts’ consensus estimates.

Is now the time to buy B&G Foods? Find out by accessing our full research report, it’s free.

B&G Foods (BGS) Q4 CY2025 Highlights:

- Revenue: $539.6 million vs analyst estimates of $536.1 million (2.2% year-on-year decline, 0.6% beat)

- Adjusted EPS: $0.28 vs analyst expectations of $0.30 (7.1% miss)

- Adjusted EBITDA: $84.68 million vs analyst estimates of $87.2 million (15.7% margin, 2.9% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.60 at the midpoint, beating analyst estimates by 17.5%

- EBITDA guidance for the upcoming financial year 2026 is $270 million at the midpoint, above analyst estimates of $265.3 million

- Operating Margin: 5.2%, up from -46.6% in the same quarter last year

- Sales Volumes were flat year on year (2.2% in the same quarter last year)

- Market Capitalization: $414.3 million

Commenting on the results, Casey Keller, President and Chief Executive Officer of B&G Foods, stated, “B&G Foods’ fourth quarter earnings were largely in line with expectations, with core business trends showing further year-over-year improvement to date during the first quarter of 2026. B&G Foods also announced yesterday the divestiture of the Green Giant U.S. frozen vegetable business—representing a significant milestone in our ongoing effort to divest brands and product lines that are non-core to B&G Foods’ long-term strategy, sharpen our focus and reduce long-term debt.”

Company Overview

Started as a small grocery store in New York City, B&G Foods (NYSE: BGS) is an American packaged foods company with a diverse portfolio of more than 50 brands.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.83 billion in revenue over the past 12 months, B&G Foods is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, B&G Foods struggled to generate demand over the last three years. Its sales dropped by 5.4% annually despite selling a similar number of units each year. We’ll explore what this means in the "Volume Growth" section.

This quarter, B&G Foods’s revenue fell by 2.2% year on year to $539.6 million but beat Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to decline by 4.2% over the next 12 months, similar to its three-year rate. it’s hard to get excited about a company that is struggling with demand.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

B&G Foods’s quarterly sales volumes have, on average, stayed about the same over the last two years. This stability is normal because the quantity demanded for consumer staples products typically doesn’t see much volatility.

In B&G Foods’s Q4 2025, year on year sales volumes were flat. This result was more or less in line with its historical levels.

Key Takeaways from B&G Foods’s Q4 Results

It was encouraging to see B&G Foods beat analysts’ gross margin expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded up 4.5% to $5.30 immediately after reporting.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).