Texas Capital Bank has been treading water for the past six months, recording a small return of 4.1% while holding steady at $90.55.

Is there a buying opportunity in Texas Capital Bank, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Texas Capital Bank Not Exciting?

We're sitting this one out for now. Here are three reasons we avoid TCBI and a stock we'd rather own.

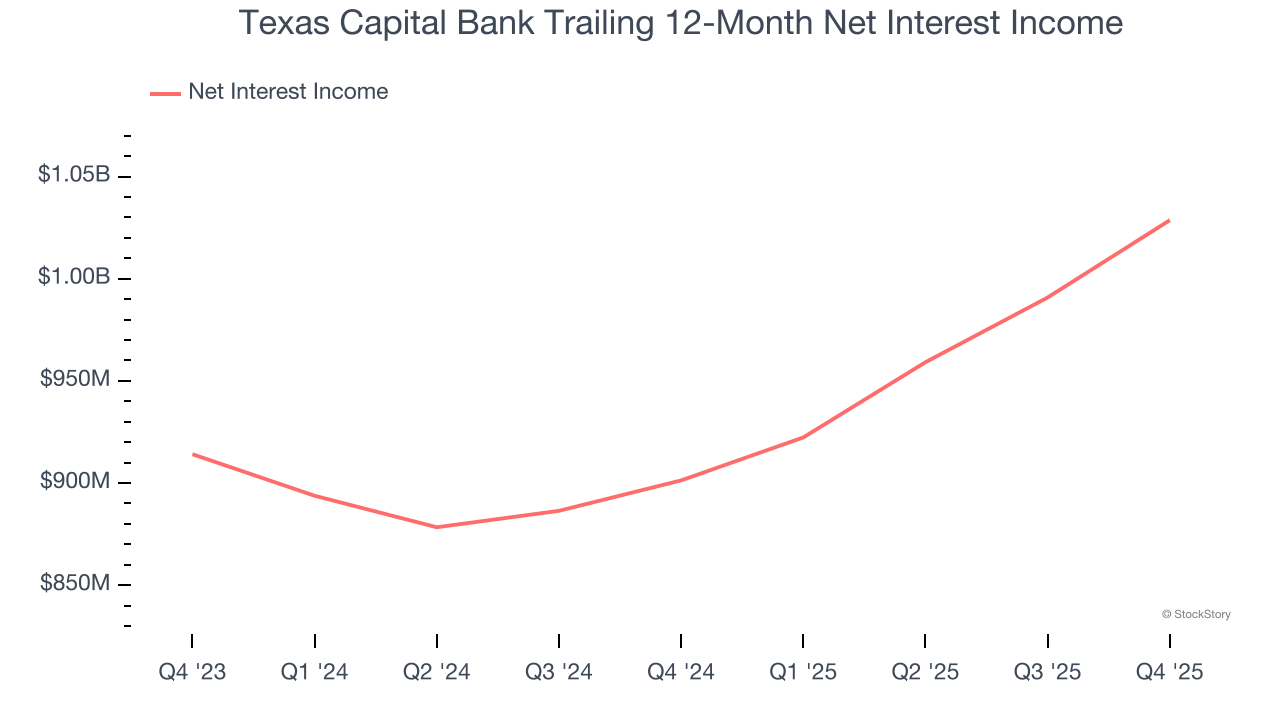

1. Net Interest Income Points to Soft Demand

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

Texas Capital Bank’s net interest income has grown at a 3.9% annualized rate over the last five years, much worse than the broader banking industry and in line with its total revenue. Its growth was driven by an increase in its net interest margin, which represents how much a bank earns in relation to its outstanding loans, as its loan book shrank throughout that period.

2. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Texas Capital Bank’s net interest income to rise by 4.1%, a slight deceleration versus its 6.1% annualized growth for the past two years.

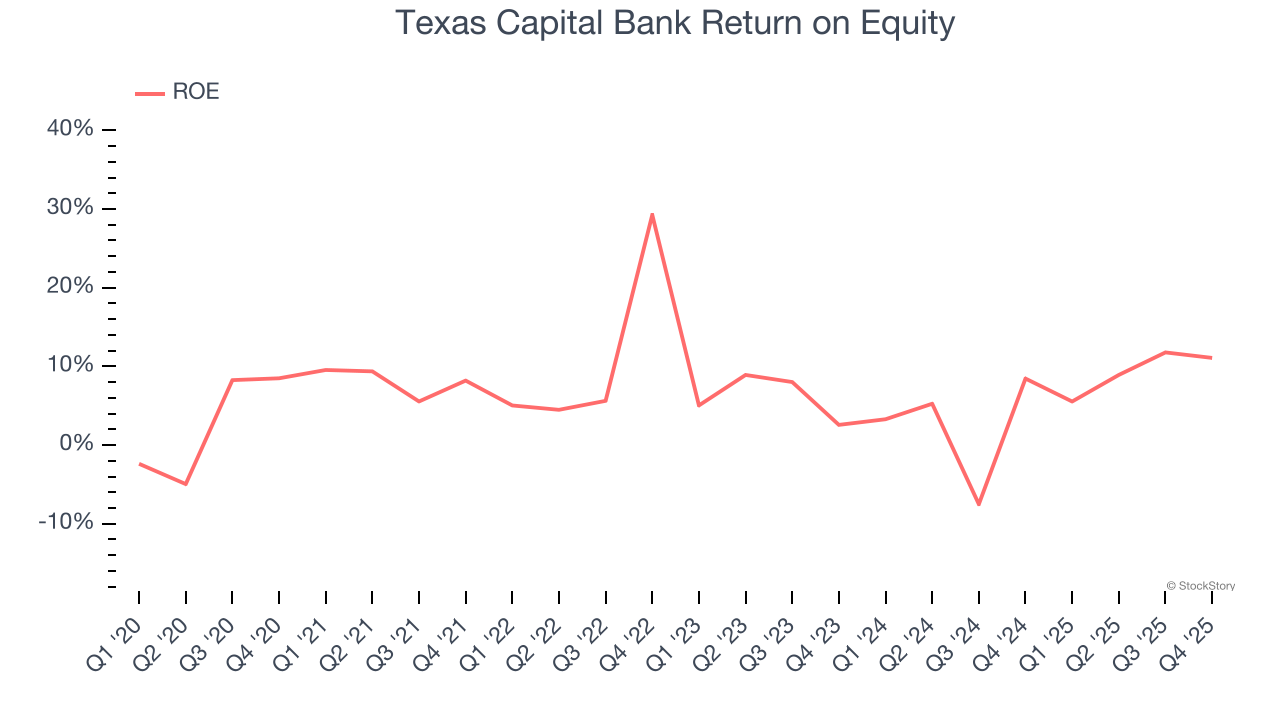

3. Previous Growth Initiatives Haven’t Impressed

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Texas Capital Bank has averaged an ROE of 7.4%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

Final Judgment

Texas Capital Bank isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at 1.1× forward P/B (or $90.55 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d recommend looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Texas Capital Bank

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.