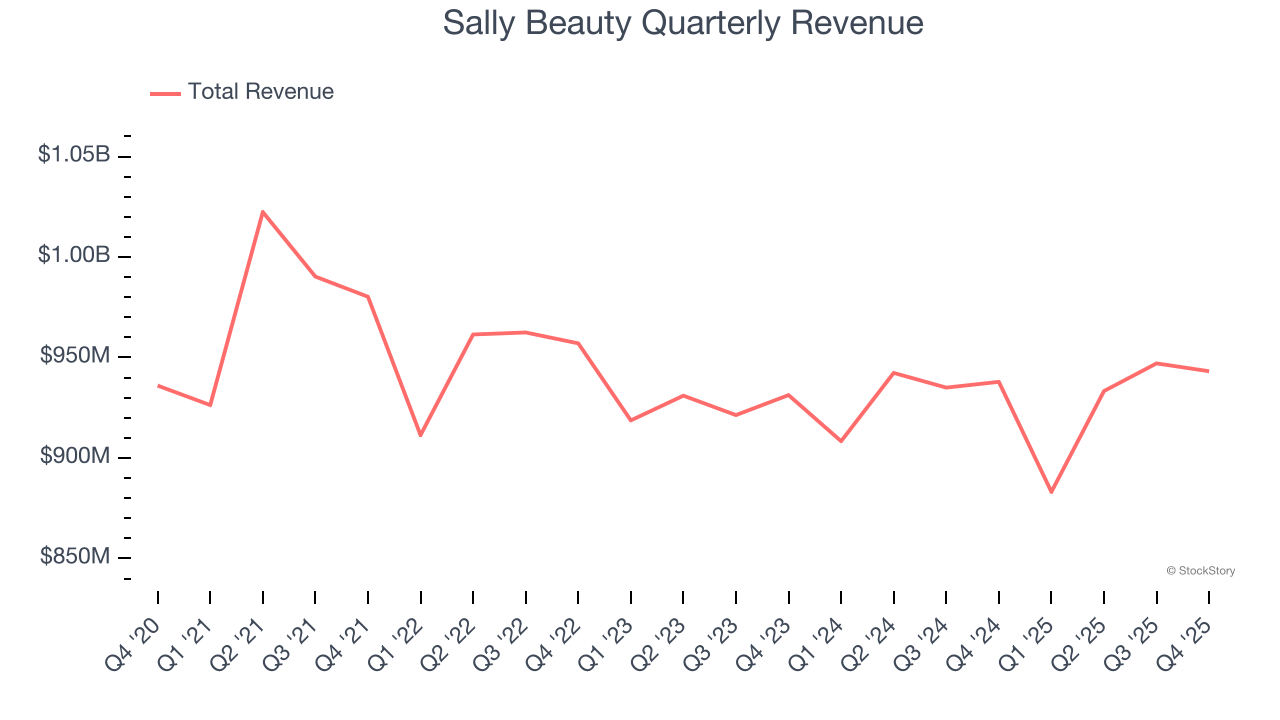

Beauty supply retailer Sally Beauty (NYSE: SBH) met Wall Street’s revenue expectations in Q4 CY2025, but sales were flat year on year at $943.2 million. The company expects next quarter’s revenue to be around $900 million, close to analysts’ estimates. Its non-GAAP profit of $0.48 per share was 3.4% above analysts’ consensus estimates.

Is now the time to buy Sally Beauty? Find out by accessing our full research report, it’s free.

Sally Beauty (SBH) Q4 CY2025 Highlights:

- Revenue: $943.2 million vs analyst estimates of $940.5 million (flat year on year, in line)

- Adjusted EPS: $0.48 vs analyst estimates of $0.46 (3.4% beat)

- Adjusted EBITDA: $111 million vs analyst estimates of $108.7 million (11.8% margin, 2.2% beat)

- The company reconfirmed its revenue guidance for the full year of $3.74 billion at the midpoint

- Management slightly raised its full-year Adjusted EPS guidance to $2.06 at the midpoint

- Operating Margin: 8.1%, down from 10.7% in the same quarter last year

- Free Cash Flow Margin: 6.1%, up from 1.4% in the same quarter last year

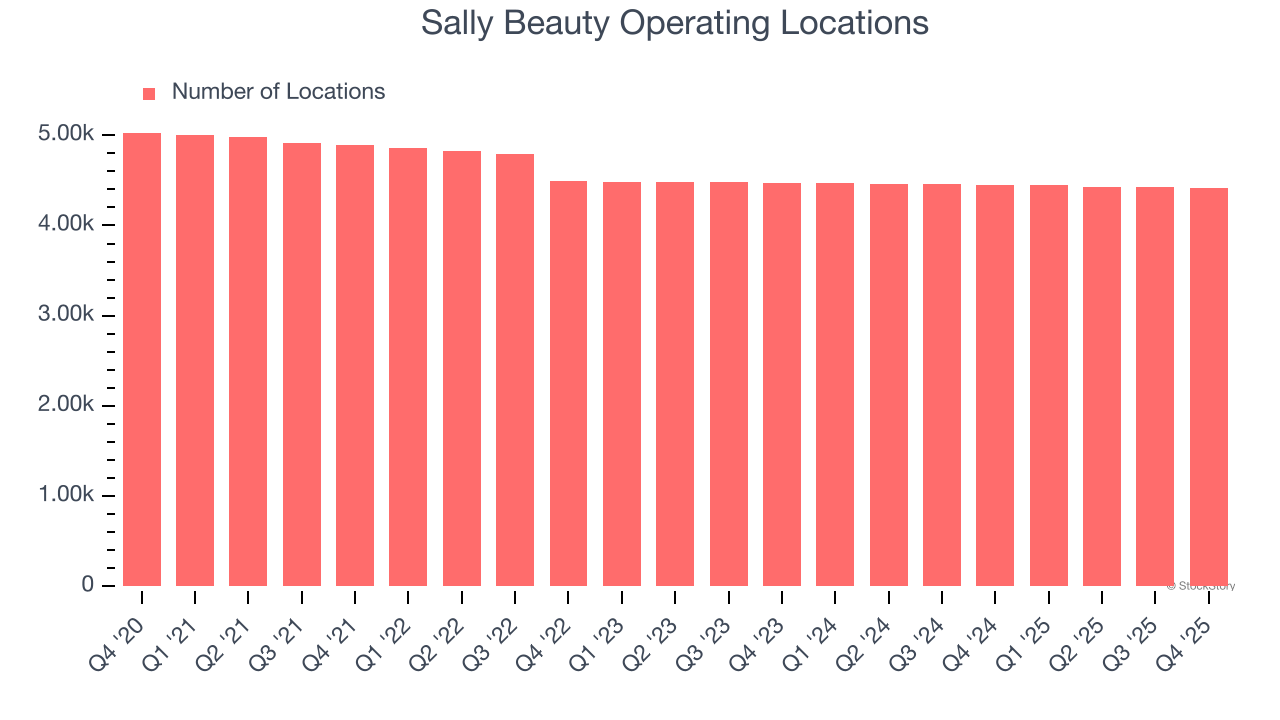

- Locations: 4,415 at quarter end, down from 4,453 in the same quarter last year

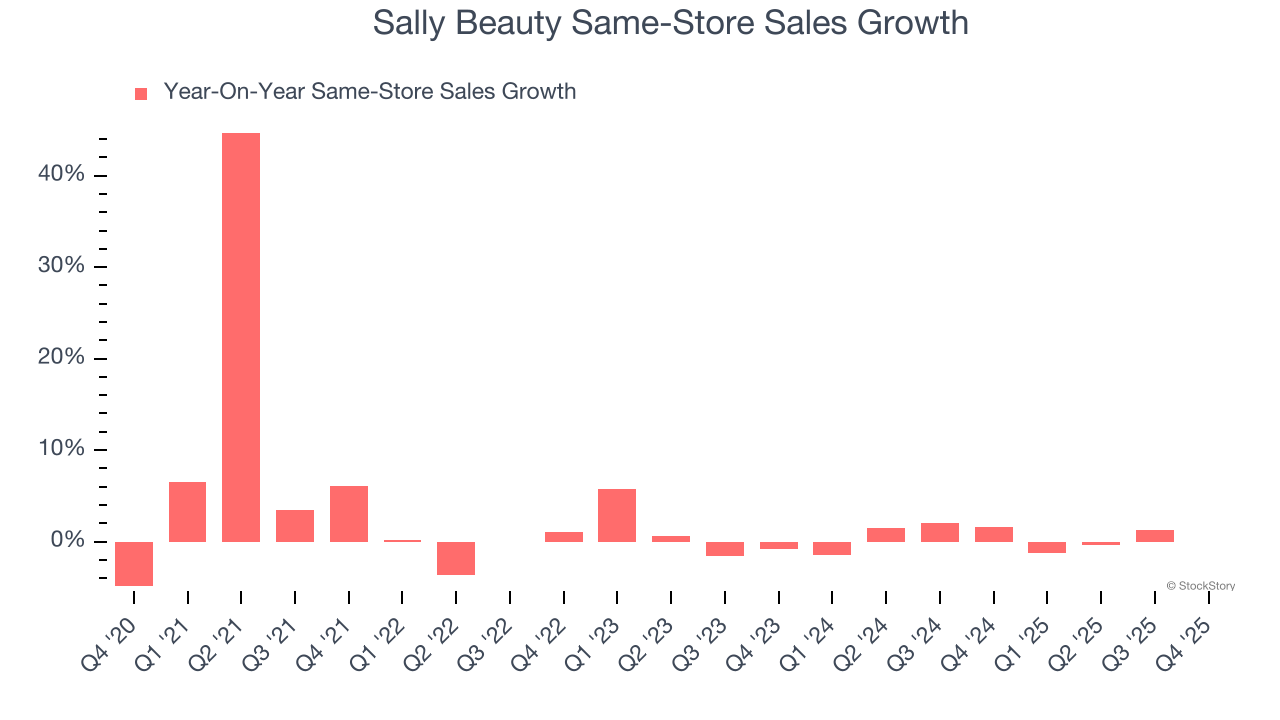

- Same-Store Sales were flat year on year (1.6% in the same quarter last year)

- Market Capitalization: $1.58 billion

Company Overview

Catering to both everyday consumers as well as salon professionals, Sally Beauty (NYSE: SBH) is a retailer that sells salon-quality beauty products such as makeup and haircare products.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $3.71 billion in revenue over the past 12 months, Sally Beauty is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Sally Beauty struggled to increase demand as its $3.71 billion of sales for the trailing 12 months was close to its revenue three years ago. This was mainly because it didn’t open many new stores.

This quarter, Sally Beauty’s $943.2 million of revenue was flat year on year and in line with Wall Street’s estimates. Company management is currently guiding for a 1.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.4% over the next 12 months. Although this projection implies its newer products will fuel better top-line performance, it is still below average for the sector.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Sally Beauty operated 4,415 locations in the latest quarter, and over the last two years, has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Sally Beauty’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Sally Beauty starts opening new stores to artificially boost revenue growth.

In the latest quarter, Sally Beauty’s year on year same-store sales were flat. This performance was more or less in line with its historical levels.

Key Takeaways from Sally Beauty’s Q4 Results

It was encouraging to see Sally Beauty beat analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed. Overall, this quarter could have been better. The stock traded down 2.1% to $15.82 immediately following the results.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).