Since February 2021, the S&P 500 has delivered a total return of 75.7%. But one standout stock has nearly doubled the market - over the past five years, Genco has surged 147% to $20.17 per share. Its momentum hasn’t stopped as it’s also gained 20.3% in the last six months, beating the S&P by 11.9%.

Is now the time to buy Genco, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Genco Will Underperform?

Despite the momentum, we're swiping left on Genco for now. Here are three reasons there are better opportunities than GNK and a stock we'd rather own.

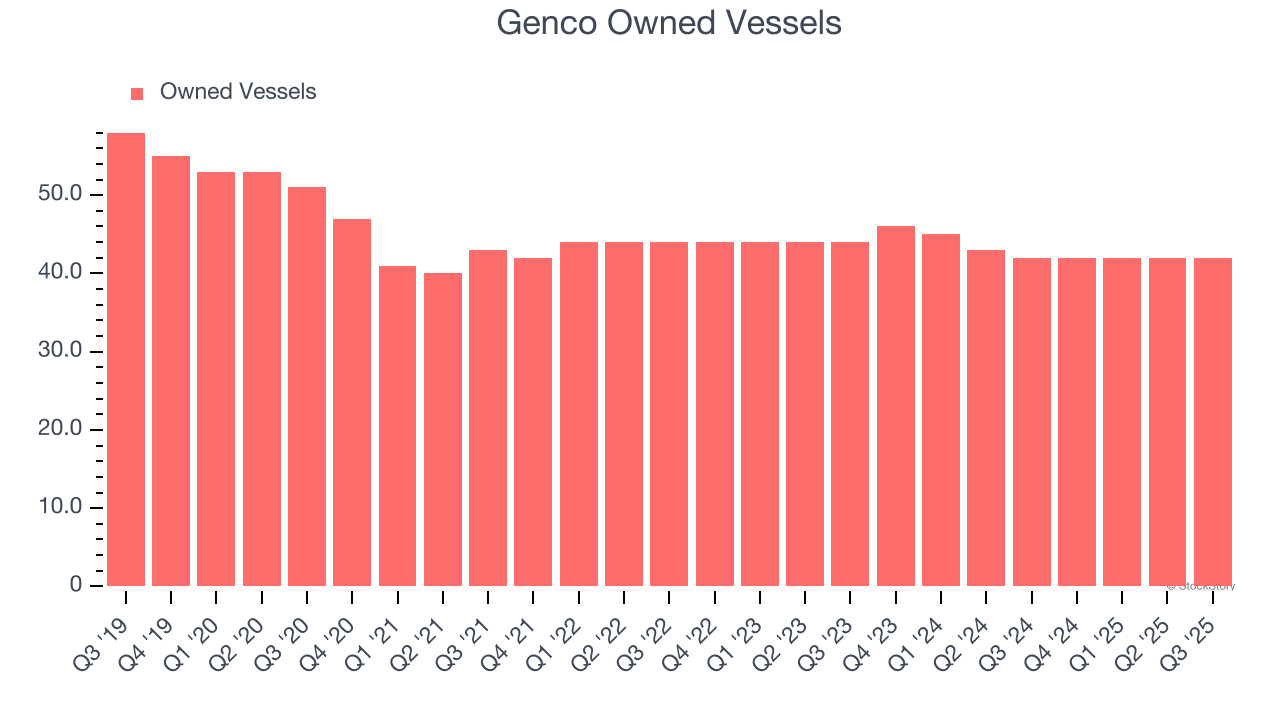

1. Decline in owned vessels Points to Weak Demand

Revenue growth can be broken down into changes in price and volume (for companies like Genco, our preferred volume metric is owned vessels). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Genco’s owned vessels came in at 42 in the latest quarter, and over the last two years, averaged 2.2% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Genco might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

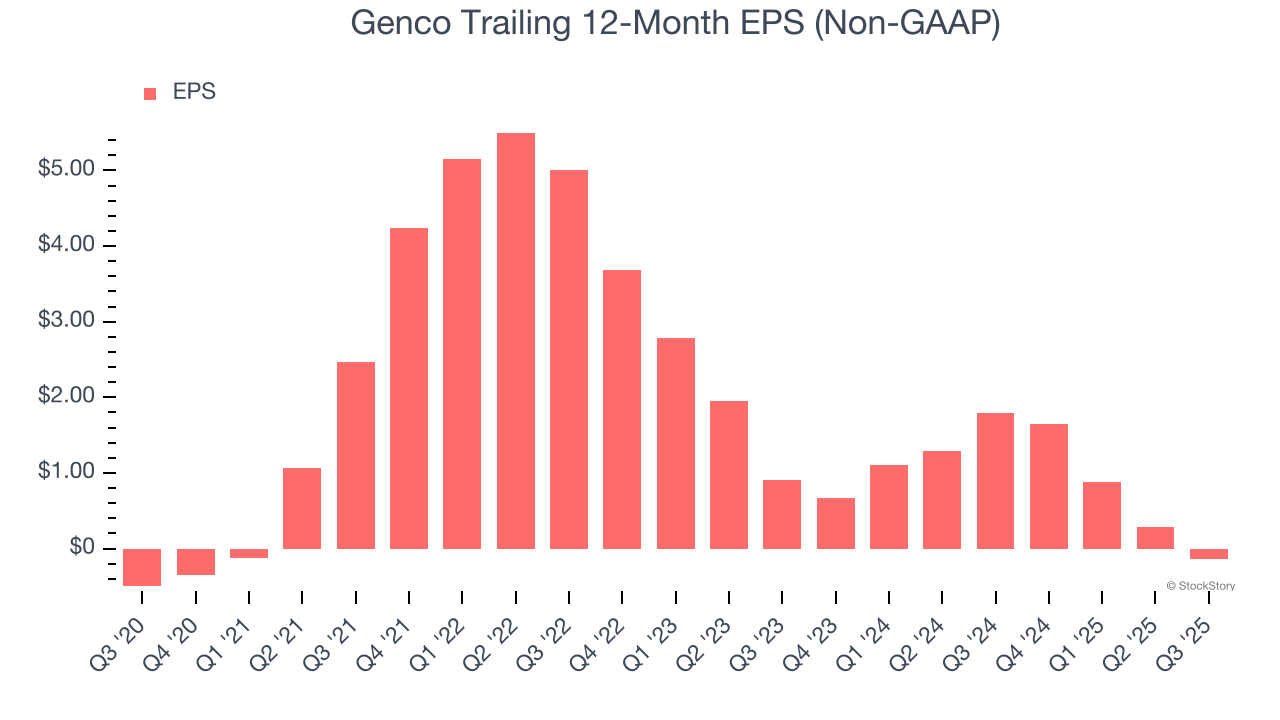

2. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Genco, its EPS declined by more than its revenue over the last two years, dropping 46.6%. This tells us the company struggled to adjust to shrinking demand.

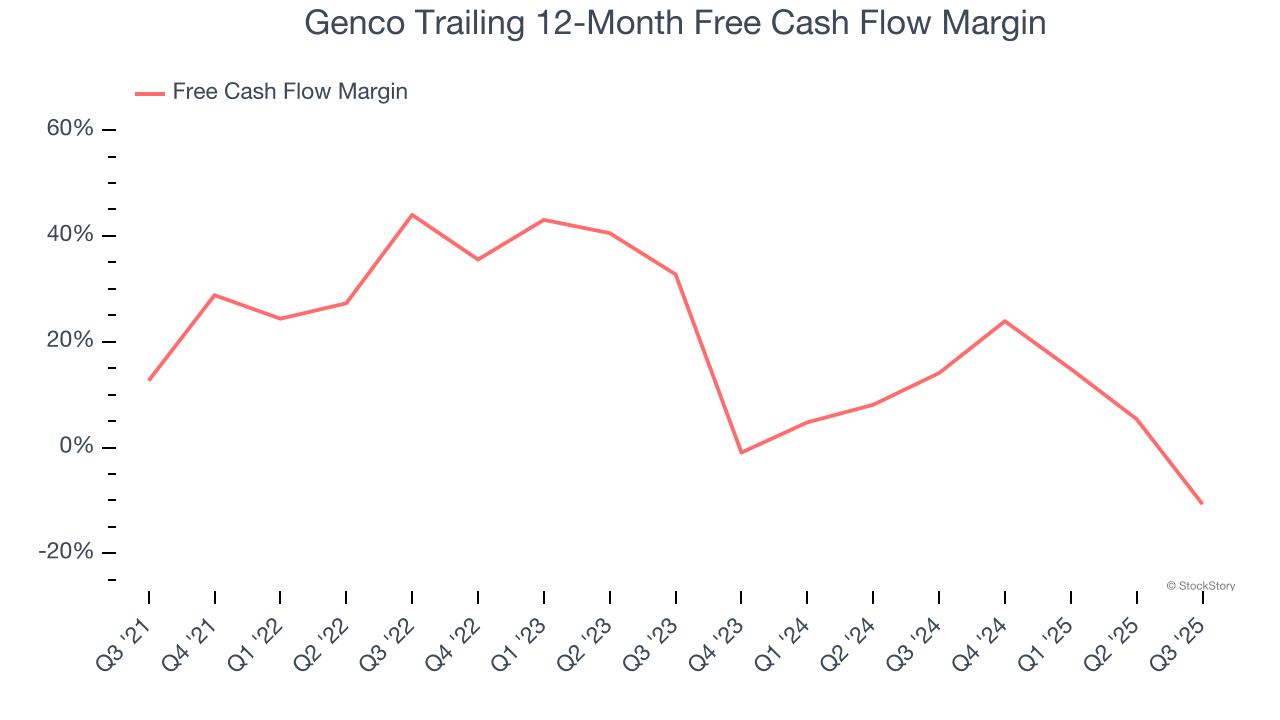

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Genco’s margin dropped by 23.4 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Genco’s free cash flow margin for the trailing 12 months was negative 10.7%.

Final Judgment

Genco doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 13.5× forward P/E (or $20.17 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are more exciting stocks to buy at the moment. We’d suggest looking at one of our top digital advertising picks.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.