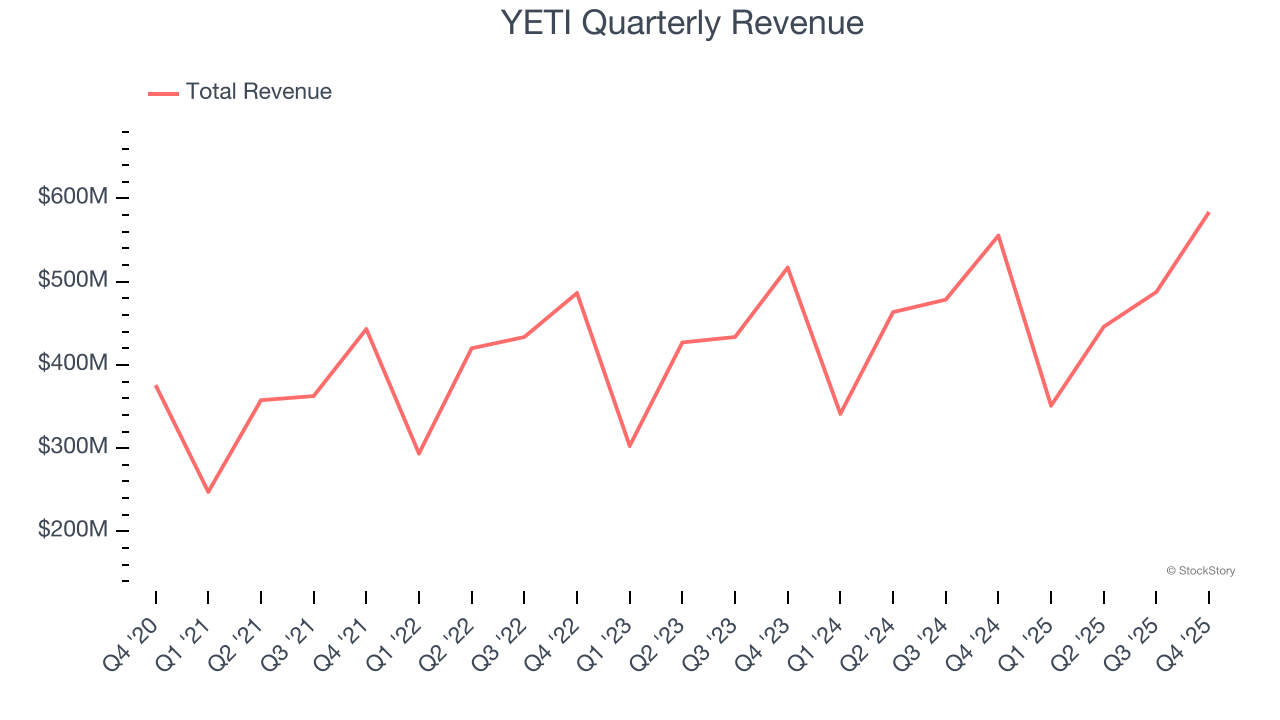

Outdoor lifestyle products brand (NYSE: YETI) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 5.1% year on year to $583.7 million. Its non-GAAP profit of $0.92 per share was 4.1% above analysts’ consensus estimates.

Is now the time to buy YETI? Find out by accessing our full research report, it’s free.

YETI (YETI) Q4 CY2025 Highlights:

- Revenue: $583.7 million vs analyst estimates of $582.5 million (5.1% year-on-year growth, in line)

- Adjusted EPS: $0.92 vs analyst estimates of $0.88 (4.1% beat)

- Adjusted EBITDA: $137.3 million vs analyst estimates of $106 million (23.5% margin, 29.5% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $2.80 at the midpoint, missing analyst estimates by 1.8%

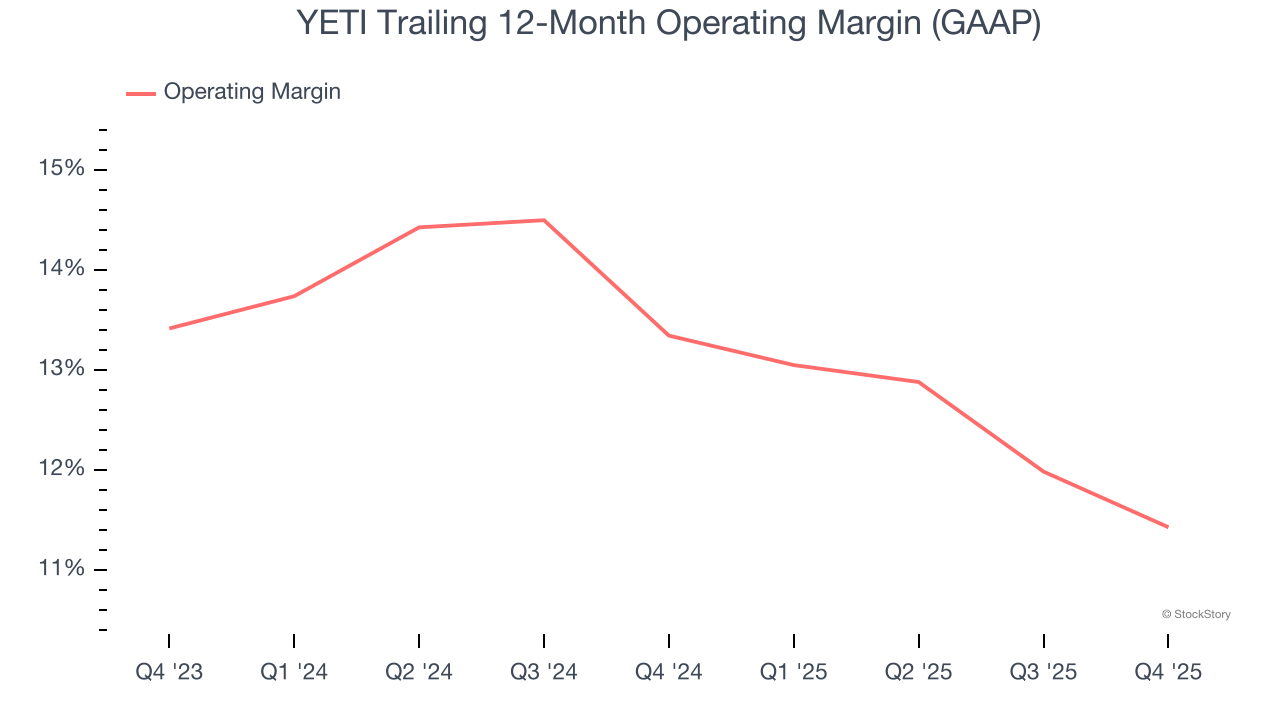

- Operating Margin: 12.9%, down from 14.9% in the same quarter last year

- Free Cash Flow Margin: 27.8%, down from 38.7% in the same quarter last year

- Market Capitalization: $3.85 billion

Matt Reintjes, President and Chief Executive Officer, commented, “Q4 was our strongest quarter of the year as the YETI brand continued to build momentum. We’re seeing solid demand, our teams are executing with discipline, and the strategy we’ve been building over the last few years is showing through in the numbers and outlook. Across categories and channels, the business is more balanced and resilient than it’s ever been. A big part of that strength comes from the work we’ve done on innovation, strengthening our brand globally, and expanding internationally. These long-term growth pillars are producing tangible results and give us tremendous confidence as we head into 2026. These are the reasons we expect to continue to drive strong top and bottom-line results while generating over $200 million in free cash flow. We are playing in a large global addressable market, which provides us with a significant runway for growth as we continue to bring new consumers to YETI.”

Company Overview

Founded by two brothers from Texas, YETI (NYSE: YETI) specializes in durable outdoor goods including coolers, drinkware, and other gear tailored to adventure enthusiasts.

Revenue Growth

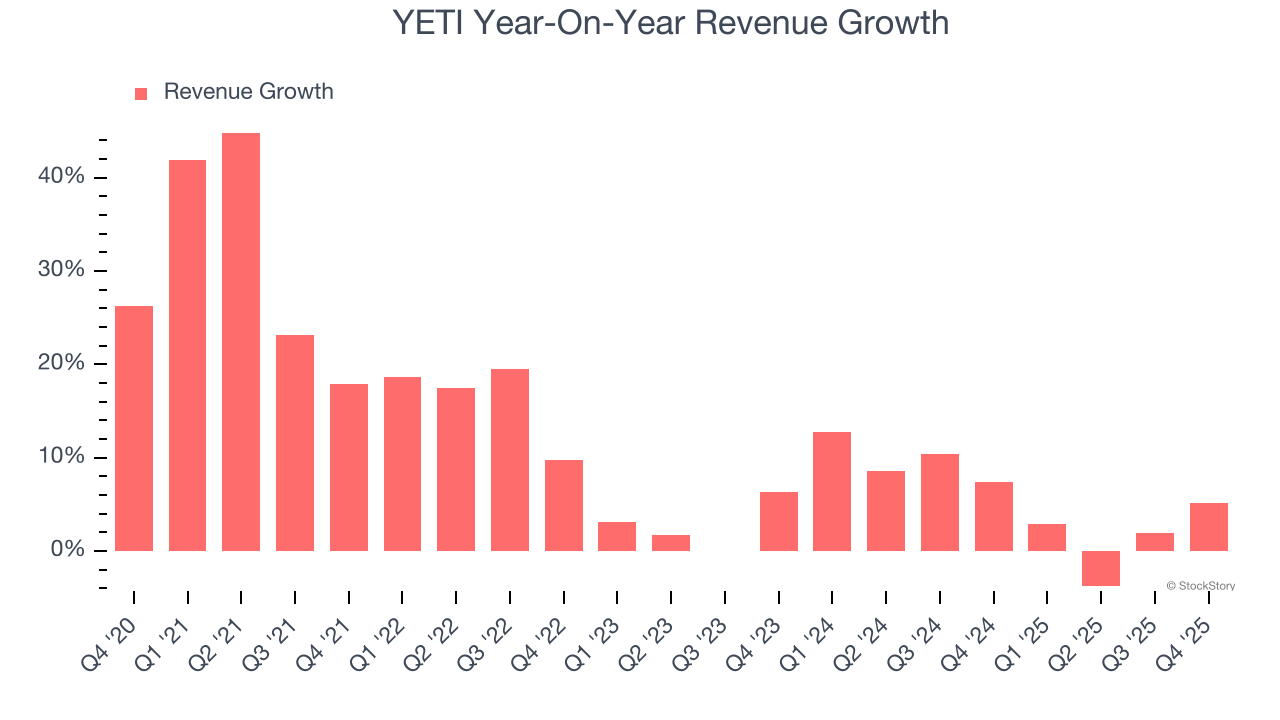

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, YETI grew its sales at a 11.3% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. YETI’s recent performance shows its demand has slowed as its annualized revenue growth of 5.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

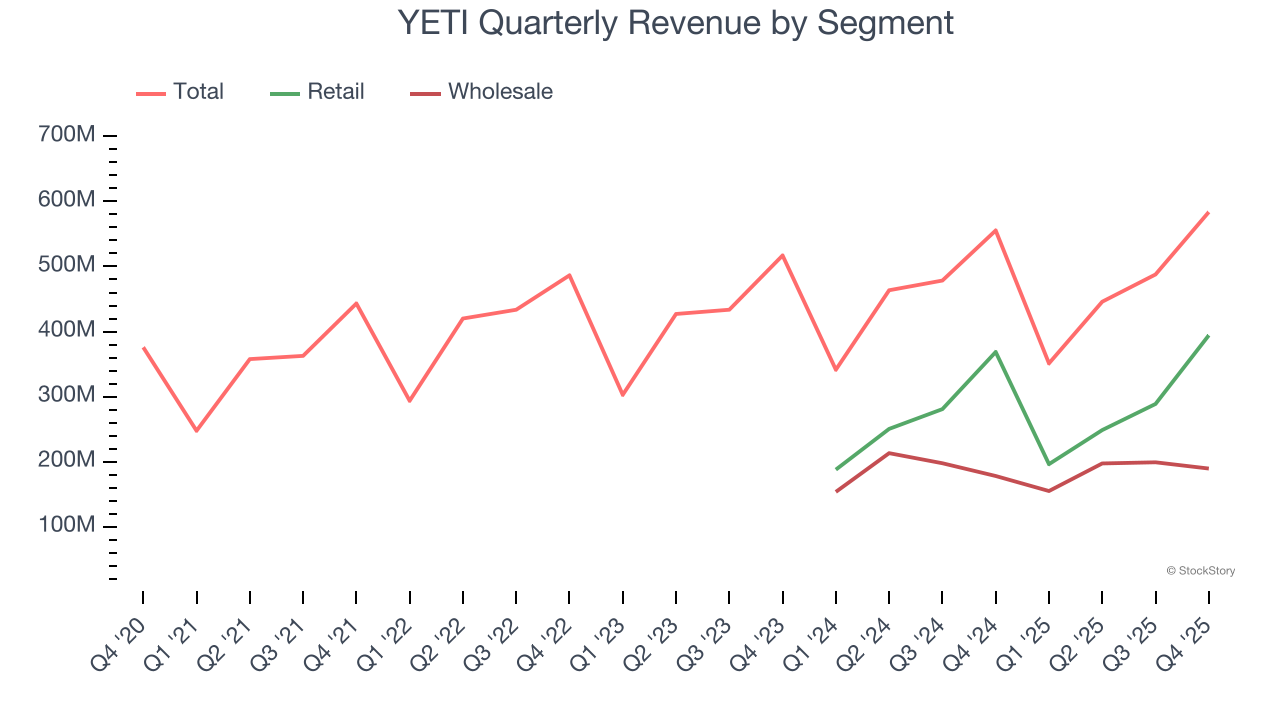

YETI also breaks out the revenue for its most important segments, Retail and Wholesale, which are 67.5% and 32.5% of revenue. Over the last two years, YETI’s Retail revenue (direct sales to customers) averaged 3.4% year-on-year growth while its Wholesale revenue (sales to retailers) was flat.

This quarter, YETI grew its revenue by 5.1% year on year, and its $583.7 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.2% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not lead to better top-line performance yet.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

YETI’s operating margin has been trending down over the last 12 months and averaged 12.4% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, YETI generated an operating margin profit margin of 12.9%, down 1.9 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

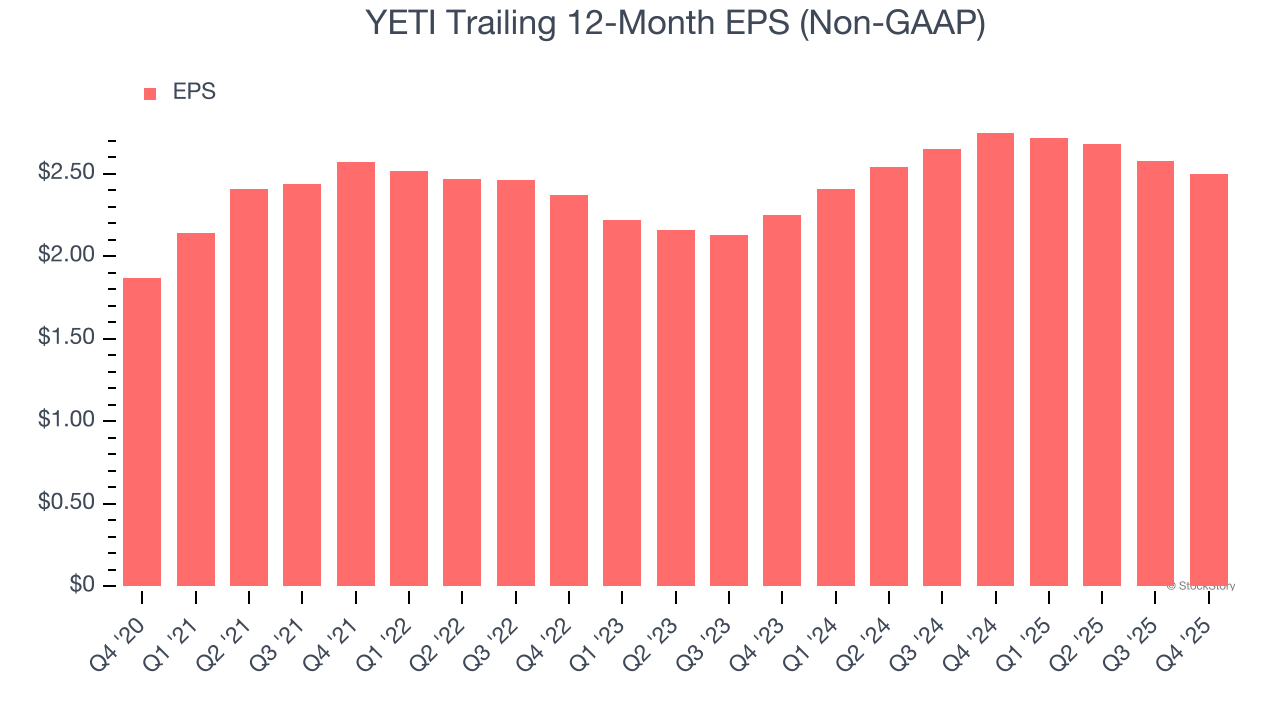

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

YETI’s EPS grew at a weak 6% compounded annual growth rate over the last five years, lower than its 11.3% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q4, YETI reported adjusted EPS of $0.92, down from $1 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 4.1%. Over the next 12 months, Wall Street expects YETI’s full-year EPS of $2.50 to grow 14.2%.

Key Takeaways from YETI’s Q4 Results

We were impressed by how significantly YETI blew past analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed, and this is weighing on shares. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 4% to $47.44 immediately following the results.

So should you invest in YETI right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).