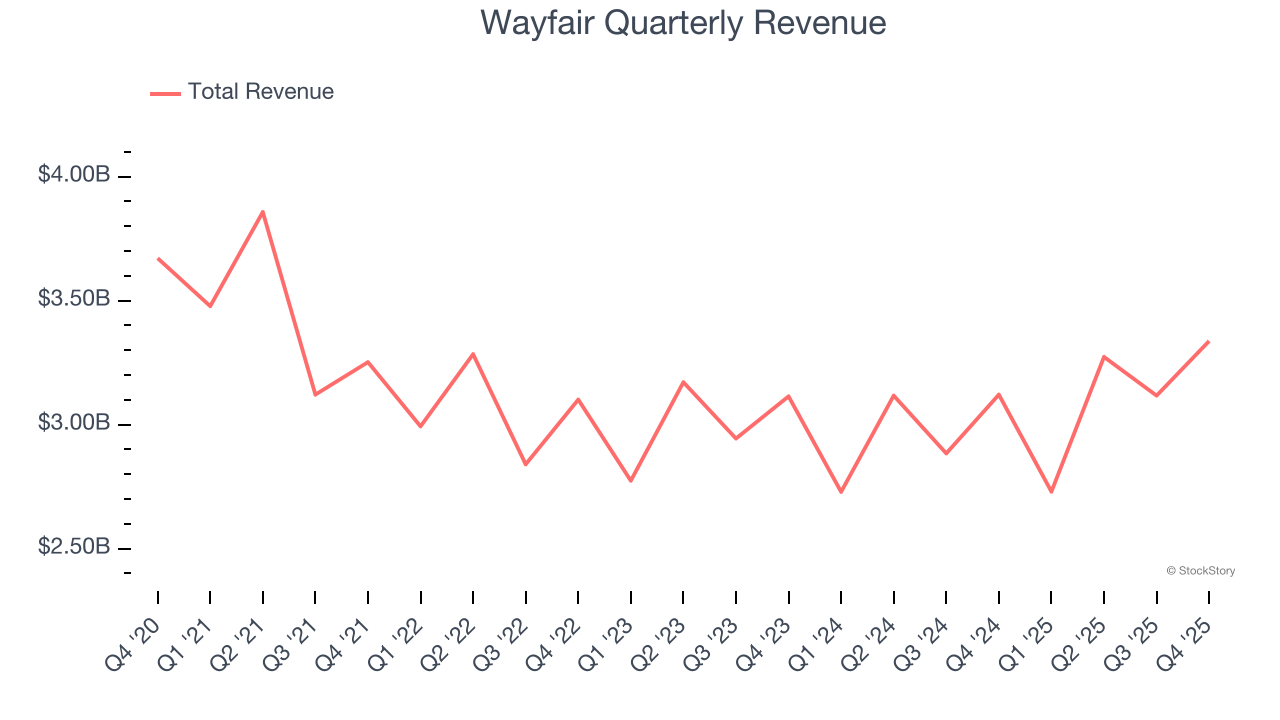

Online home goods retailer Wayfair (NYSE: W) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 6.9% year on year to $3.34 billion. Its non-GAAP profit of $0.85 per share was 23.9% above analysts’ consensus estimates.

Is now the time to buy Wayfair? Find out by accessing our full research report, it’s free.

Wayfair (W) Q4 CY2025 Highlights:

- Revenue: $3.34 billion vs analyst estimates of $3.3 billion (6.9% year-on-year growth, 1.1% beat)

- Adjusted EPS: $0.85 vs analyst estimates of $0.69 (23.9% beat)

- Adjusted EBITDA: $224 million vs analyst estimates of $199.2 million (6.7% margin, 12.5% beat)

- Operating Margin: 2.5%, up from -3.7% in the same quarter last year

- Free Cash Flow Margin: 4.3%, up from 3% in the previous quarter

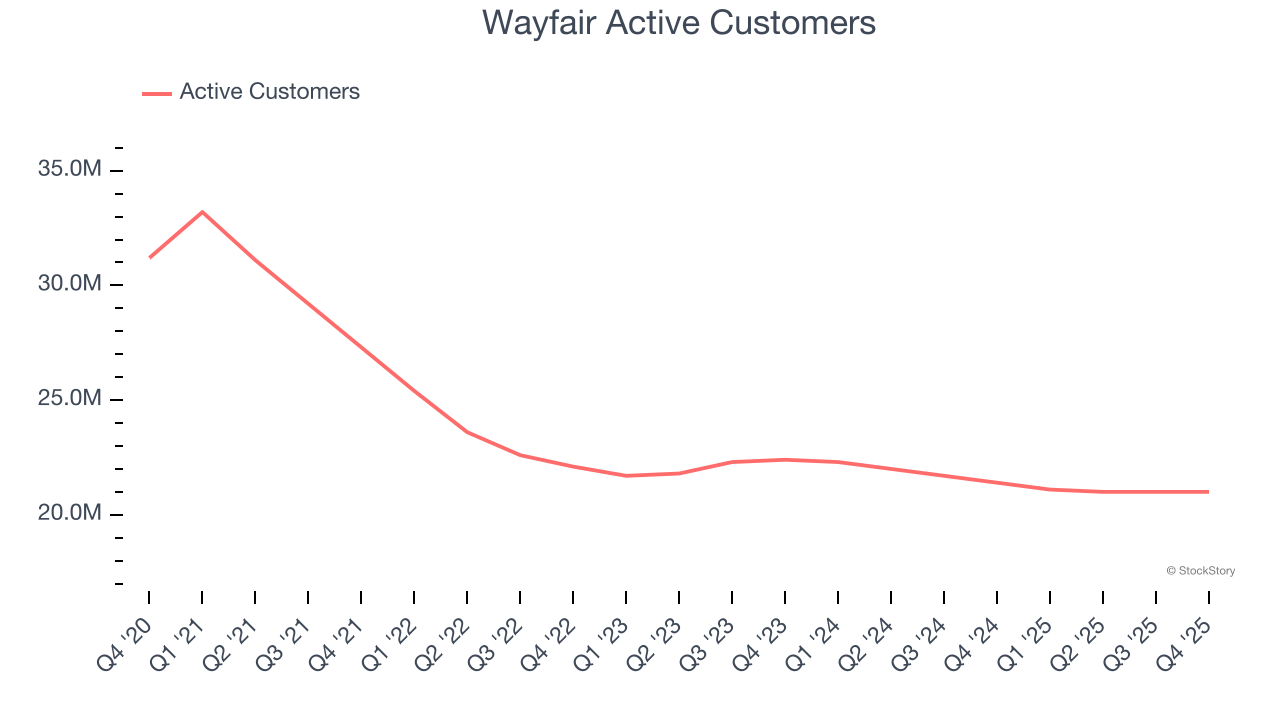

- Active Customers: 21 million, down 400,000 year on year

- Market Capitalization: $11.92 billion

"Q4 capped off a tremendous year for Wayfair, with revenue growing 7.8% year-over-year excluding the impact of Germany. We had our third consecutive quarter of new customer growth, on top of healthy growth in repeat orders, all in the face of a category that contracted in the low single digits for the final quarter of the year. 2025 was a year where we returned to growth and accelerated throughout the year through a number of organic business strategies that can compound for years to come. This was characterized by two important themes: our share capture overwhelming the drag of the macro, and the substantial flow through of that growth to the bottom line. We expect our topline growth and flow through to adjusted EBITDA to be the bedrock of our story for years to come," said Niraj Shah, CEO, co-founder and co-chairman, Wayfair.

Company Overview

Founded in 2002 by Niraj Shah, Wayfair (NYSE: W) is a leading online retailer of mass-market home goods in the US, UK, Canada, and Germany.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Wayfair struggled to consistently increase demand as its $12.46 billion of sales for the trailing 12 months was close to its revenue three years ago. This was below our standards and suggests it’s a lower quality business.

This quarter, Wayfair reported year-on-year revenue growth of 6.9%, and its $3.34 billion of revenue exceeded Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Active Customers

Buyer Growth

As an online retailer, Wayfair generates revenue growth by expanding its number of users and the average order size in dollars.

Wayfair struggled with new customer acquisition over the last two years as its active customers have declined by 2.3% annually to 21 million in the latest quarter. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Wayfair wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

In Q4, Wayfair’s active customers once again decreased by 400,000, a 1.9% drop since last year. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating buyer growth just yet.

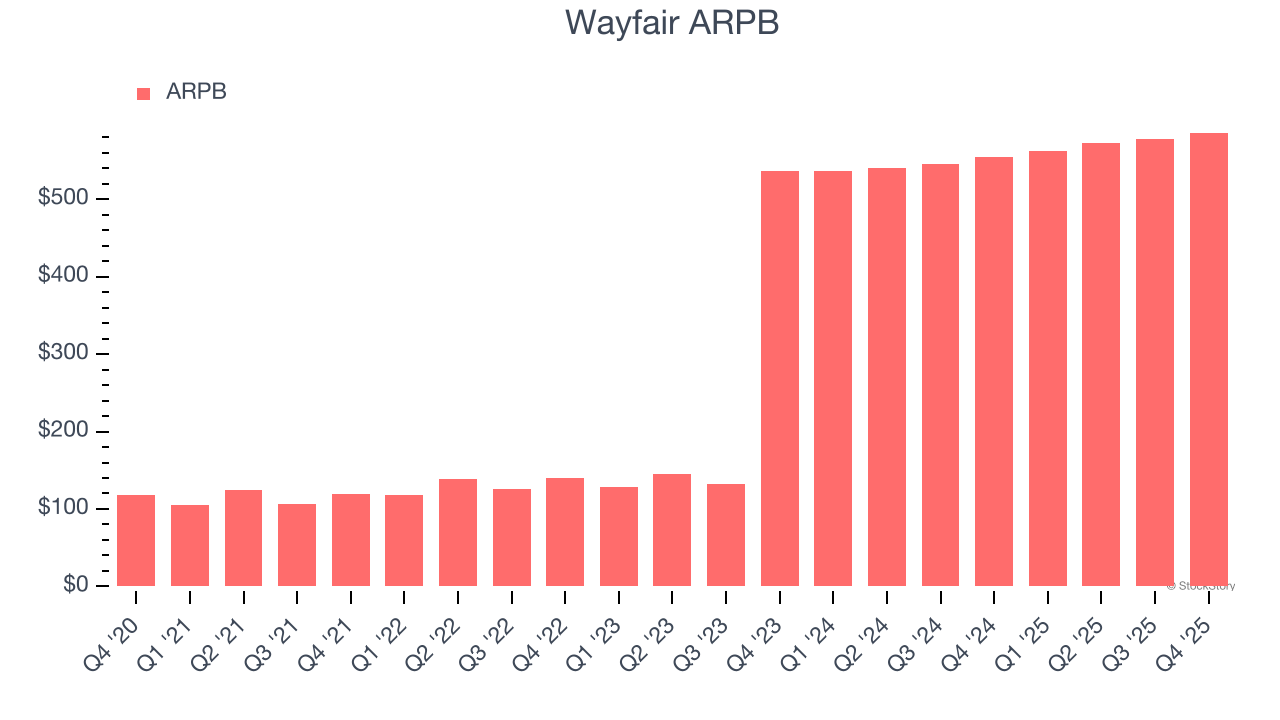

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much customers spend per order.

Wayfair’s ARPB growth has been exceptional over the last two years, averaging 116%. Although its active customers shrank during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing buyers.

This quarter, Wayfair’s ARPB clocked in at $586. It grew by 5.6% year on year, faster than its active customers.

Key Takeaways from Wayfair’s Q4 Results

We were impressed by how significantly Wayfair blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its number of buyers declined. Overall, we think this was a solid quarter with some key areas of upside. Investors were likely hoping for more, and shares traded down 2.8% to $89.54 immediately following the results.

So do we think Wayfair is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).