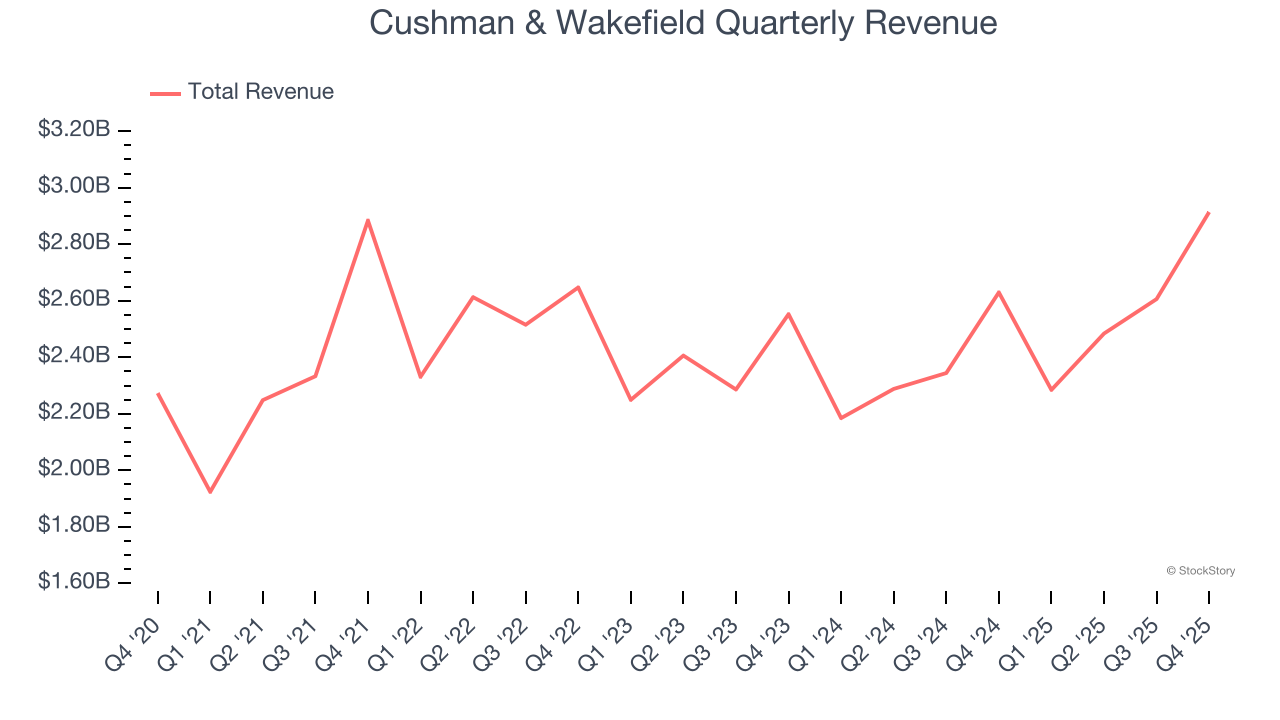

Real estate services firm Cushman & Wakefield (NYSE: CWK) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 10.8% year on year to $2.91 billion. Its non-GAAP profit of $0.54 per share was in line with analysts’ consensus estimates.

Is now the time to buy Cushman & Wakefield? Find out by accessing our full research report, it’s free.

Cushman & Wakefield (CWK) Q4 CY2025 Highlights:

- Revenue: $2.91 billion vs analyst estimates of $2.75 billion (10.8% year-on-year growth, 6.1% beat)

- Adjusted EPS: $0.54 vs analyst estimates of $0.54 (in line)

- Adjusted EBITDA: $238.7 million vs analyst estimates of $236.1 million (8.2% margin, 1.1% beat)

- Operating Margin: 6.1%, in line with the same quarter last year

- Free Cash Flow Margin: 8%, up from 3.9% in the same quarter last year

- Market Capitalization: $3.14 billion

Company Overview

With expertise in the commercial real estate sector, Cushman & Wakefield (NYSE: CWK) is a global Chicago-based real estate firm offering a comprehensive range of services to clients.

Revenue Growth

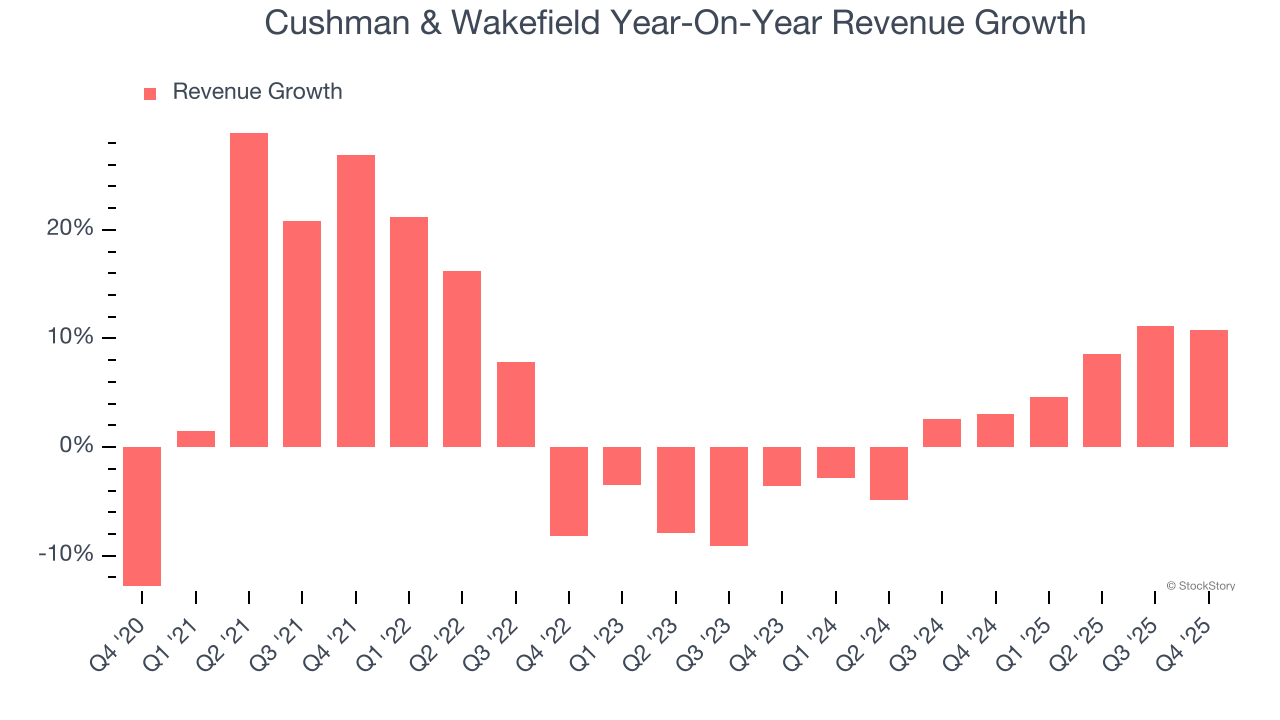

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Cushman & Wakefield’s 5.6% annualized revenue growth over the last five years was weak. This was below our standard for the consumer discretionary sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Cushman & Wakefield’s recent performance shows its demand has slowed as its annualized revenue growth of 4.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

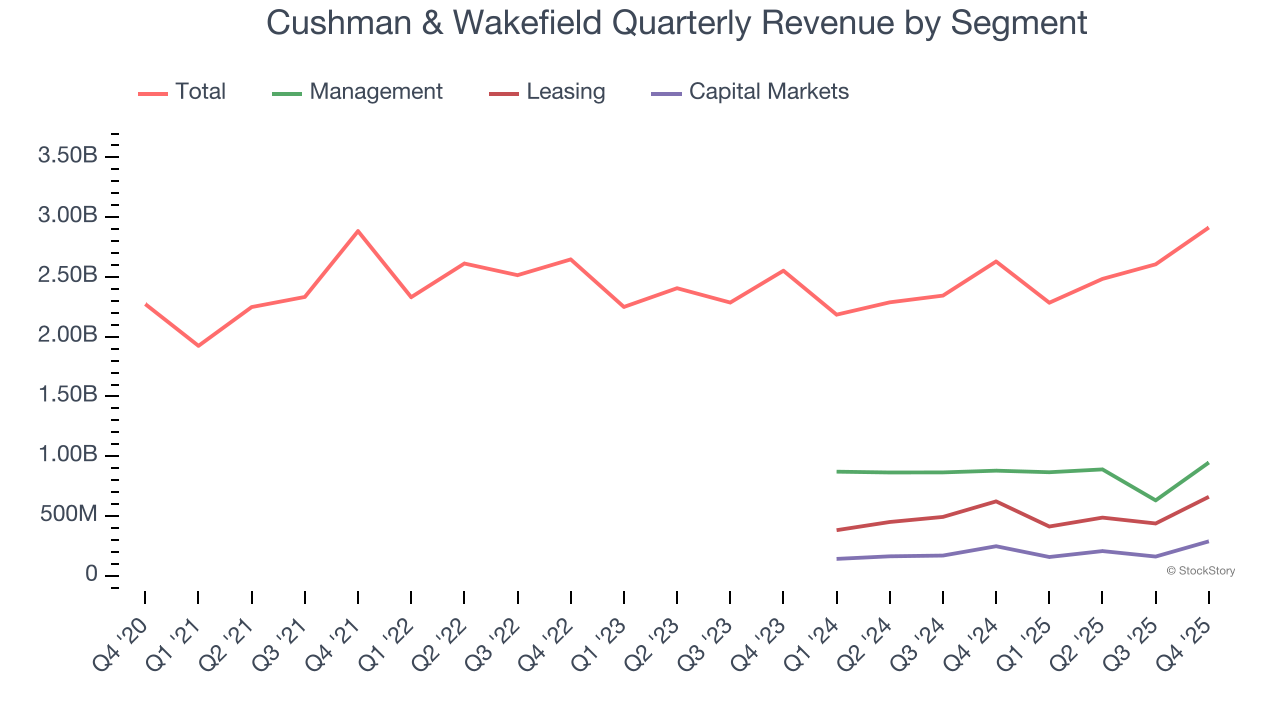

Cushman & Wakefield also breaks out the revenue for its three most important segments: Management, Leasing, and Capital Markets, which are 32.5%, 22.7%, and 9.9% of revenue. Over the last two years, Cushman & Wakefield’s Management revenue (property management) averaged 4.2% year-on-year declines, but its Leasing (sourcing tenants) and Capital Markets (financial advisory) revenues averaged 2.8% and 12.4% growth.

This quarter, Cushman & Wakefield reported year-on-year revenue growth of 10.8%, and its $2.91 billion of revenue exceeded Wall Street’s estimates by 6.1%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

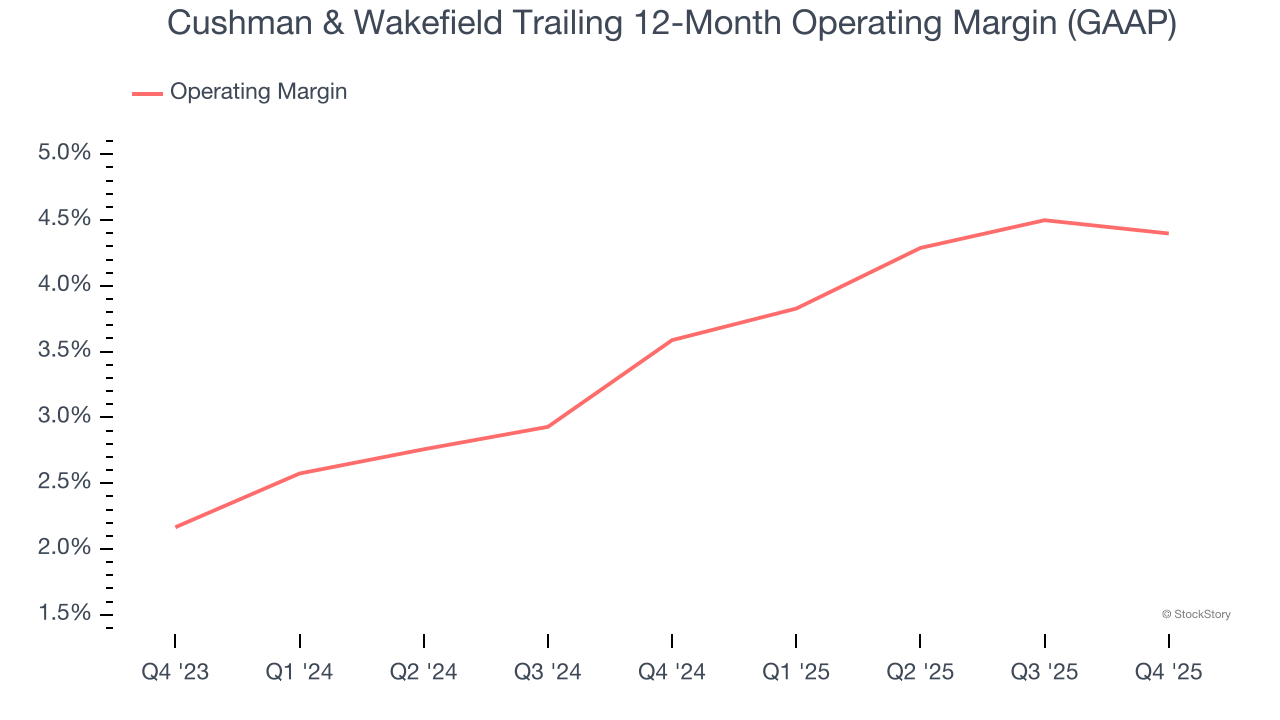

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Cushman & Wakefield’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 4% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

In Q4, Cushman & Wakefield generated an operating margin profit margin of 6.1%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

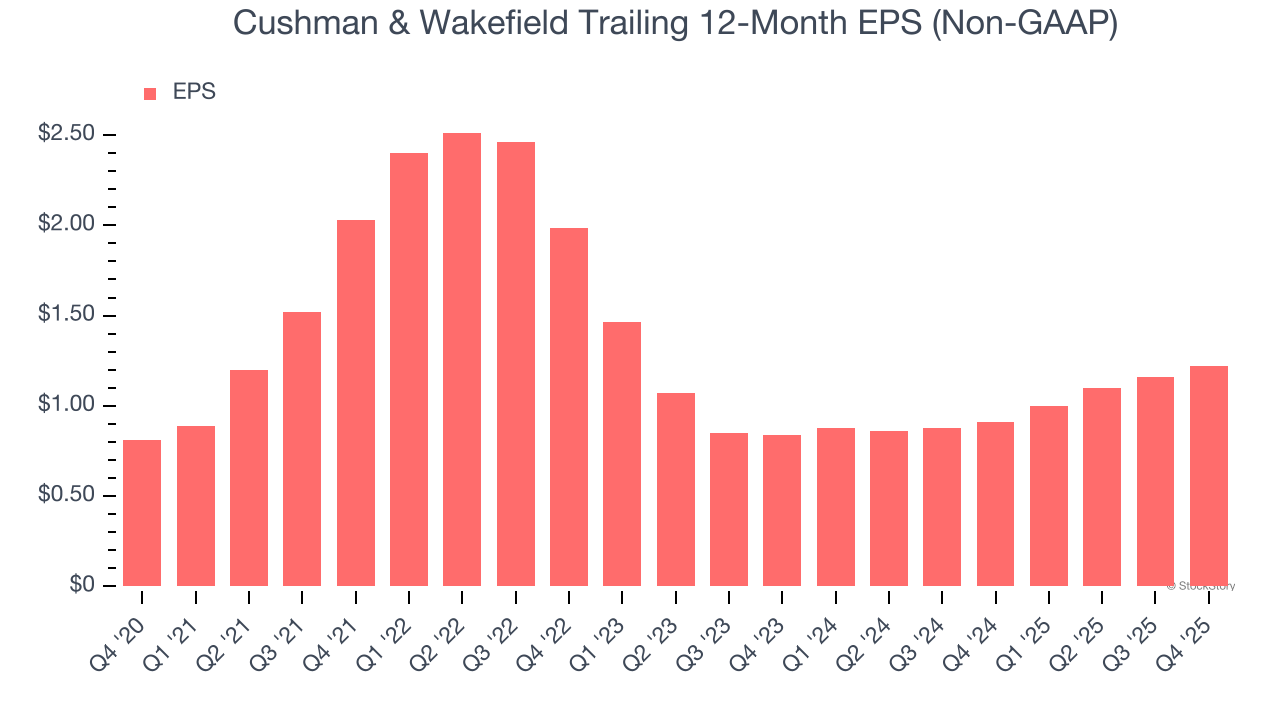

Cushman & Wakefield’s EPS grew at a weak 8.5% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 5.6% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

In Q4, Cushman & Wakefield reported adjusted EPS of $0.54, up from $0.48 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Cushman & Wakefield’s full-year EPS of $1.22 to grow 17.8%.

Key Takeaways from Cushman & Wakefield’s Q4 Results

We enjoyed seeing Cushman & Wakefield beat analysts’ revenue expectations this quarter. Overall, this print had some key positives. The stock remained flat at $13.56 immediately following the results.

Is Cushman & Wakefield an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).