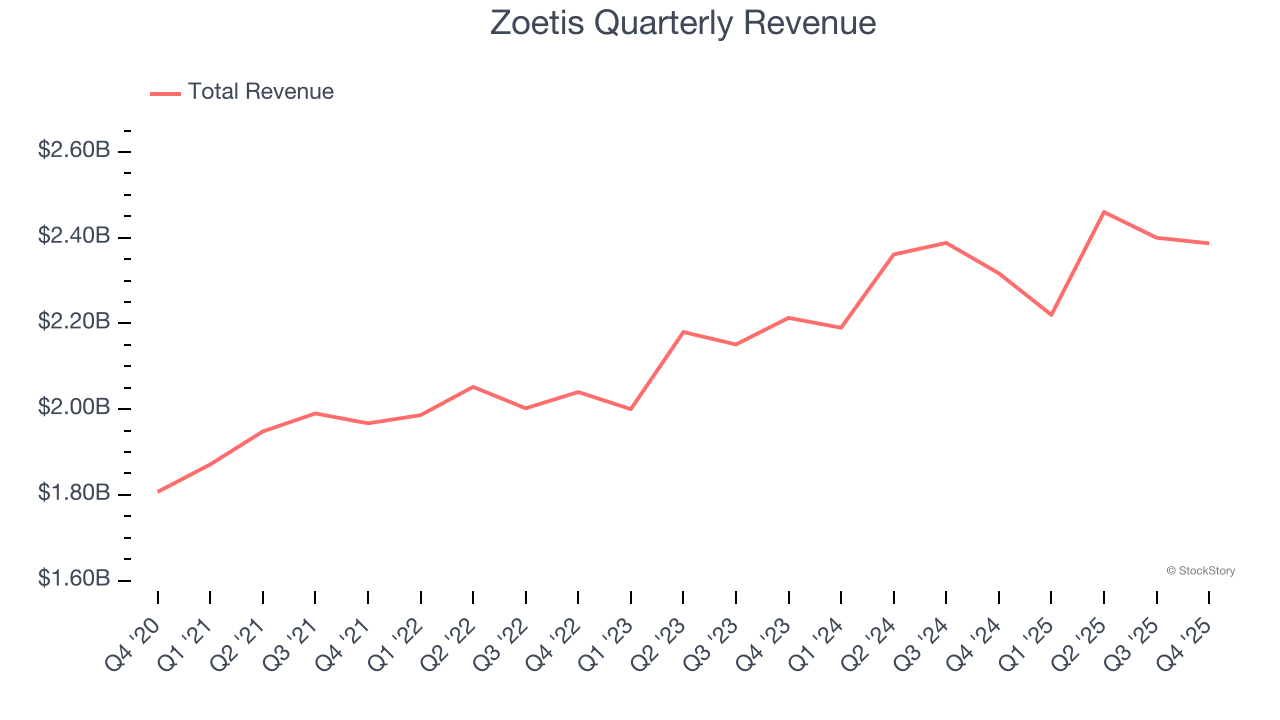

Animal health company Zoetis (NYSE: ZTS) announced better-than-expected revenue in Q4 CY2025, with sales up 3% year on year to $2.39 billion. The company expects the full year’s revenue to be around $9.93 billion, close to analysts’ estimates. Its non-GAAP profit of $1.48 per share was 5.5% above analysts’ consensus estimates.

Is now the time to buy Zoetis? Find out by accessing our full research report, it’s free.

Zoetis (ZTS) Q4 CY2025 Highlights:

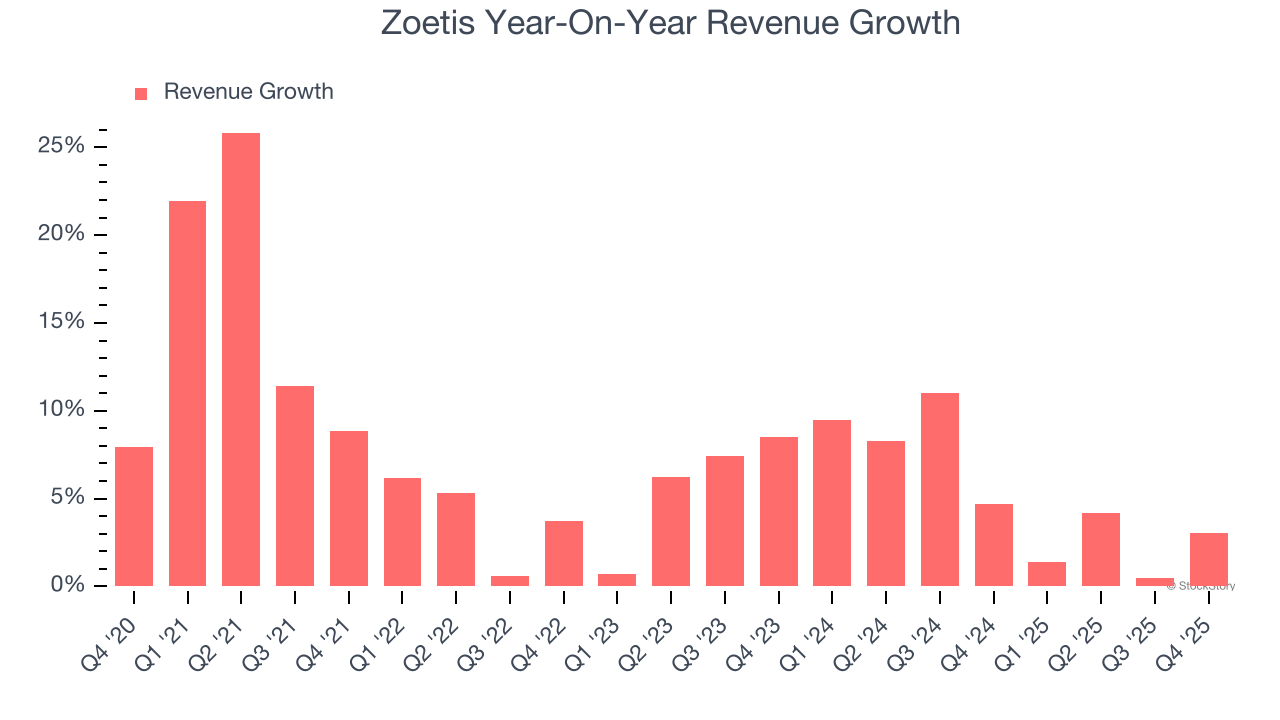

- Revenue: $2.39 billion vs analyst estimates of $2.37 billion (3% year-on-year growth, 0.8% beat)

- Adjusted EPS: $1.48 vs analyst estimates of $1.40 (5.5% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $7.05 at the midpoint, beating analyst estimates by 3.3%

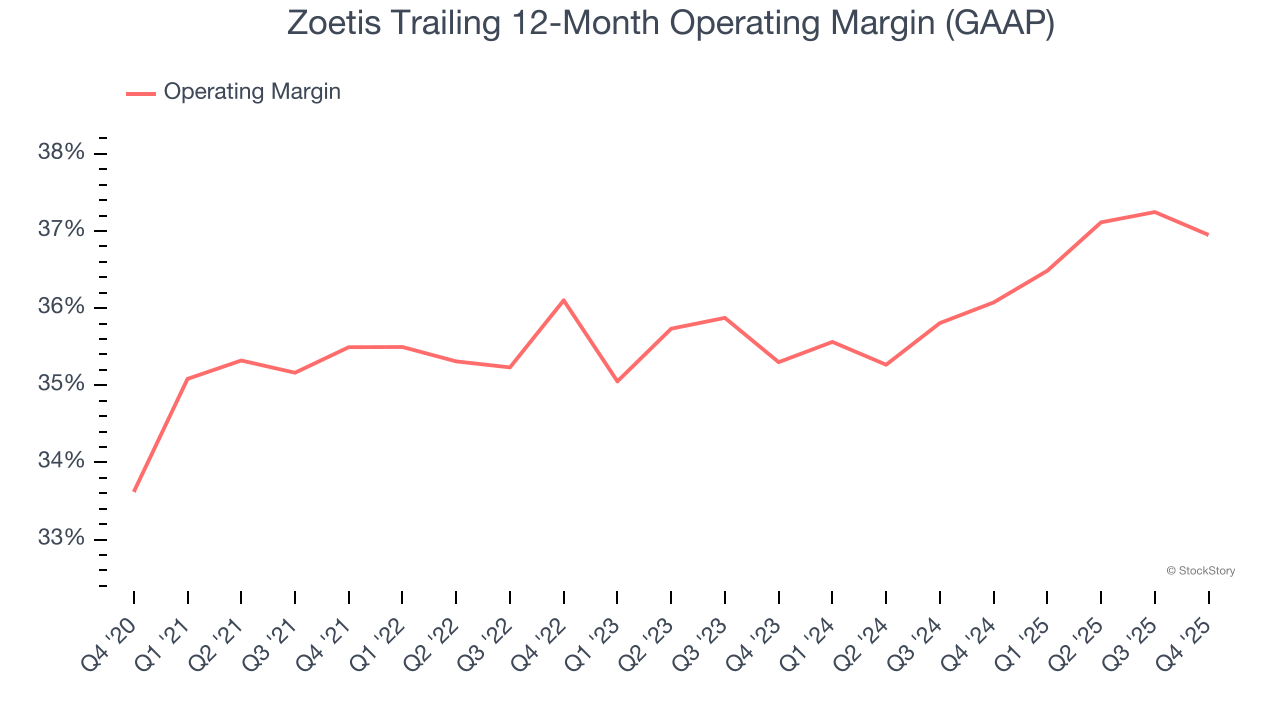

- Operating Margin: 31.9%, down from 32.9% in the same quarter last year

- Market Capitalization: $56.7 billion

"Zoetis delivered solid results in 2025, demonstrating the strength and resilience of our portfolio across species, geographies, and channels. Leadership across key brands and categories drove continued growth, even as we navigated a dynamic operating environment,” said Kristin Peck, Chief Executive Officer of Zoetis.

Company Overview

Originally spun off from Pfizer in 2013 as the world's largest pure-play animal health company, Zoetis (NYSE: ZTS) discovers, develops, and sells medicines, vaccines, diagnostic products, and services for pets and livestock animals worldwide.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Zoetis’s sales grew at a mediocre 7.2% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the healthcare sector, but there are still things to like about Zoetis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Zoetis’s recent performance shows its demand has slowed as its annualized revenue growth of 5.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Zoetis reported modest year-on-year revenue growth of 3% but beat Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not catalyze better top-line performance yet. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Zoetis has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average operating margin of 36%.

Analyzing the trend in its profitability, Zoetis’s operating margin rose by 1.5 percentage points over the last five years, as its sales growth gave it operating leverage. The company’s two-year trajectory shows its performance was mostly driven by its recent improvements.

In Q4, Zoetis generated an operating margin profit margin of 31.9%, down 1 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

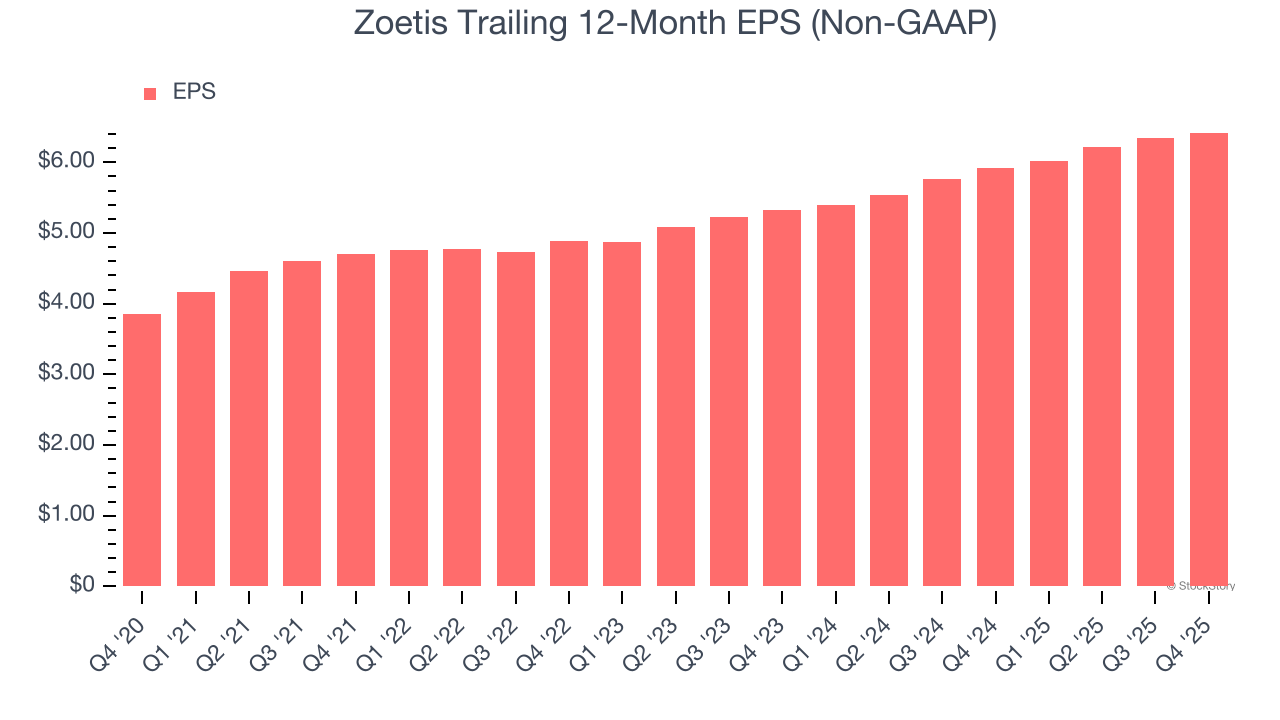

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Zoetis’s EPS grew at a remarkable 10.8% compounded annual growth rate over the last five years, higher than its 7.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

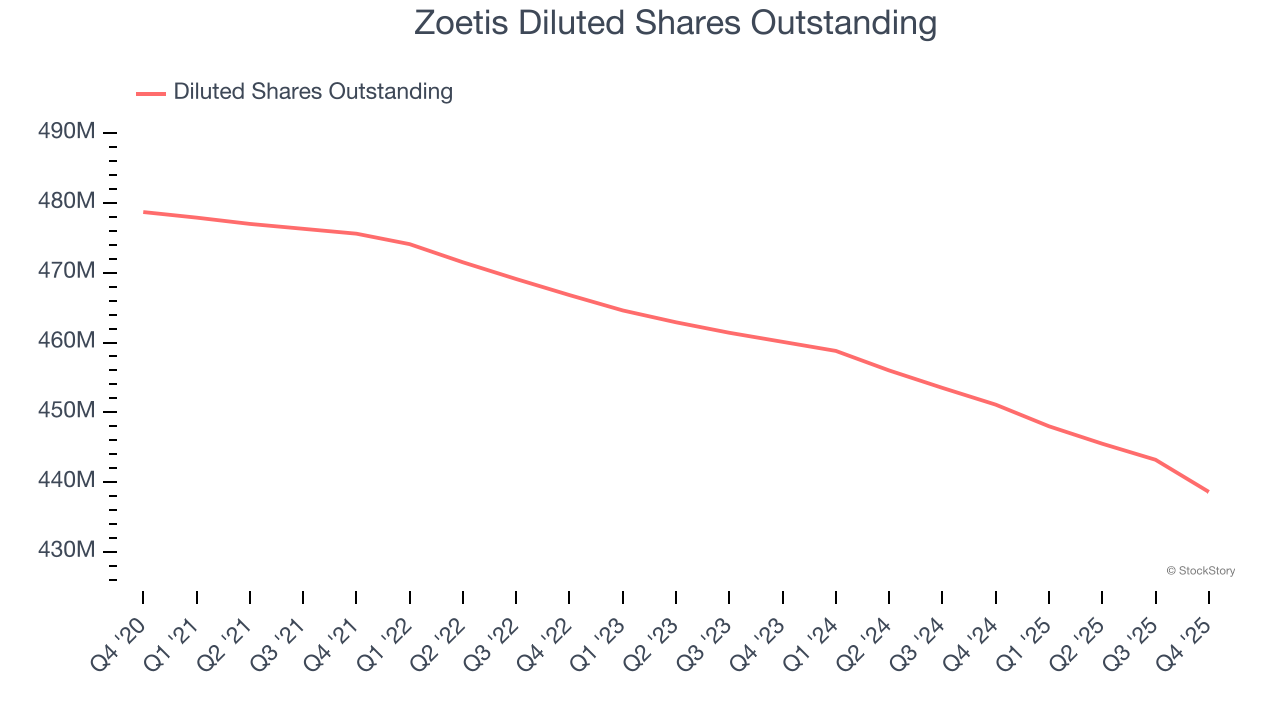

We can take a deeper look into Zoetis’s earnings to better understand the drivers of its performance. As we mentioned earlier, Zoetis’s operating margin declined this quarter but expanded by 1.5 percentage points over the last five years. Its share count also shrank by 8.4%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, Zoetis reported adjusted EPS of $1.48, up from $1.40 in the same quarter last year. This print beat analysts’ estimates by 5.5%. Over the next 12 months, Wall Street expects Zoetis’s full-year EPS of $6.42 to grow 6%.

Key Takeaways from Zoetis’s Q4 Results

We enjoyed seeing Zoetis beat analysts’ full-year EPS guidance expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 4.8% to $134.82 immediately following the results.

Zoetis put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).