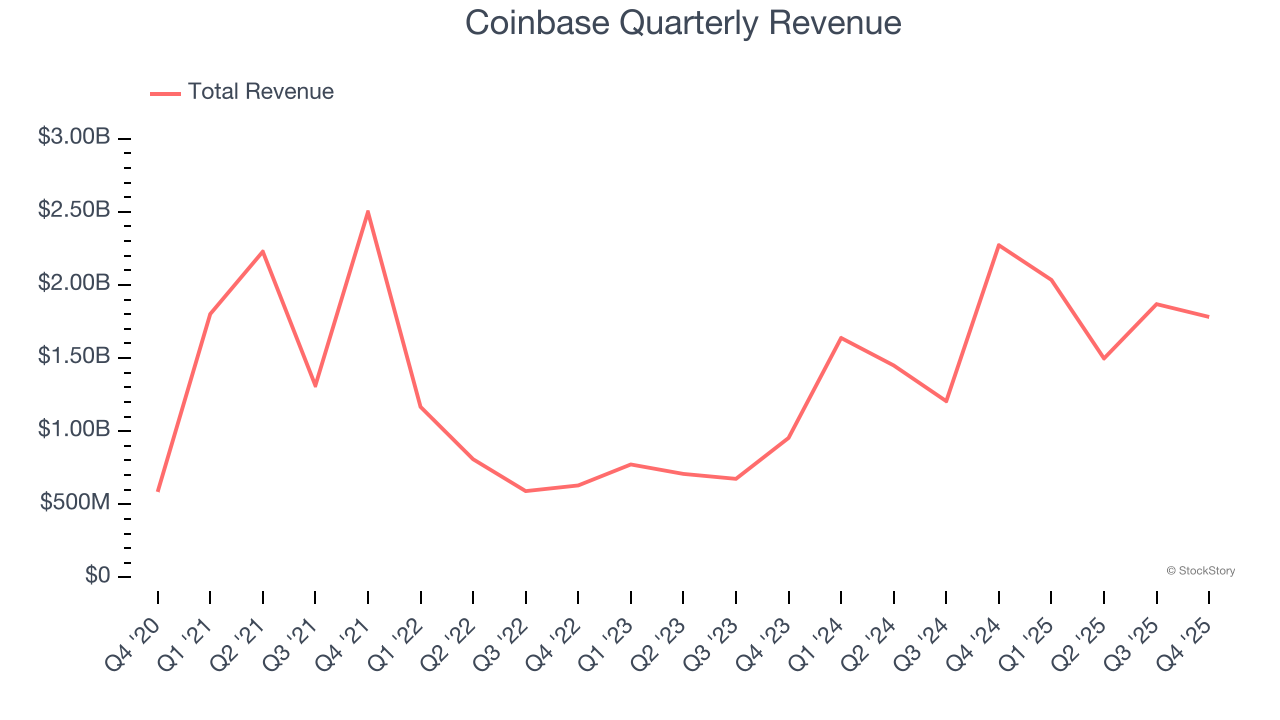

Blockchain infrastructure company Coinbase (NASDAQ: COIN) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 21.6% year on year to $1.78 billion. Its non-GAAP profit of $0.66 per share was 31.2% below analysts’ consensus estimates.

Is now the time to buy Coinbase? Find out by accessing our full research report, it’s free.

Coinbase (COIN) Q4 CY2025 Highlights:

- Revenue: $1.78 billion vs analyst estimates of $1.83 billion (21.6% year-on-year decline, 2.5% miss)

- Adjusted EPS: $0.66 vs analyst expectations of $0.96 (31.2% miss)

- Adjusted EBITDA: $566 million vs analyst estimates of $680.8 million (31.8% margin, 16.9% miss)

- Operating Margin: 15.4%, down from 45.5% in the same quarter last year

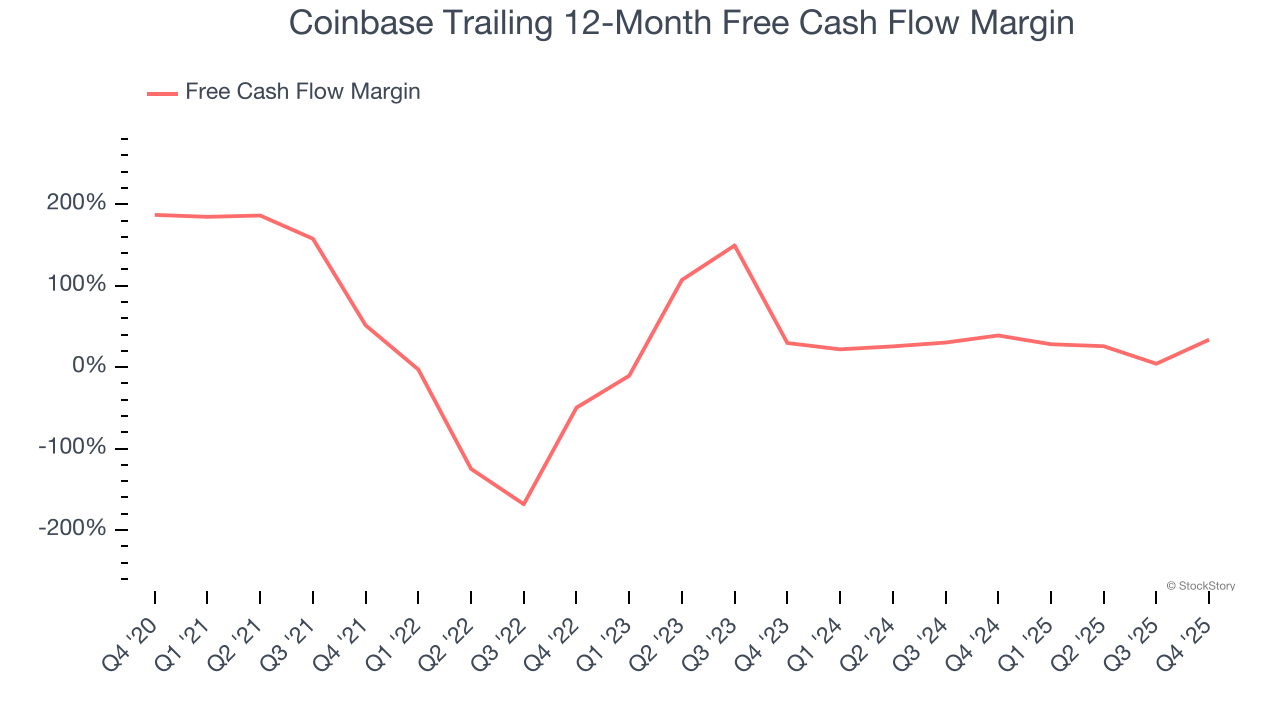

- Free Cash Flow was $3.07 billion, up from -$784.5 million in the previous quarter

- Market Capitalization: $41.31 billion

Company Overview

Widely regarded as the face of crypto, Coinbase (NASDAQ: COIN) is a blockchain infrastructure company updating the financial system with its trading, staking, stablecoin, and other payment solutions.

Revenue Growth

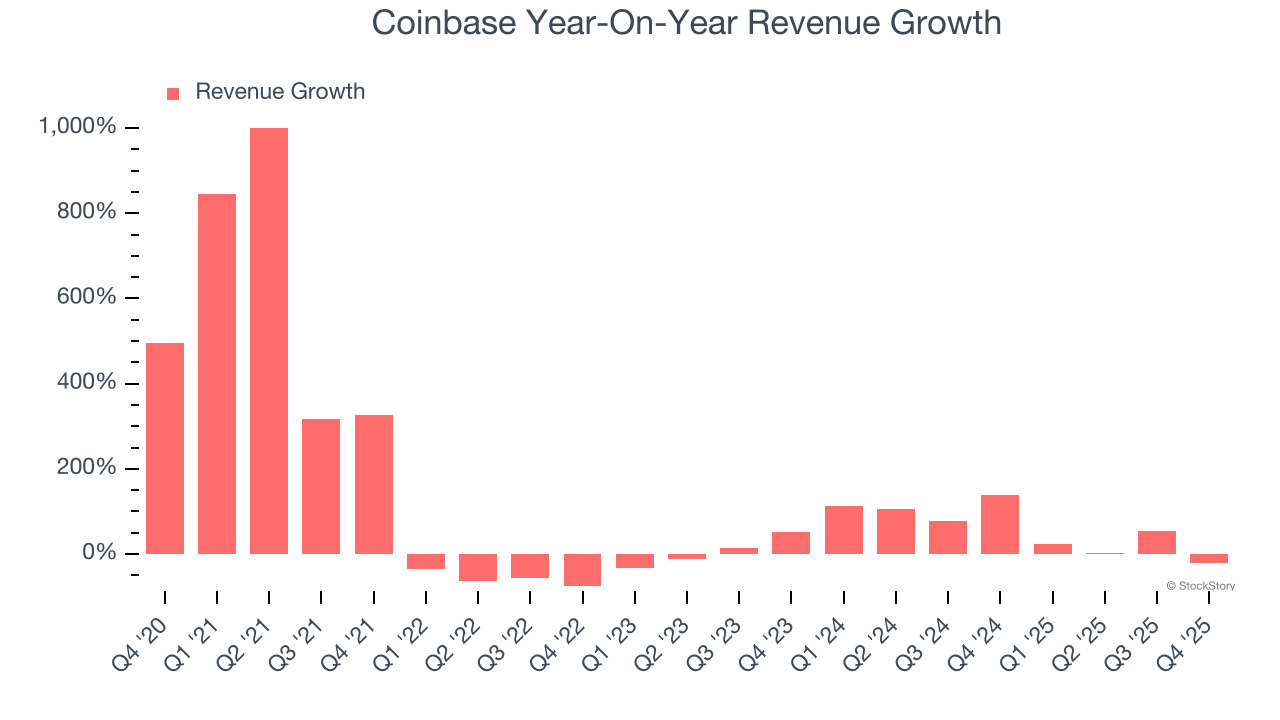

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Coinbase grew its sales at an incredible 41.2% compounded annual growth rate. Its growth beat the average consumer internet company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer internet, a half-decade historical view may miss recent innovations or disruptive industry trends. Coinbase’s annualized revenue growth of 52% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Coinbase missed Wall Street’s estimates and reported a rather uninspiring 21.6% year-on-year revenue decline, generating $1.78 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 14.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is noteworthy and implies the market is baking in success for its products and services.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Coinbase has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging an eye-popping 36.3% over the last two years.

Taking a step back, we can see that Coinbase’s margin dropped by 17.7 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity.

Coinbase’s free cash flow clocked in at $3.07 billion in Q4, equivalent to a 172% margin. This result was good as its margin was 129.6 percentage points higher than in the same quarter last year. Its cash profitability was also above its two-year level, and we hope the company can build on this trend.

Key Takeaways from Coinbase’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $141.73 immediately after reporting.

So do we think Coinbase is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).