Over the past six months, TransDigm’s stock price fell to $1,444. Shareholders have lost 8.8% of their capital, which is disappointing considering the S&P 500 has climbed by 10%. This may have investors wondering how to approach the situation.

Given the weaker price action, is now a good time to buy TDG? Find out in our full research report, it’s free.

Why Are We Positive On TransDigm?

Supplying parts for nearly all aircraft currently in service, TransDigm (NYSE: TDG) develops and manufactures components and systems for military and commercial aviation.

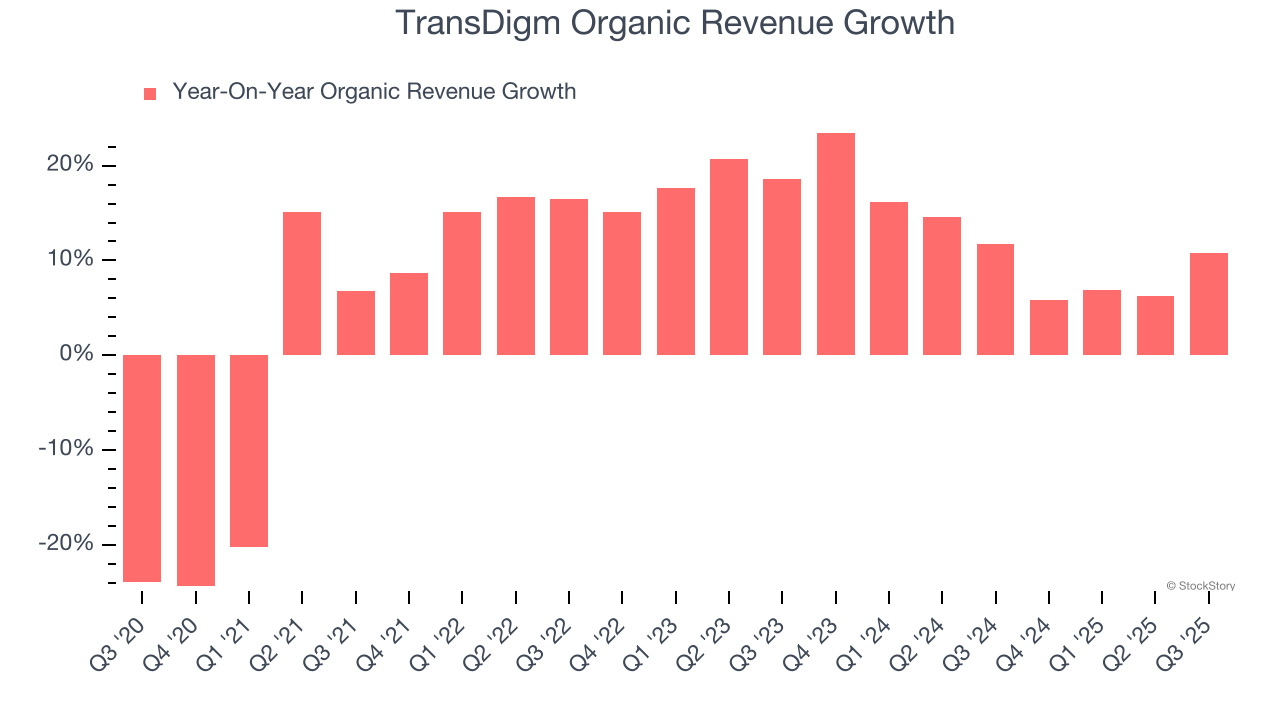

1. Core Business Firing on All Cylinders

We can better understand Aerospace companies by analyzing their organic revenue. This metric gives visibility into TransDigm’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, TransDigm’s organic revenue averaged 12% year-on-year growth. This performance was impressive and shows it can expand quickly without relying on expensive (and risky) acquisitions.

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

TransDigm’s EPS grew at an astounding 20.9% compounded annual growth rate over the last five years, higher than its 11.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

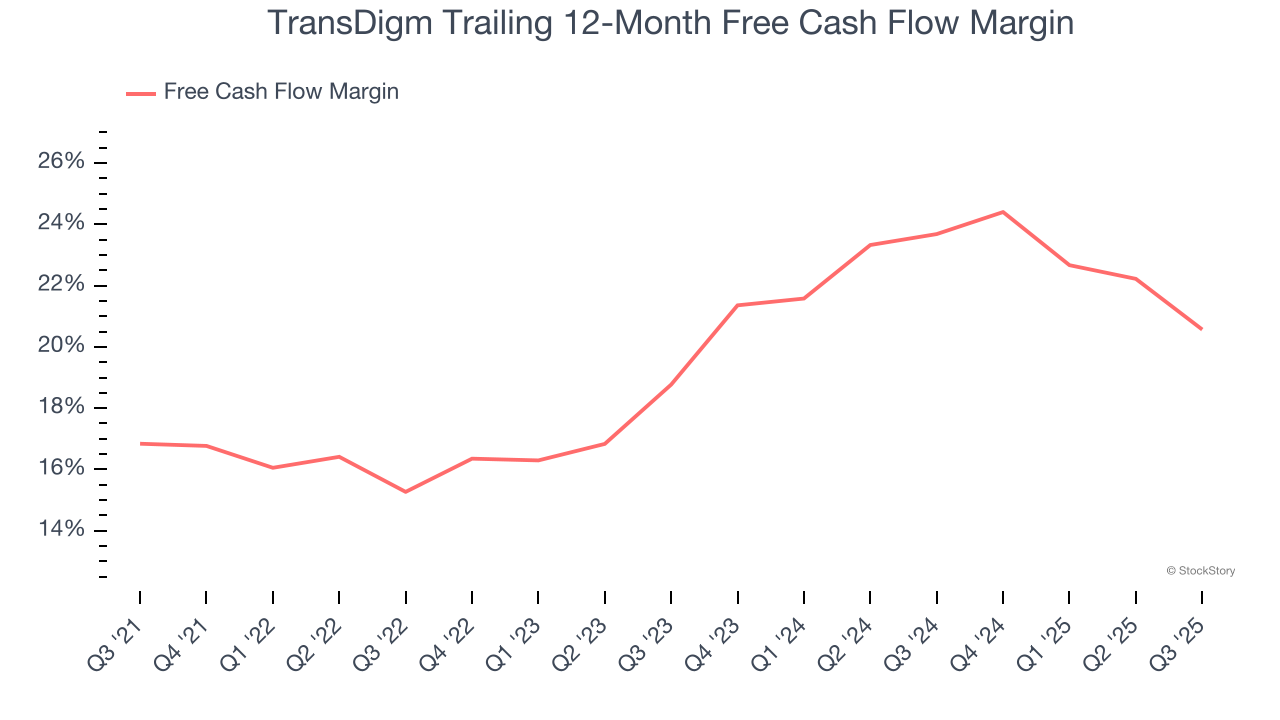

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

TransDigm has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 19.6% over the last five years.

Final Judgment

These are just a few reasons why TransDigm is one of the best industrials companies out there. After the recent drawdown, the stock trades at 37.5× forward P/E (or $1,444 per share). Is now the right time to buy? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.