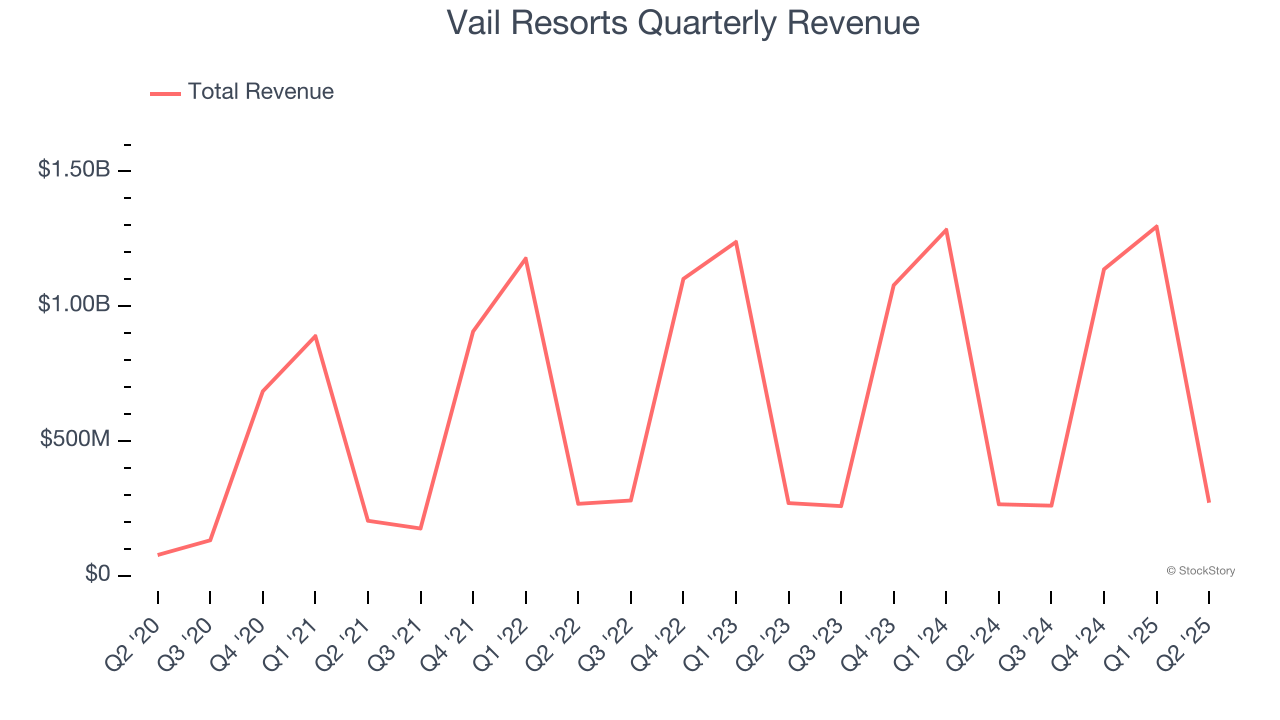

Luxury ski resort company Vail Resorts (NYSE: MTN) fell short of the market’s revenue expectations in Q2 CY2025 as sales rose 2.2% year on year to $271.3 million. Its GAAP loss of $5.08 per share was 7.7% below analysts’ consensus estimates.

Is now the time to buy Vail Resorts? Find out by accessing our full research report, it’s free.

Vail Resorts (MTN) Q2 CY2025 Highlights:

- Revenue: $271.3 million vs analyst estimates of $272.8 million (2.2% year-on-year growth, 0.5% miss)

- EPS (GAAP): -$5.08 vs analyst expectations of -$4.72 (7.7% miss)

- Adjusted EBITDA: -$124.8 million vs analyst estimates of -$125.3 million (-46% margin, in line)

- EBITDA guidance for the upcoming financial year 2026 is $875 million at the midpoint, below analyst estimates of $890.4 million

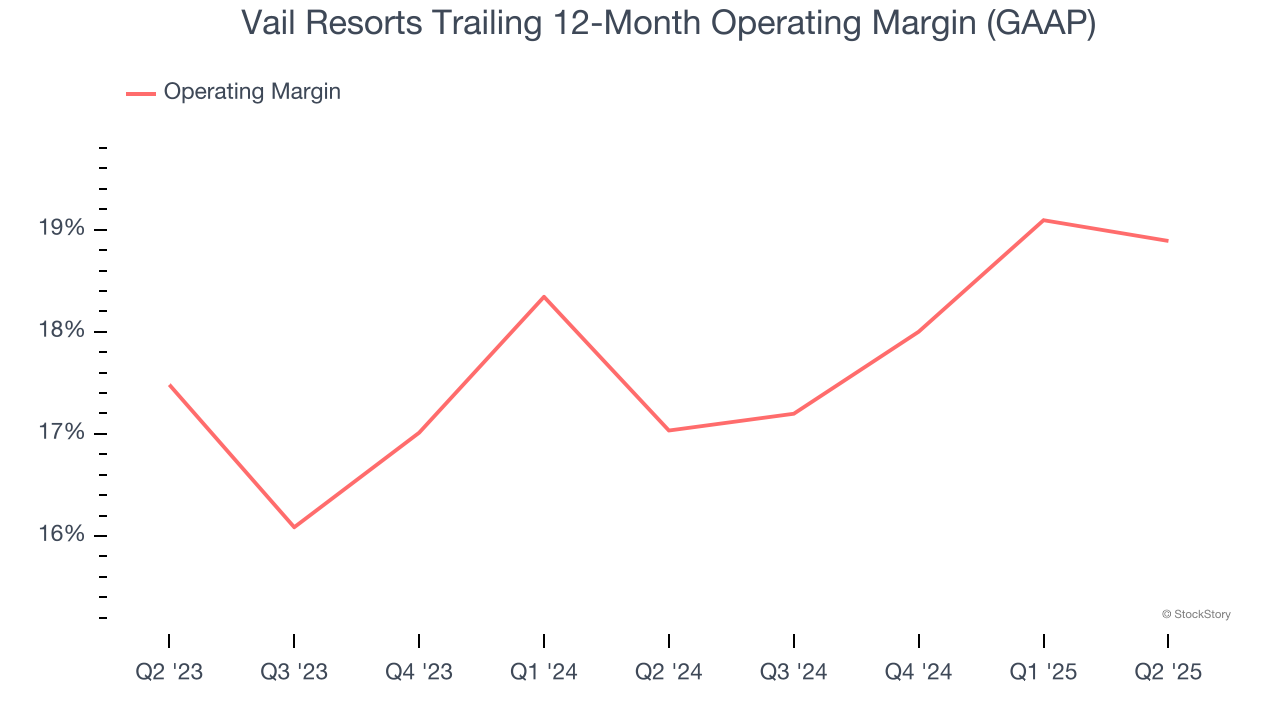

- Operating Margin: -75.1%, in line with the same quarter last year

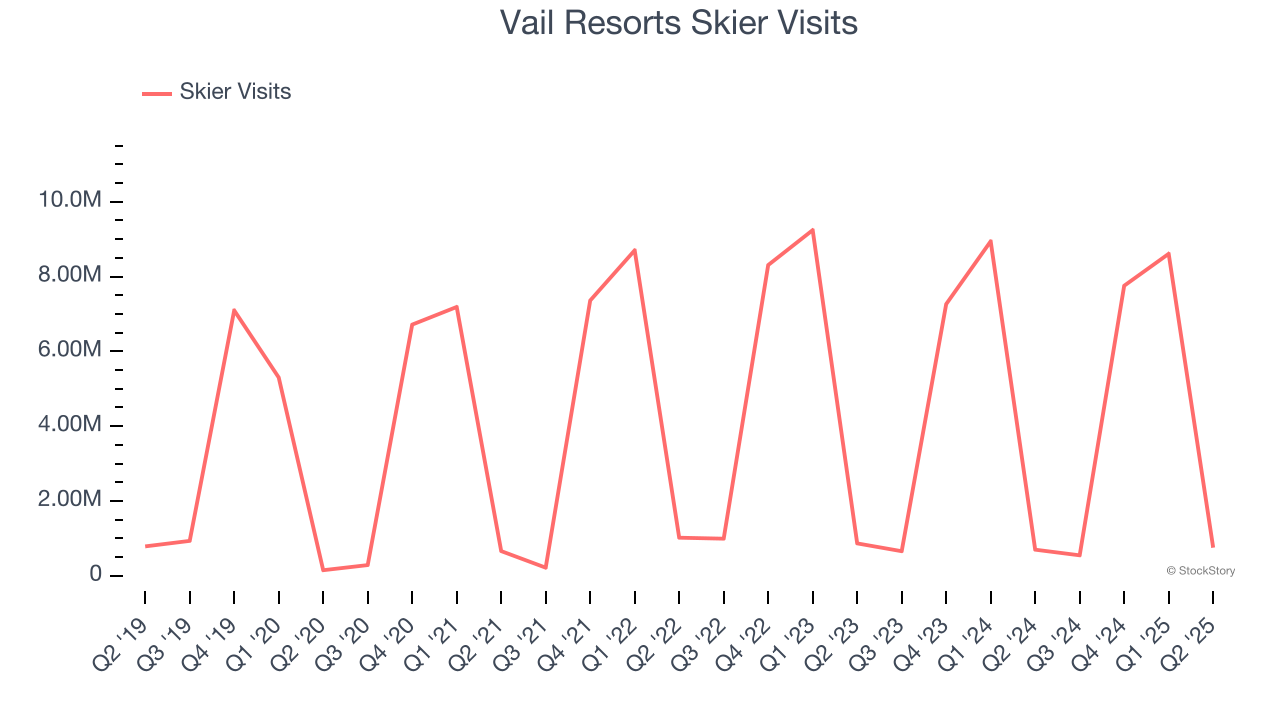

- Skier Visits: 753,000, up 54,000 year on year

- Market Capitalization: $5.49 billion

Commenting on the Company's fiscal 2025 results, Rob Katz, Chief Executive Officer, said, "The Company achieved 2% growth in Resort Reported EBITDA despite total skier visits declining 3% across our North American destination mountain resorts and regional ski areas versus the prior year. Visitation reflects the benefit of improved conditions in the second quarter relative to the prior year, offset by the expected decline in visitation from selling fewer pass units for the 2024/2025 North American ski season. For the full year, Resort net revenue increased 3% driven by a 4% increase in season pass revenue and increased ancillary spend per guest across our ski school and dining businesses. Resort Reported EBITDA for fiscal 2025 also reflects strong cost discipline, including $37 million of savings from the resource efficiency transformation plan before one-time costs. The Company's full year Resort Reported EBITDA growth is partially offset by $14 million of increased costs from company-wide performance-based management incentive plan expense that was not earned in the prior year, $15 million of one-time costs related to the two-year resource efficiency transformation plan, $8 million of one-time costs related to the Company's previously announced CEO transition, and $5 million unfavorable EBITDA impact from changes in foreign exchange rates relative to the prior year. Excluding these impacts and removing the impact of Crans-Montana operating results and acquisition, closing, and integration expenses in both periods, Resort Reported EBITDA increased approximately 6% compared to the prior year, despite the decline in total skier visits across our North American resorts versus the prior year, highlighting strong cost discipline and the impacts of the resource efficiency transformation plan."

Company Overview

Founded by two Aspen, Colorado ski patrol guides, Vail Resorts (NYSE: MTN) is a mountain resort company offering luxury experiences in over 30 locations across the globe.

Revenue Growth

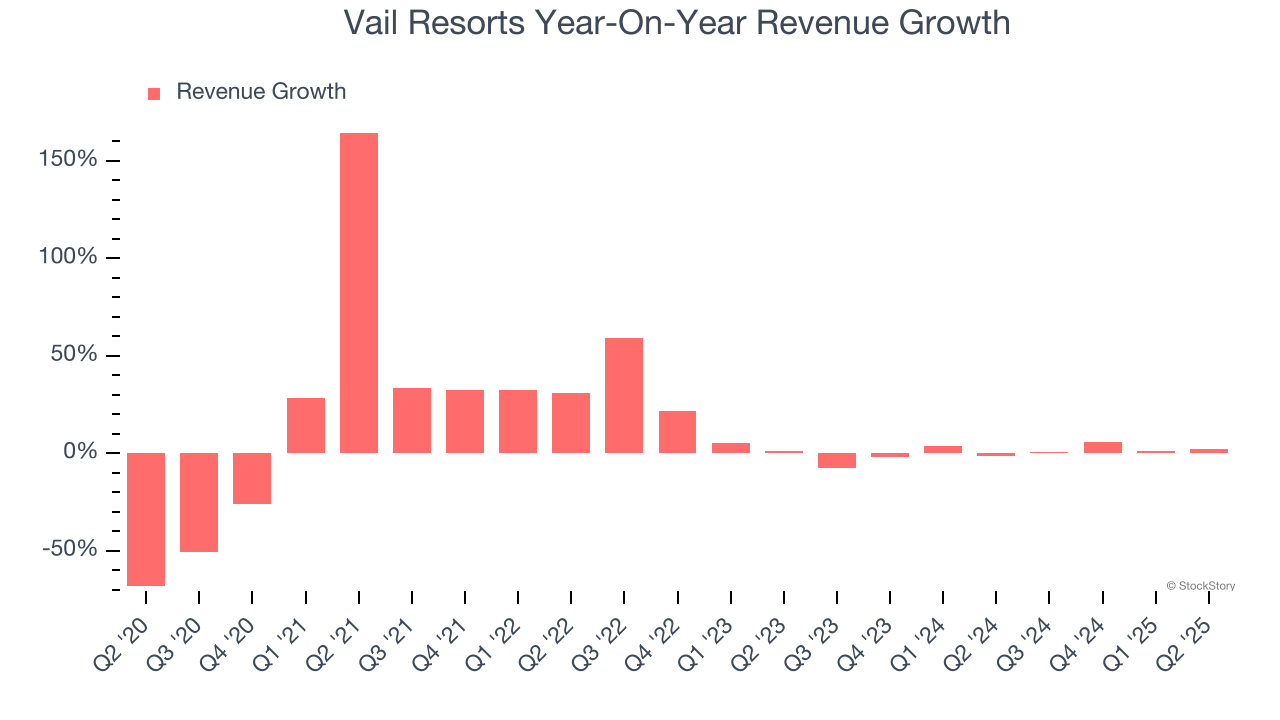

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Vail Resorts grew its sales at a sluggish 8.6% compounded annual growth rate. This was below our standard for the consumer discretionary sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Vail Resorts’s recent performance shows its demand has slowed as its annualized revenue growth of 1.3% over the last two years was below its five-year trend. Note that COVID hurt Vail Resorts’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

We can dig further into the company’s revenue dynamics by analyzing its number of skier visits, which reached 753,000 in the latest quarter. Over the last two years, Vail Resorts’s skier visits averaged 9.4% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Vail Resorts’s revenue grew by 2.2% year on year to $271.3 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.4% over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Vail Resorts’s operating margin has risen over the last 12 months and averaged 18% over the last two years. On top of that, its profitability was top-notch for a consumer discretionary business, showing it’s an well-run company with an efficient cost structure.

This quarter, Vail Resorts generated an operating margin profit margin of negative 75.1%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

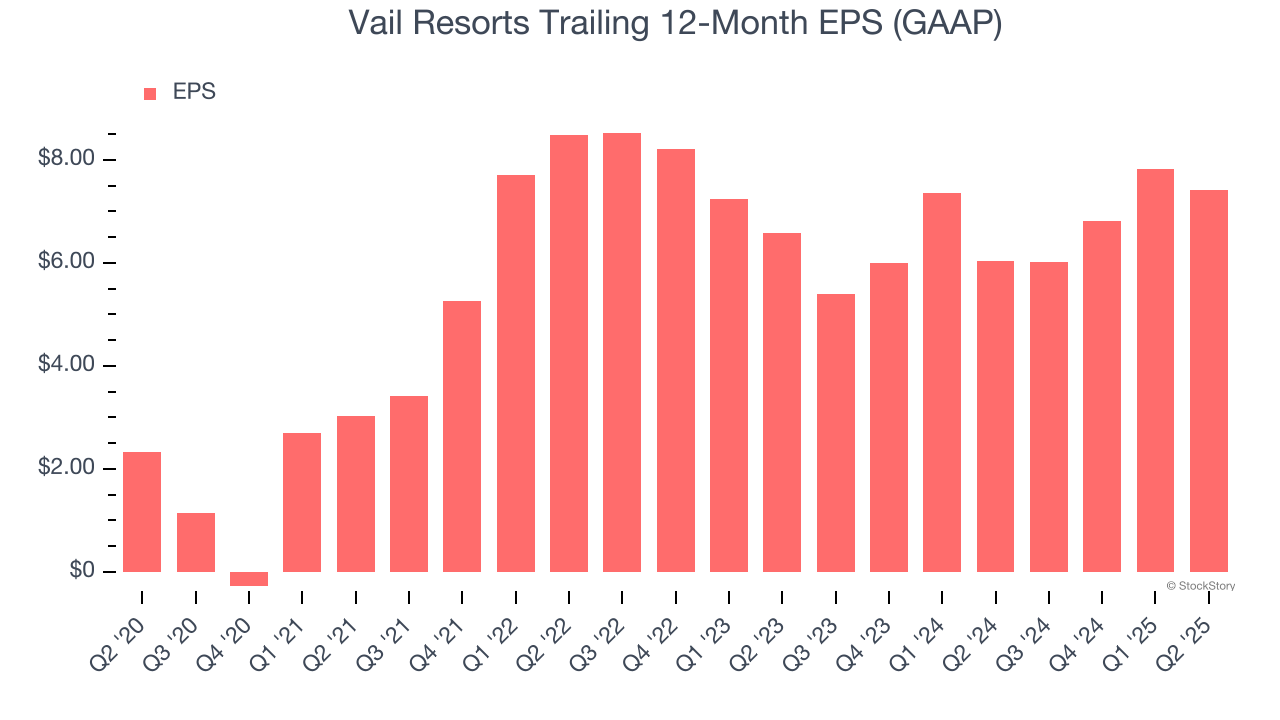

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Vail Resorts’s EPS grew at an astounding 26.1% compounded annual growth rate over the last five years, higher than its 8.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q2, Vail Resorts reported EPS of negative $5.08, down from negative $4.67 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Vail Resorts’s full-year EPS of $7.41 to grow 2.9%.

Key Takeaways from Vail Resorts’s Q2 Results

We struggled to find many positives in these results. Its EPS missed and its . Overall, this was a softer quarter. The stock traded down 1.4% to $146 immediately after reporting.

Vail Resorts’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.