Over the past six months, BOK Financial’s shares (currently trading at $96.95) have posted a disappointing 10.4% loss, well below the S&P 500’s 2.8% gain. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in BOK Financial, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is BOK Financial Not Exciting?

Despite the more favorable entry price, we're swiping left on BOK Financial for now. Here are three reasons why there are better opportunities than BOKF and a stock we'd rather own.

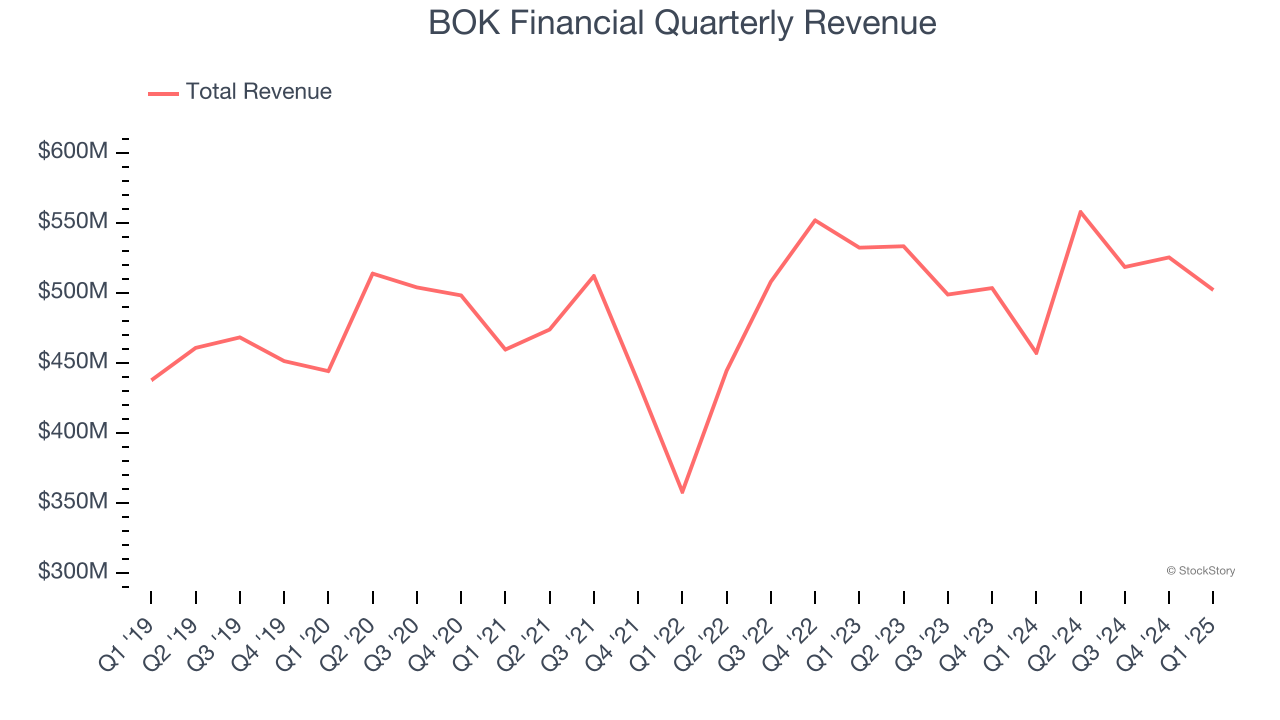

1. Long-Term Revenue Growth Disappoints

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income.

Regrettably, BOK Financial’s revenue grew at a tepid 2.9% compounded annual growth rate over the last five years. This fell short of our benchmarks.

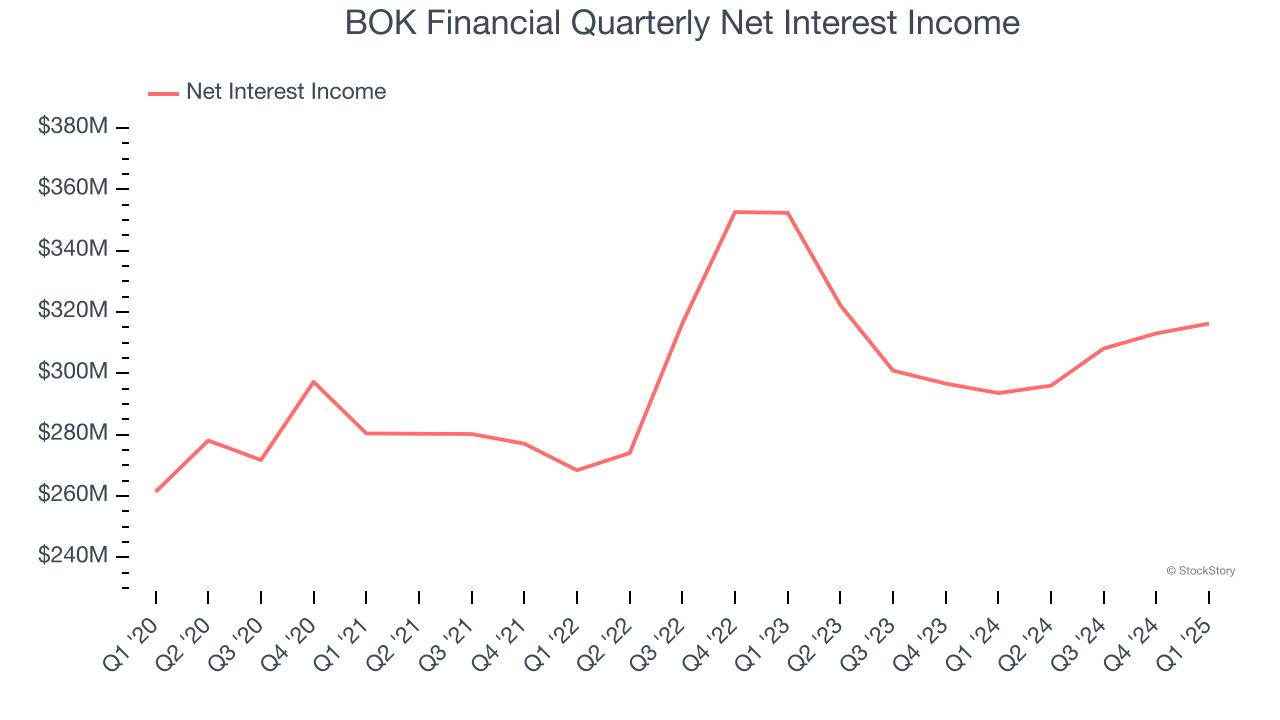

2. Net Interest Income Points to Soft Demand

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

BOK Financial’s net interest income has grown at a 2.3% annualized rate over the last four years, much worse than the broader bank industry.

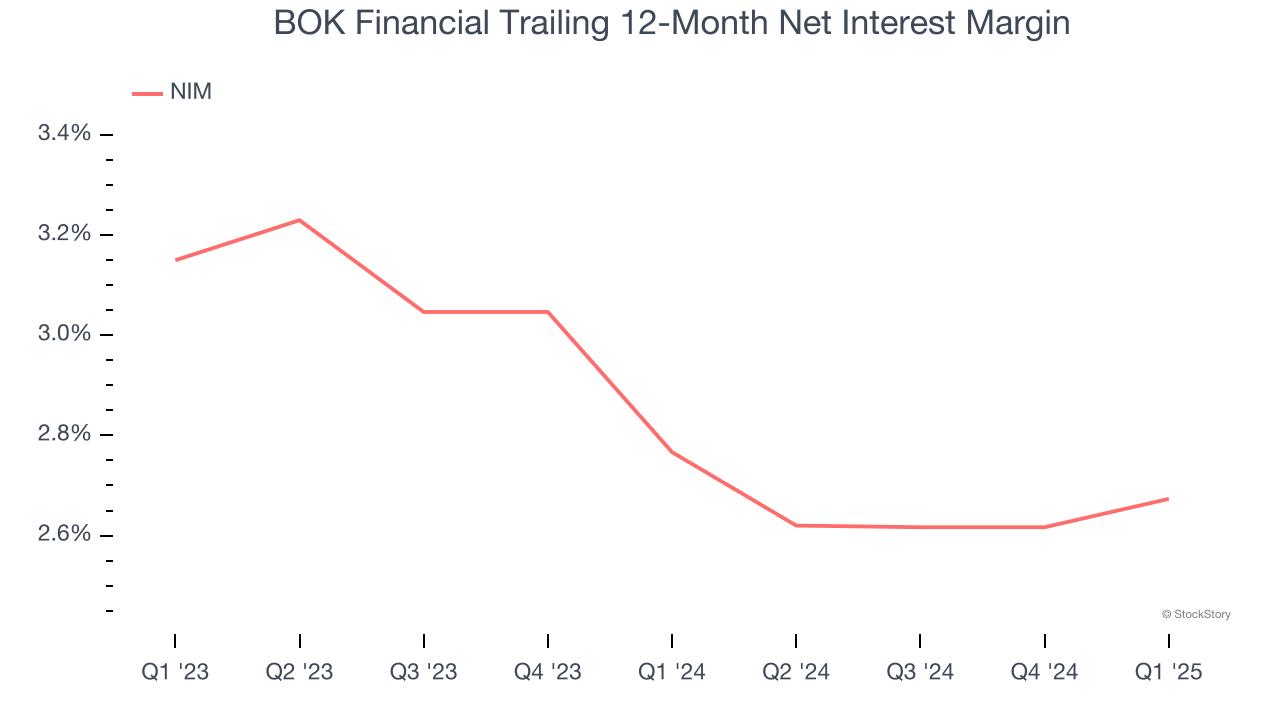

3. Net Interest Margin Dropping

Revenue is a fine reference point for banks, but net interest income and margin are better indicators of business quality for banks because they’re balance sheet-driven businesses that leverage their assets to generate profits.

Over the past two years, BOK Financial’s net interest margin averaged 2.7%. Its margin also contracted by 47.7 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean BOK Financial either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

Final Judgment

BOK Financial’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 1× forward P/B (or $96.95 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere. We’d recommend looking at a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.