Over the past six months, Cathay General Bancorp’s shares (currently trading at $44.78) have posted a disappointing 12.1% loss while the S&P 500 was flat. This may have investors wondering how to approach the situation.

Is now the time to buy Cathay General Bancorp, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Cathay General Bancorp Not Exciting?

Despite the more favorable entry price, we're swiping left on Cathay General Bancorp for now. Here are three reasons why we avoid CATY and a stock we'd rather own.

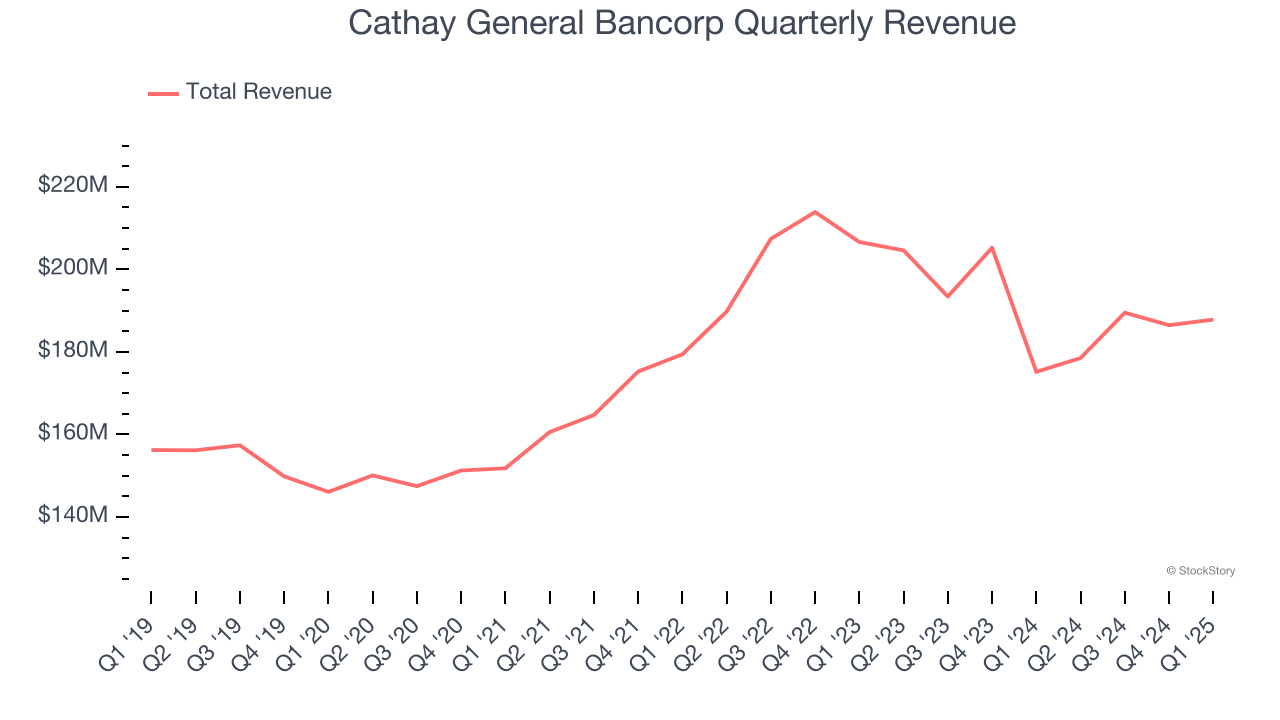

1. Long-Term Revenue Growth Disappoints

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

Unfortunately, Cathay General Bancorp’s 4% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the bank sector.

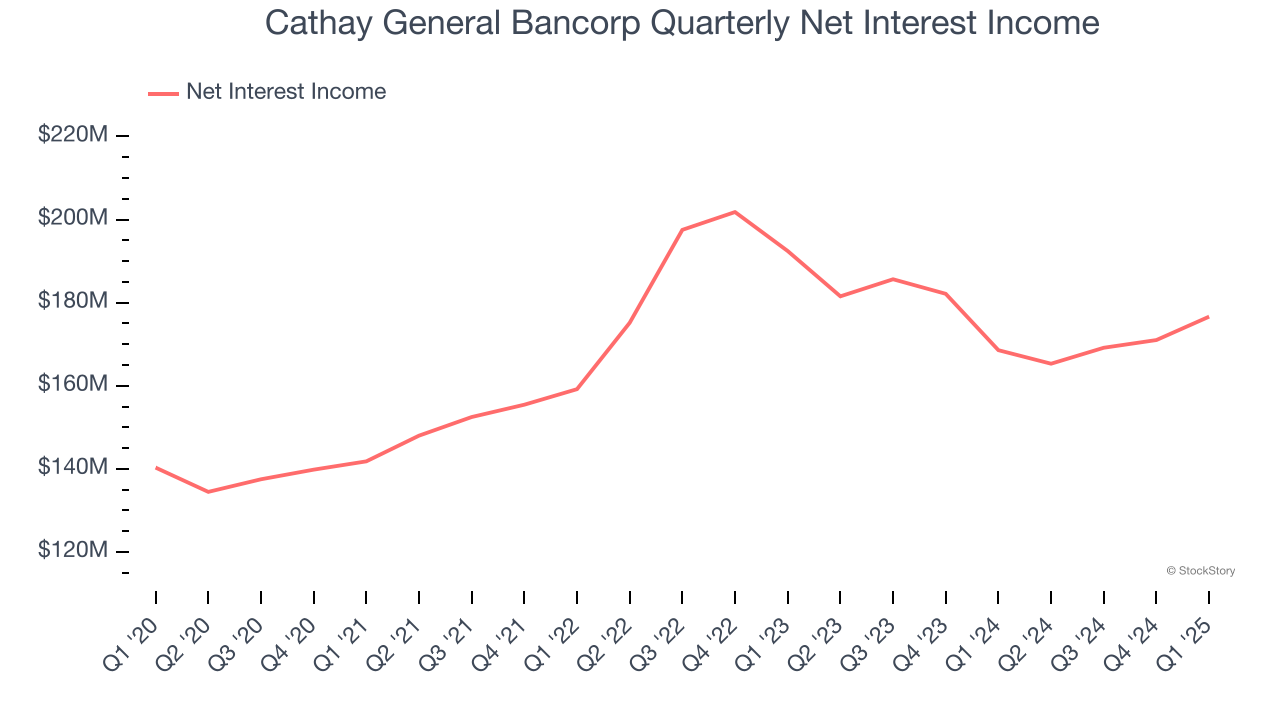

2. Net Interest Income Points to Soft Demand

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

Cathay General Bancorp’s net interest income has grown at a 5.4% annualized rate over the last four years, worse than the broader banking industry.

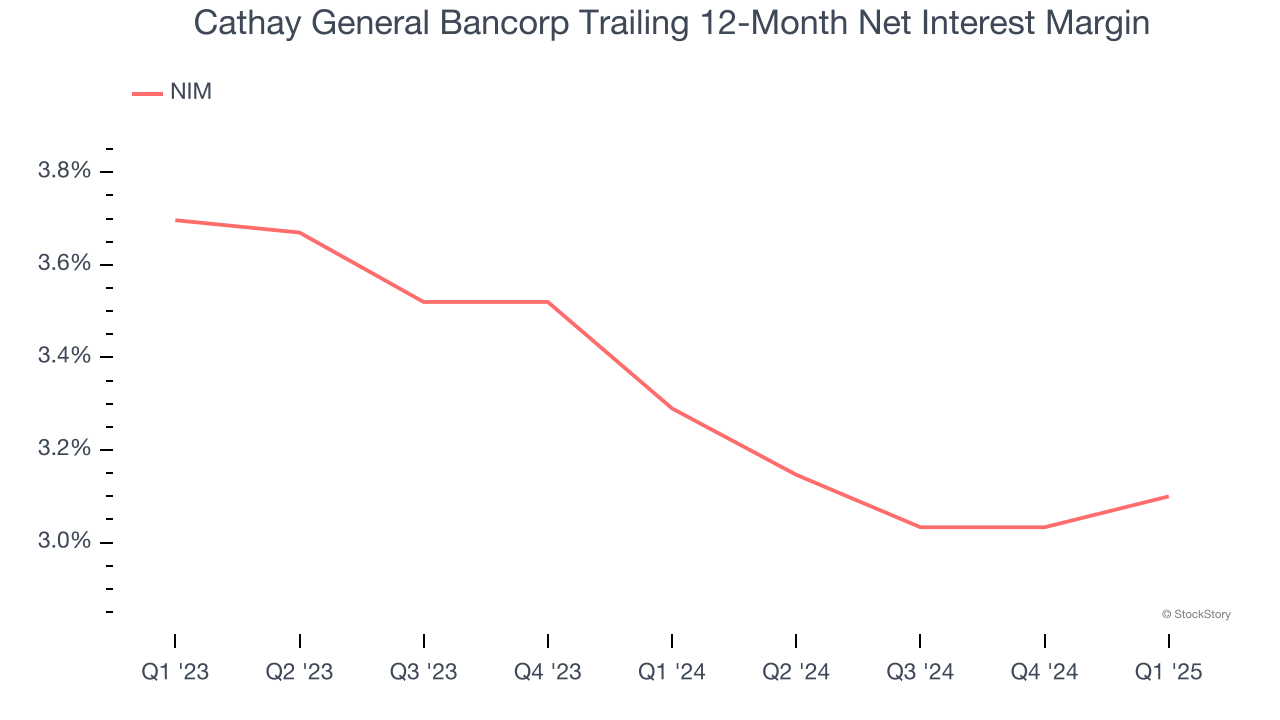

3. Net Interest Margin Dropping

Net interest margin represents how much a bank earns in relation to its outstanding loans. It’s one of the most important metrics to track because it shows how a bank’s loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, Cathay General Bancorp’s net interest margin averaged 3.2%. Its margin also contracted by 59.7 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income and means Cathay General Bancorp is either investing in worse-performing loans (if sticking in the same risk tier), seeing its cost of capital rise, or facing competition that is eating into its premiums.

Final Judgment

Cathay General Bancorp isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 1× forward P/B (or $44.78 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.