Doughnut chain Krispy Kreme (NASDAQ: DNUT) missed Wall Street’s revenue expectations in Q1 CY2025, with sales falling 15.3% year on year to $375.2 million. Its non-GAAP loss of $0.05 per share was in line with analysts’ consensus estimates.

Is now the time to buy Krispy Kreme? Find out by accessing our full research report, it’s free.

Krispy Kreme (DNUT) Q1 CY2025 Highlights:

- Revenue: $375.2 million vs analyst estimates of $383.8 million (15.3% year-on-year decline, 2.2% miss)

- Adjusted EPS: -$0.05 vs analyst estimates of -$0.05 (in line)

- Adjusted EBITDA: $23.98 million vs analyst estimates of $29.26 million (6.4% margin, 18.1% miss)

- Operating Margin: -5.4%, down from 2.7% in the same quarter last year

- Free Cash Flow was -$46.73 million compared to -$46.77 million in the same quarter last year

- Market Capitalization: $739 million

“Our ability to become a bigger Krispy Kreme requires that we become better, and we are taking swift and decisive action to pay down debt, de-leverage the balance sheet and drive sustainable, profitable growth,” said Krispy Kreme CEO, Josh Charlesworth.

Company Overview

Famous for its Original Glazed doughnuts and parent company of Insomnia Cookies, Krispy Kreme (NASDAQ: DNUT) is one of the most beloved and well-known fast-food chains in the world.

Sales Growth

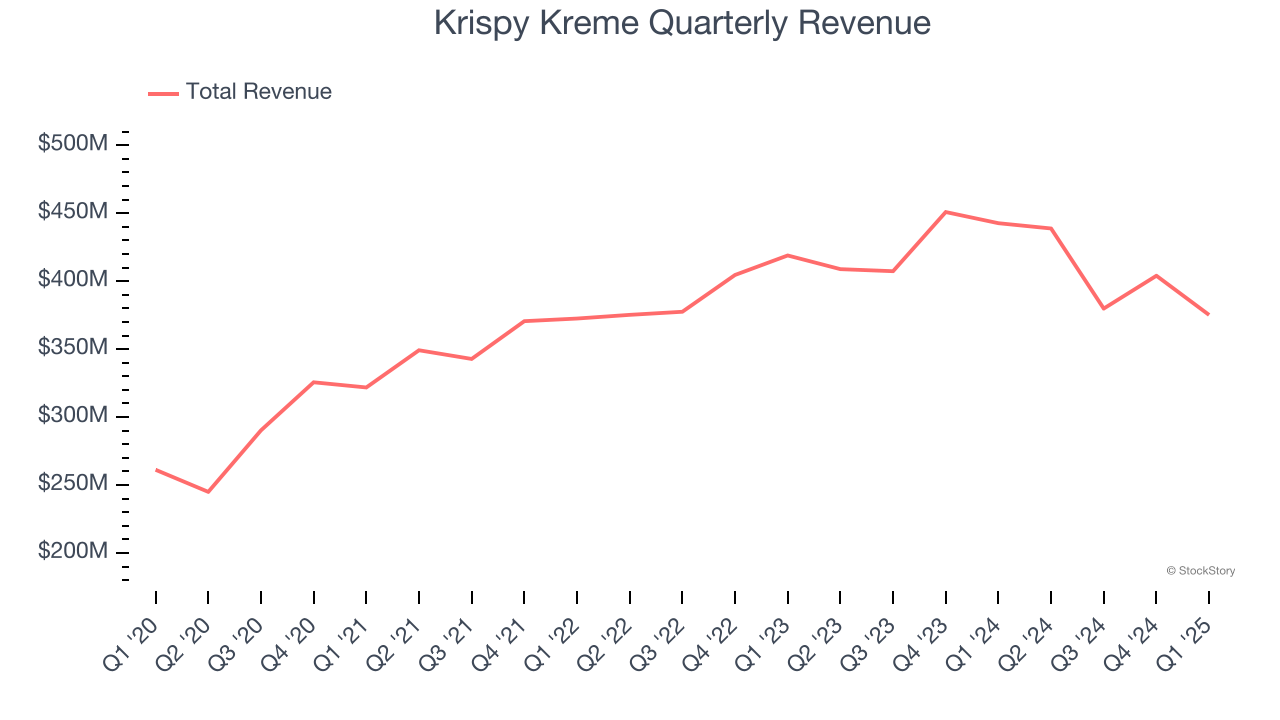

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.60 billion in revenue over the past 12 months, Krispy Kreme is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, Krispy Kreme grew its sales at a decent 10% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new restaurants and expanded its reach.

This quarter, Krispy Kreme missed Wall Street’s estimates and reported a rather uninspiring 15.3% year-on-year revenue decline, generating $375.2 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months, a deceleration versus the last five years. This projection doesn't excite us and implies its menu offerings will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

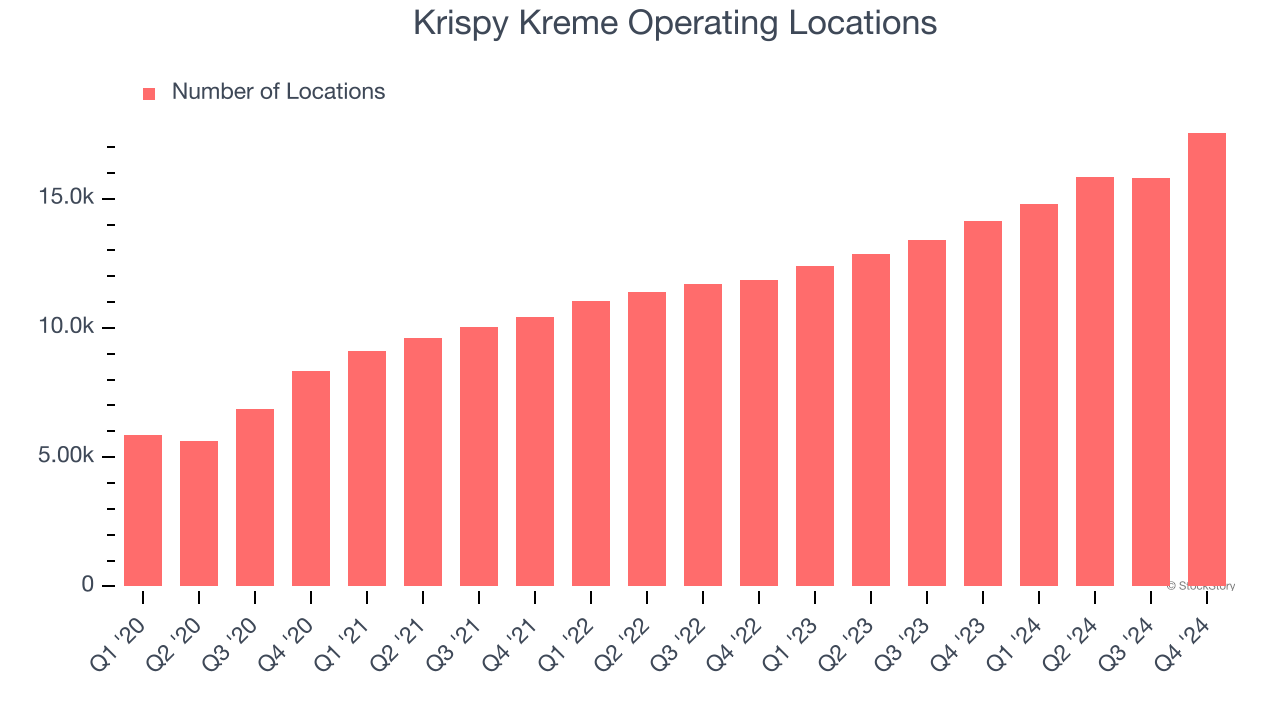

Number of Restaurants

The number of dining locations a restaurant chain operates is a critical driver of how quickly company-level sales can grow.

Over the last two years, Krispy Kreme opened new restaurants at a rapid clip by averaging 18.8% annual growth, among the fastest in the restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Note that Krispy Kreme reports its restaurant count intermittently, so some data points are missing in the chart below.

Key Takeaways from Krispy Kreme’s Q1 Results

We struggled to find many positives in these results. Its EBITDA missed significantly and its revenue fell short of Wall Street’s estimates. Overall, this was a bad quarter. The stock traded down 24.5% to $3.25 immediately after reporting.

Krispy Kreme underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.