Over the past six months, Red Rock Resorts’s stock price fell to $44.87. Shareholders have lost 18% of their capital, disappointing when considering the S&P 500 was flat. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Red Rock Resorts, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even with the cheaper entry price, we don't have much confidence in Red Rock Resorts. Here are three reasons why we avoid RRR and a stock we'd rather own.

Why Do We Think Red Rock Resorts Will Underperform?

Founded in 1976, Red Rock Resorts (NASDAQ: RRR) operates a range of casino resorts and entertainment properties, primarily in the Las Vegas metropolitan area.

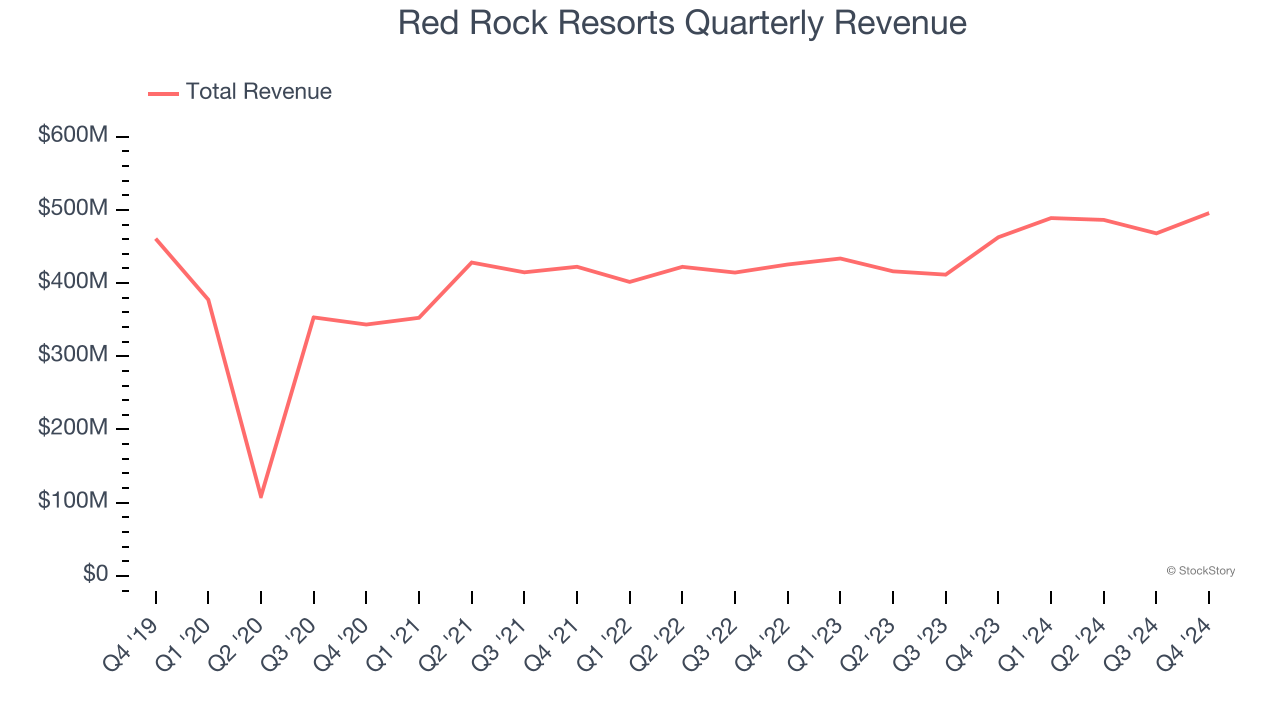

1. Long-Term Revenue Growth Flatter Than a Pancake

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Red Rock Resorts struggled to consistently increase demand as its $1.94 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of poor business quality.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Red Rock Resorts’s revenue to stall, a deceleration versus its 8% annualized growth for the past two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

3. Cash Flow Margin Set to Decline

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the next year, analysts predict Red Rock Resorts’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 13.6% for the last 12 months will decrease to 4.1%.

Final Judgment

We see the value of companies helping consumers, but in the case of Red Rock Resorts, we’re out. After the recent drawdown, the stock trades at 22× forward price-to-earnings (or $44.87 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are better investments elsewhere. We’d suggest looking at a top digital advertising platform riding the creator economy.

Stocks We Like More Than Red Rock Resorts

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.