Over the past six months, Insulet has been a great trade. While the S&P 500 was flat, the stock price has climbed by 14.6% to $265.87 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Following the strength, is PODD a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Is PODD a Good Business?

Revolutionizing diabetes care with its tubeless "Pod" technology, Insulet (NASDAQ: PODD) develops and manufactures innovative insulin delivery systems for people with diabetes, primarily through its Omnipod product line.

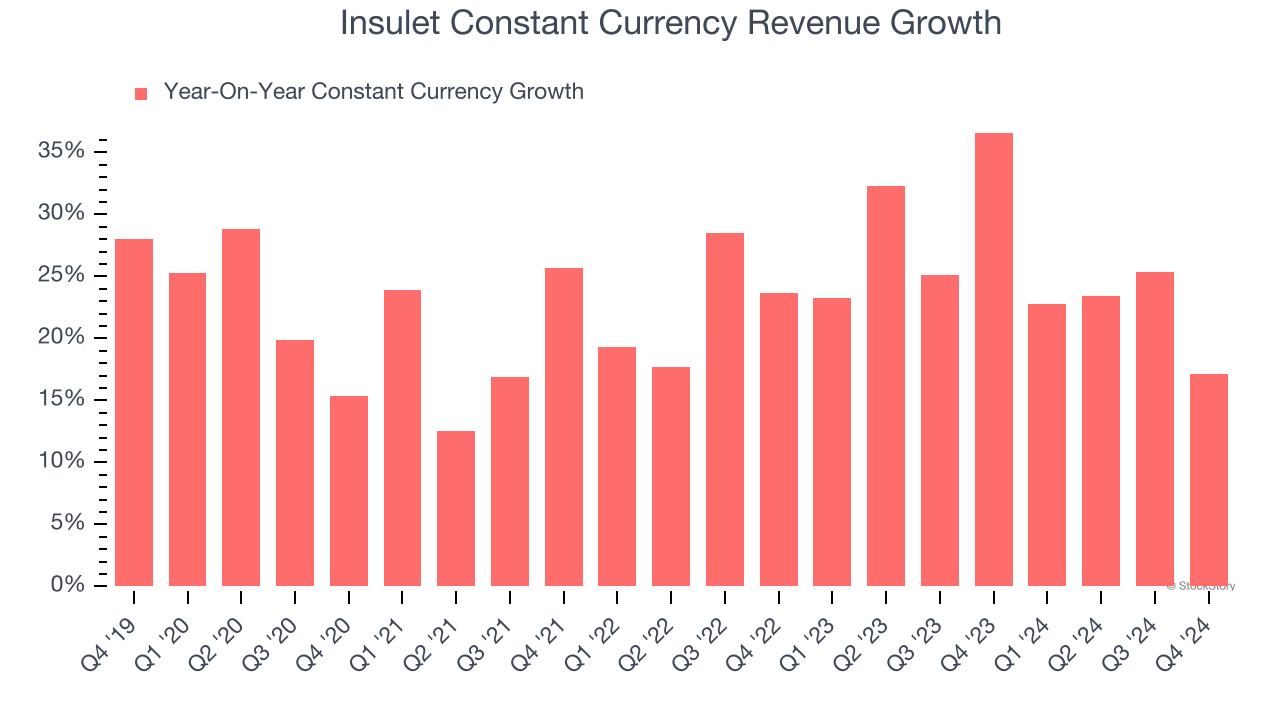

1. Constant Currency Revenue Propels Growth

In addition to reported revenue, constant currency revenue is a useful data point for analyzing Patient Monitoring companies. This metric excludes currency movements, which are outside of Insulet’s control and are not indicative of underlying demand.

Over the last two years, Insulet’s constant currency revenue averaged 25.7% year-on-year growth. This performance was fantastic and shows it can expand quickly on a global scale regardless of the macroeconomic environment.

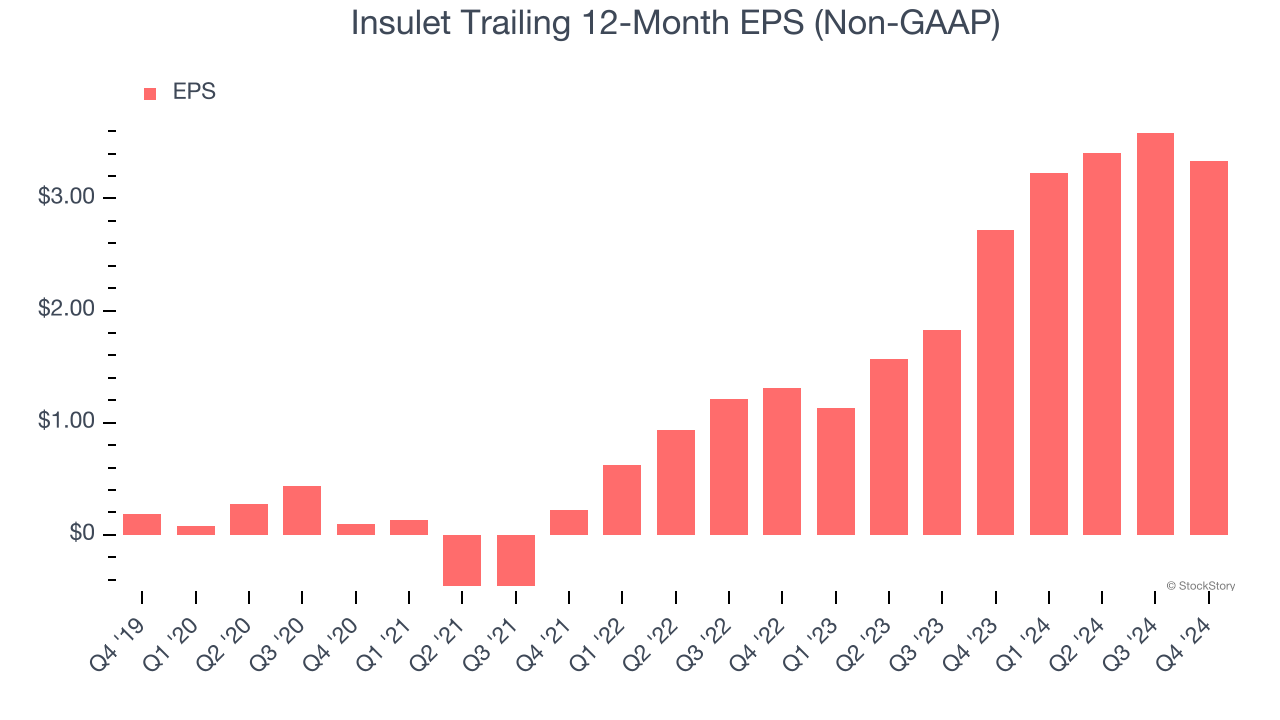

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Insulet’s EPS grew at an astounding 78% compounded annual growth rate over the last five years, higher than its 22.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

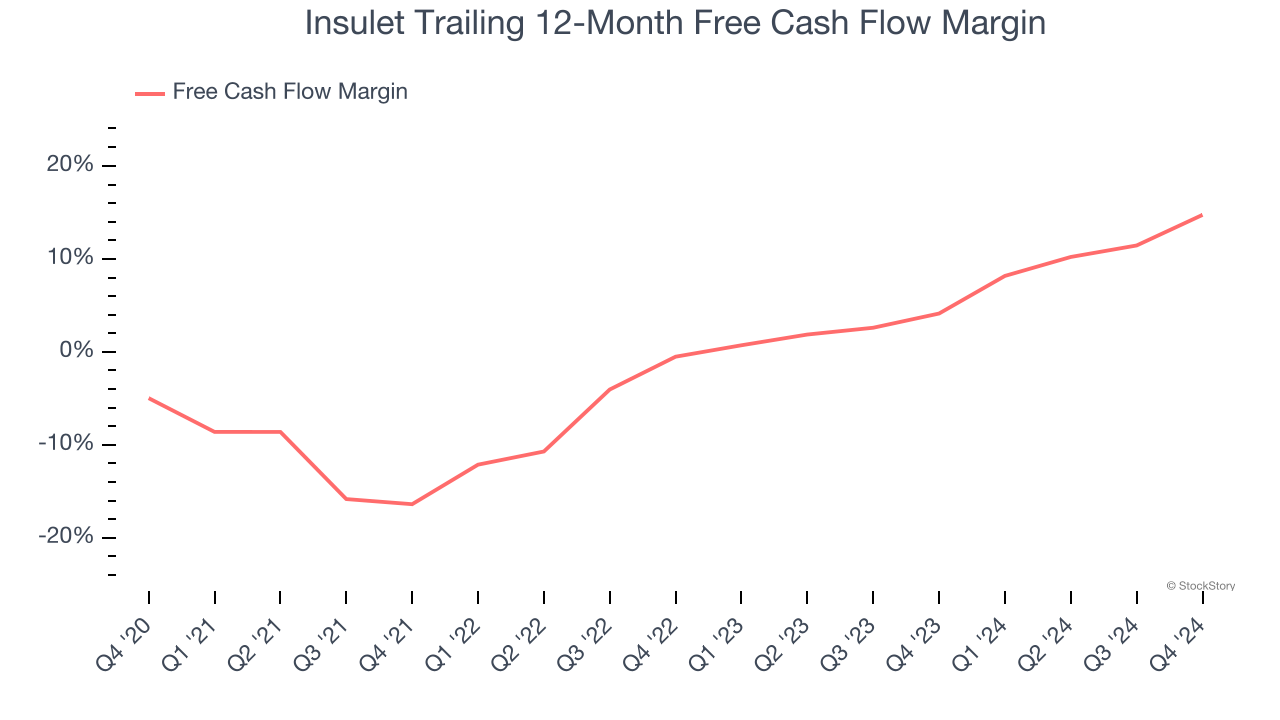

3. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Insulet’s margin expanded by 19.7 percentage points over the last five years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Insulet’s free cash flow margin for the trailing 12 months was 14.7%.

Final Judgment

These are just a few reasons why we think Insulet is a high-quality business, and with its shares outperforming the market lately, the stock trades at 68× forward price-to-earnings (or $265.87 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Insulet

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.