Over the past six months, BJ’s stock price fell to $38.37. Shareholders have lost 12.4% of their capital, which is disappointing considering the S&P 500 has climbed by 13.6%. This might have investors contemplating their next move.

Is there a buying opportunity in BJ's, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Why Do We Think BJ's Will Underperform?

Even though the stock has become cheaper, we're swiping left on BJ's for now. Here are three reasons we avoid BJRI and a stock we'd rather own.

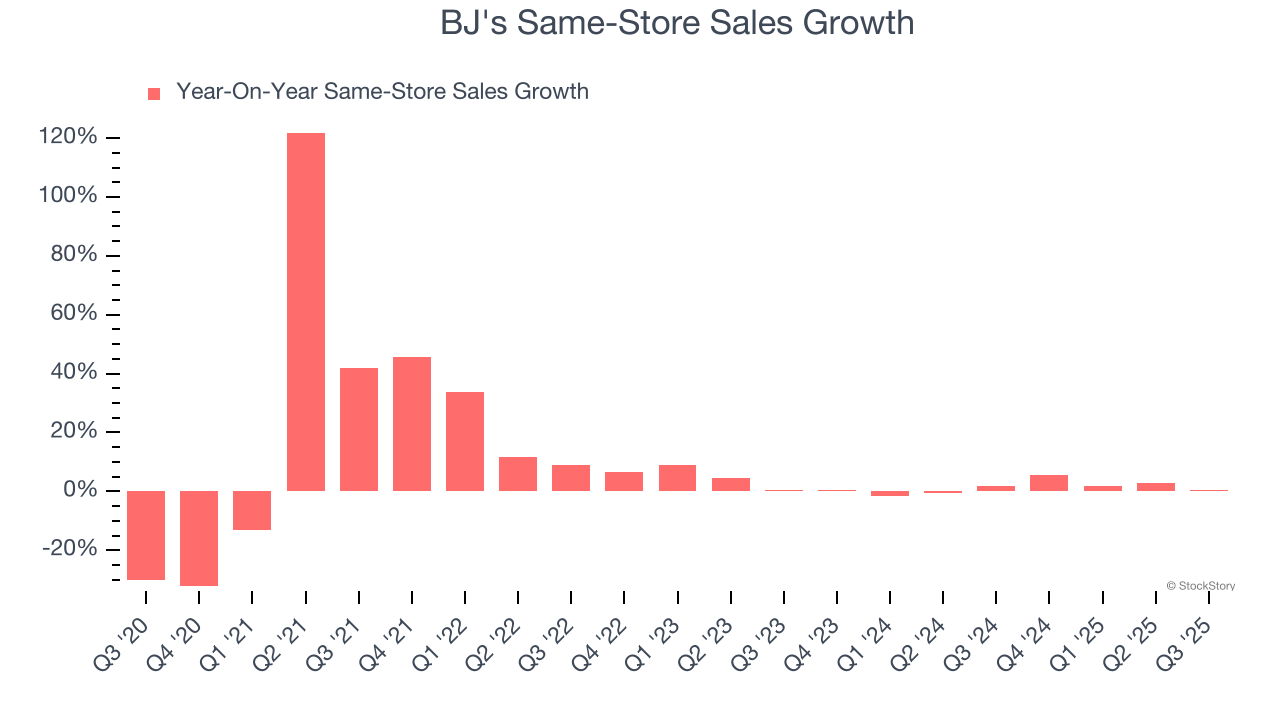

1. Same-Store Sales Falling Behind Peers

Same-store sales show the change in sales at restaurants open for at least a year. This is a key performance indicator because it measures organic growth.

BJ’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.3% per year.

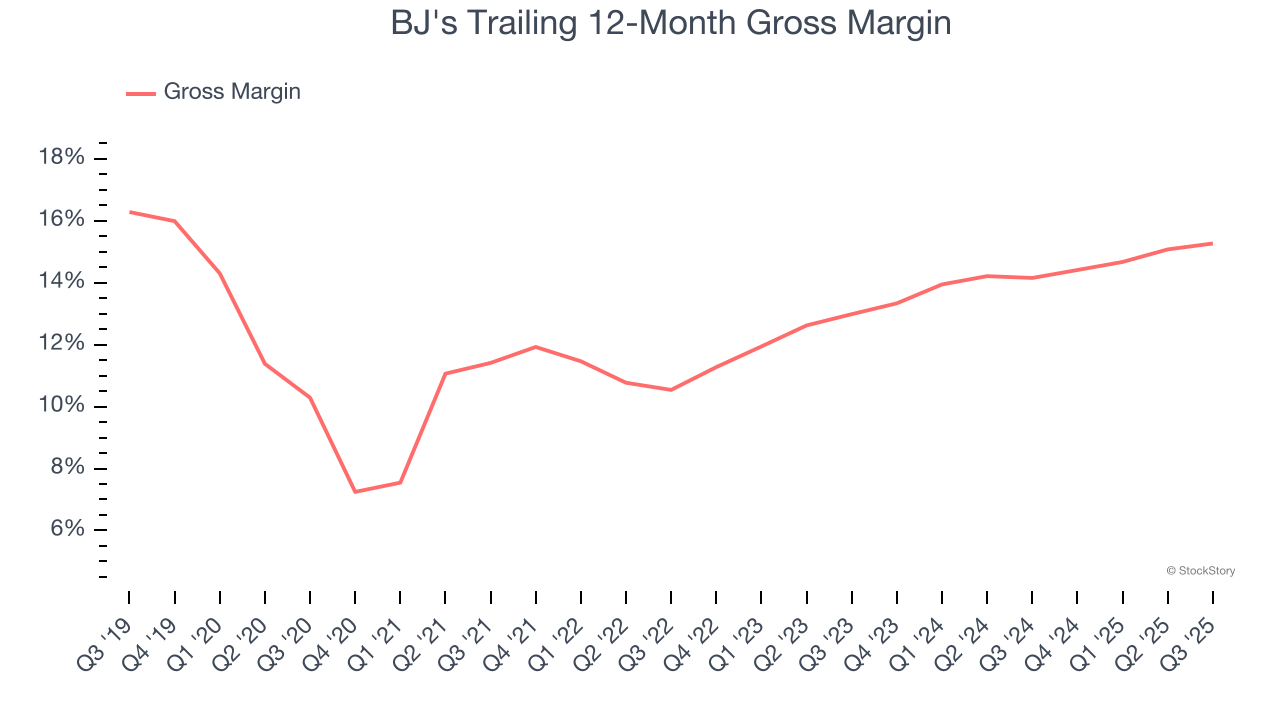

2. Low Gross Margin Reveals Weak Structural Profitability

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate pricing power and differentiation, whether it be the dining experience or quality and taste of food.

BJ's has bad unit economics for a restaurant company, signaling it operates in a competitive market and has little room for error if demand unexpectedly falls. As you can see below, it averaged a 14.7% gross margin over the last two years. Said differently, BJ's had to pay a chunky $85.28 to its suppliers for every $100 in revenue.

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

BJ's historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3%, lower than the typical cost of capital (how much it costs to raise money) for restaurant companies.

Final Judgment

BJ's doesn’t pass our quality test. Following the recent decline, the stock trades at 17.2× forward P/E (or $38.37 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are superior stocks to buy right now. We’d recommend looking at a top digital advertising platform riding the creator economy.

High-Quality Stocks for All Market Conditions

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.