Wrapping up Q3 earnings, we look at the numbers and key takeaways for the sit-down dining stocks, including The Cheesecake Factory (NASDAQ: CAKE) and its peers.

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

The 12 sit-down dining stocks we track reported a mixed Q3. As a group, revenues were in line with analysts’ consensus estimates.

While some sit-down dining stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 2.2% since the latest earnings results.

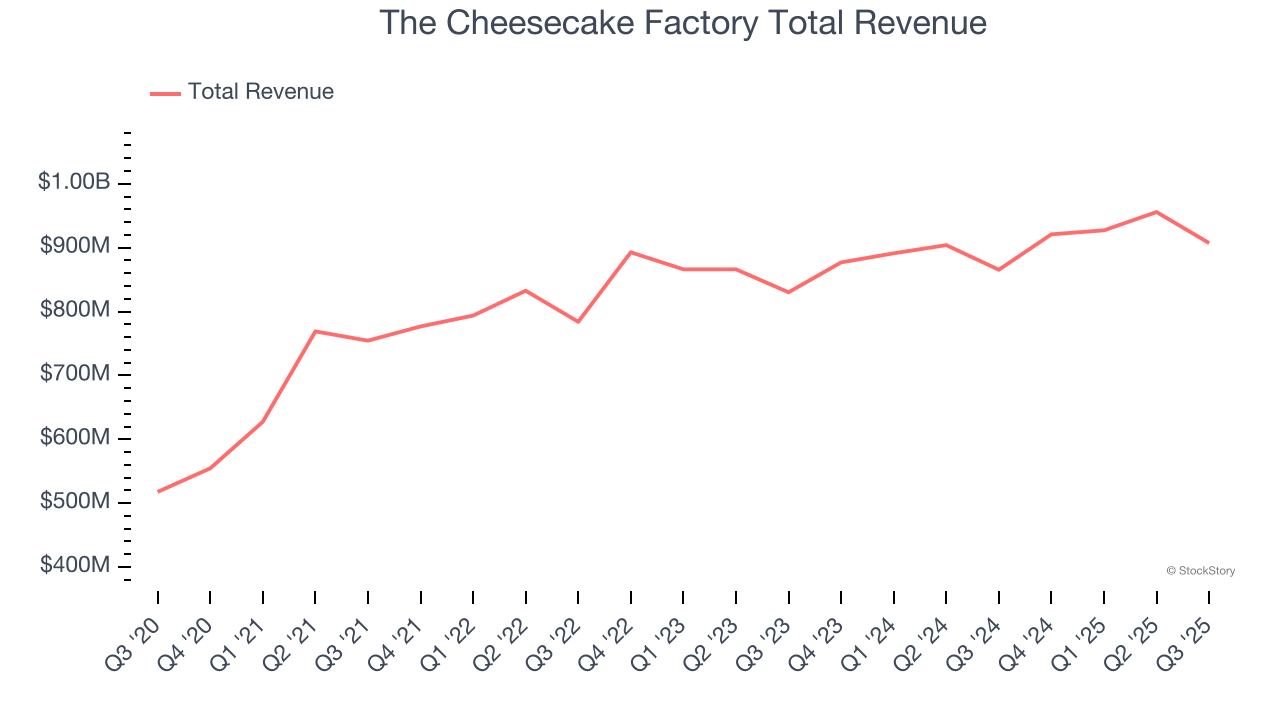

The Cheesecake Factory (NASDAQ: CAKE)

Celebrated for its delicious (and free) brown bread, gigantic portions, and delectable desserts, Cheesecake Factory (NASDAQ: CAKE) is an iconic American restaurant chain that also owns and operates a portfolio of separate restaurant brands.

The Cheesecake Factory reported revenues of $907.2 million, up 4.8% year on year. This print fell short of analysts’ expectations by 0.5%. Overall, it was a mixed quarter for the company with a beat of analysts’ EPS estimates but a slight miss of analysts’ same-store sales estimates.

“We delivered another quarter of solid results, with revenue within our guidance range and earnings and profitability finishing above the high end of our expectations,” said David Overton, Chairman and Chief Executive Officer.

Unsurprisingly, the stock is down 19.9% since reporting and currently trades at $43.51.

Read our full report on The Cheesecake Factory here, it’s free for active Edge members.

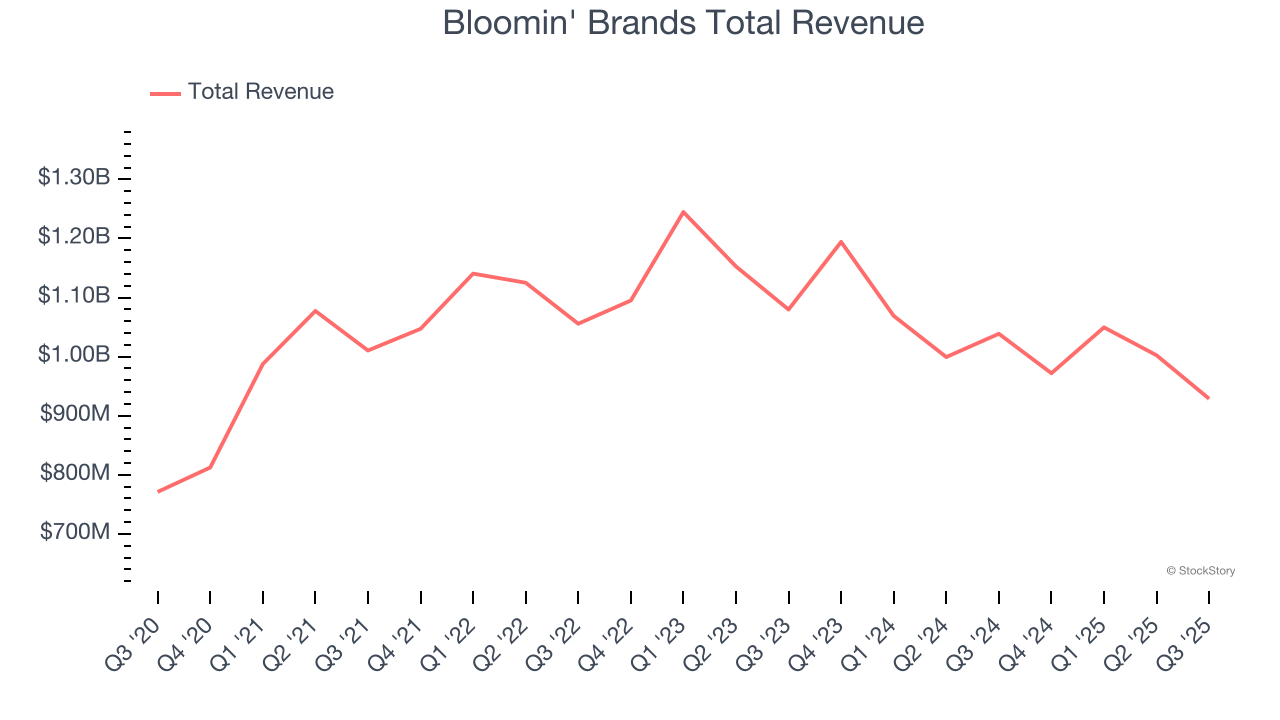

Best Q3: Bloomin' Brands (NASDAQ: BLMN)

Owner of the iconic Australian-themed Outback Steakhouse, Bloomin’ Brands (NASDAQ: BLMN) is a leading American restaurant company that owns and operates a portfolio of popular restaurant brands.

Bloomin' Brands reported revenues of $928.8 million, down 10.6% year on year, outperforming analysts’ expectations by 2.7%. The business had a stunning quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 17.6% since reporting. It currently trades at $5.96.

Is now the time to buy Bloomin' Brands? Access our full analysis of the earnings results here, it’s free for active Edge members.

Slowest Q3: Denny's (NASDAQ: DENN)

Open around the clock, Denny’s (NASDAQ: DENN) is a chain of diner restaurants serving breakfast and traditional American fare.

Denny's reported revenues of $113.2 million, up 1.3% year on year, falling short of analysts’ expectations by 3.2%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a miss of analysts’ EBITDA estimates.

Interestingly, the stock is up 49.4% since the results and currently trades at $6.14.

Read our full analysis of Denny’s results here.

Brinker International (NYSE: EAT)

Founded by Norman Brinker in Dallas, Brinker International (NYSE: EAT) is a casual restaurant chain that operates the Chili’s, Maggiano’s Little Italy, and It’s Just Wings banners.

Brinker International reported revenues of $1.35 billion, up 18.5% year on year. This result beat analysts’ expectations by 1.3%. Aside from that, it was a satisfactory quarter as it also logged an impressive beat of analysts’ same-store sales estimates but full-year revenue guidance slightly missing analysts’ expectations.

Brinker International had the weakest full-year guidance update among its peers. The stock is up 1.5% since reporting and currently trades at $126.09.

Read our full, actionable report on Brinker International here, it’s free for active Edge members.

First Watch (NASDAQ: FWRG)

Based on a nautical reference to the first work shift aboard a ship, First Watch (NASDAQ: FWRG) is a chain of breakfast and brunch restaurants whose menu is heavily-focused on eggs and griddle items such as pancakes.

First Watch reported revenues of $316 million, up 25.6% year on year. This number topped analysts’ expectations by 1.9%. Overall, it was a very strong quarter as it also recorded a solid beat of analysts’ same-store sales estimates and a solid beat of analysts’ EBITDA estimates.

First Watch delivered the fastest revenue growth among its peers. The stock is down 3.8% since reporting and currently trades at $15.24.

Read our full, actionable report on First Watch here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.