Even though Horace Mann Educators (currently trading at $45.50 per share) has gained 9.4% over the last six months, it has lagged the S&P 500’s 16.4% return during that period. This may have investors wondering how to approach the situation.

Is now the time to buy Horace Mann Educators, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

Why Is Horace Mann Educators Not Exciting?

We're sitting this one out for now. Here are three reasons we avoid HMN and a stock we'd rather own.

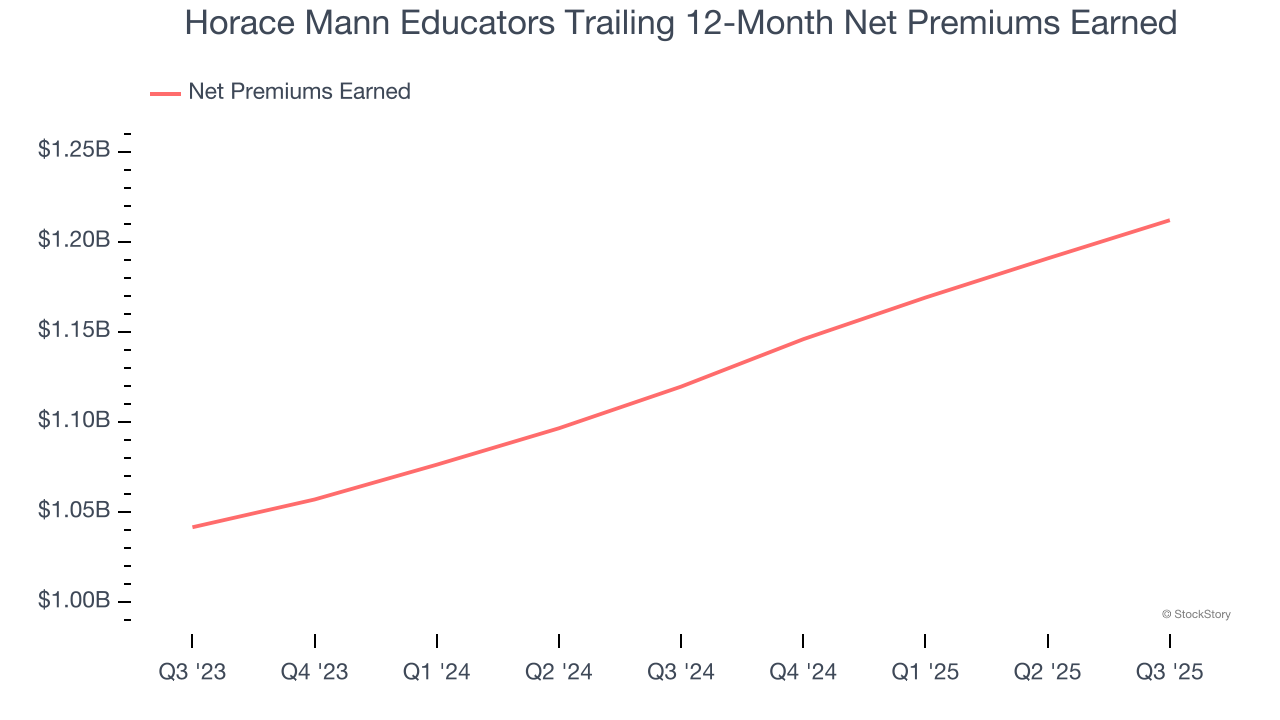

1. Net Premiums Earned Point to Soft Demand

Insurers sell policies then use reinsurance (insurance for insurance companies) to protect themselves from large losses. Net premiums earned are therefore what's collected from selling policies less what’s paid to reinsurers as a risk mitigation tool.

Horace Mann Educators’s net premiums earned has grown at a 5.3% annualized rate over the last five years, worse than the broader insurance industry and in line with its total revenue.

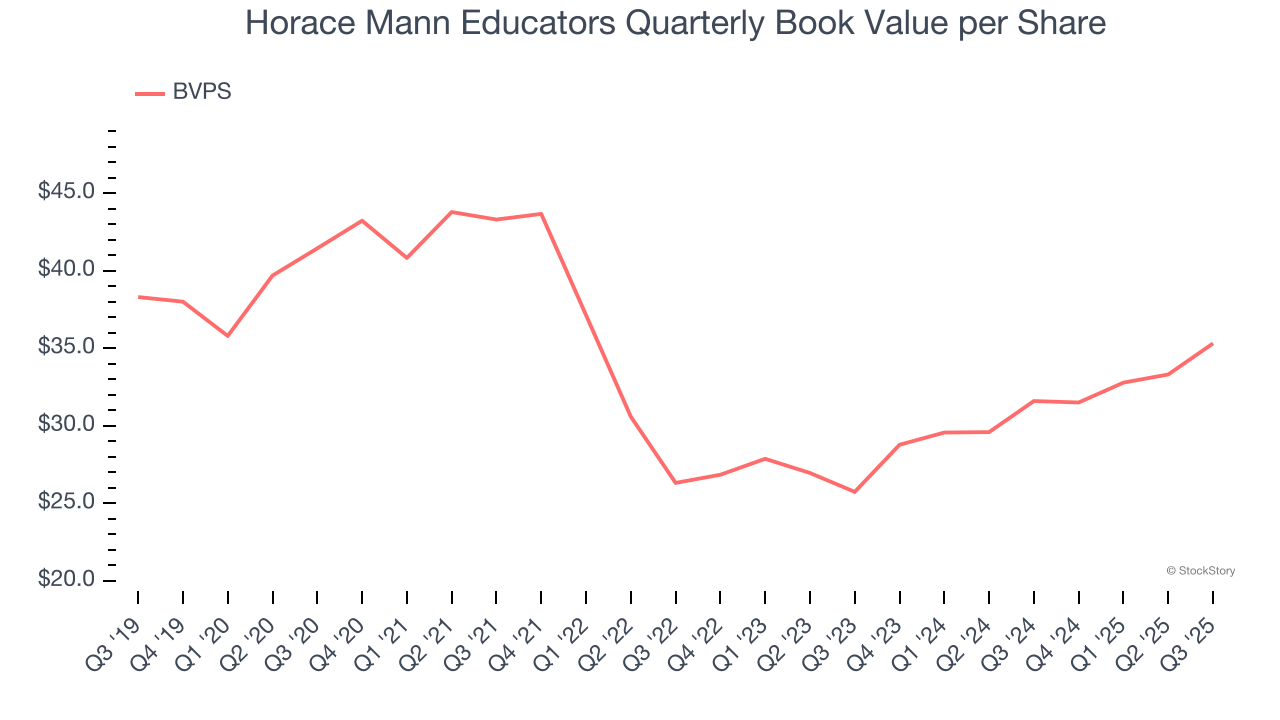

2. Steady Increase in BVPS Highlights Solid Asset Growth

In the insurance industry, book value per share (BVPS) provides a clear picture of shareholder value, as it represents the total equity backing a company’s insurance operations and growth initiatives.

Although Horace Mann Educators’s BVPS declined at a 3.2% annual clip over the last five years. the good news is that its growth inflected positive over the past two years as BVPS grew at a solid 17.1% annual clip (from $25.74 to $35.31 per share).

3. Previous Growth Initiatives Haven’t Impressed

Return on Equity, or ROE, ties everything together and is a vital metric. It tells us how much profit the insurer generates for each dollar of shareholder equity entrusted to management. Over a long period, insurers with higher ROEs tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Horace Mann Educators has averaged an ROE of 6.7%, uninspiring for a company operating in a sector where the average shakes out around 12.5%.

Final Judgment

Horace Mann Educators isn’t a terrible business, but it doesn’t pass our quality test. With its shares underperforming the market lately, the stock trades at 1.3× forward P/B (or $45.50 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at the Amazon and PayPal of Latin America.

High-Quality Stocks for All Market Conditions

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.