Although Revolve (currently trading at $22.50 per share) has gained 17.3% over the last six months, it has trailed the S&P 500’s 27.3% return during that period. This might have investors contemplating their next move.

Is there a buying opportunity in Revolve, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Do We Think Revolve Will Underperform?

We don't have much confidence in Revolve. Here are three reasons we avoid RVLV and a stock we'd rather own.

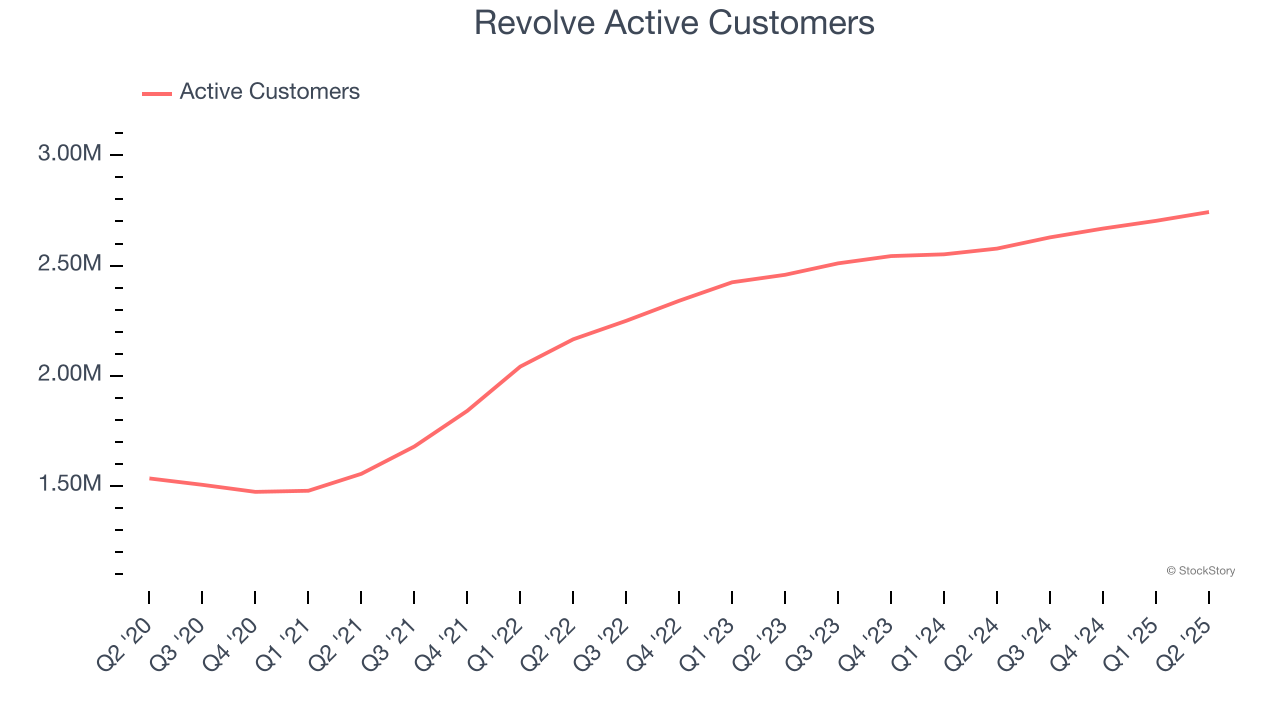

1. Change in Active Customers Points to Soft Demand

As an online retailer, Revolve generates revenue growth by expanding its number of users and the average order size in dollars.

Over the last two years, Revolve’s active customers , a key performance metric for the company, increased by 6.5% annually to 2.74 million in the latest quarter. This growth rate is slightly below average for a consumer internet business. If Revolve wants to reach the next level, it likely needs to enhance the appeal of its current offerings or innovate with new products.

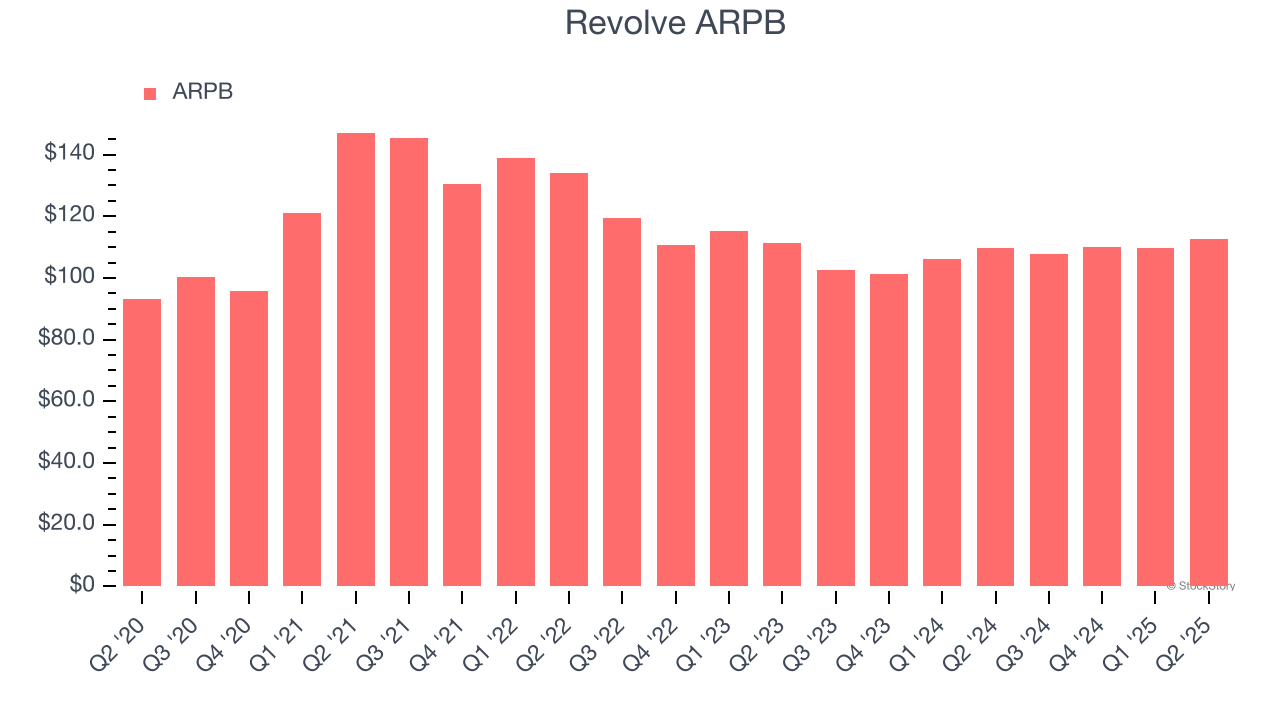

2. Customer Spending Decreases, Engagement Falling?

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much customers spend per order.

Revolve’s ARPB fell over the last two years, averaging 1.5% annual declines. This isn’t great when combined with its weaker active customers performance. If Revolve tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether buyer growth would be sustainable.

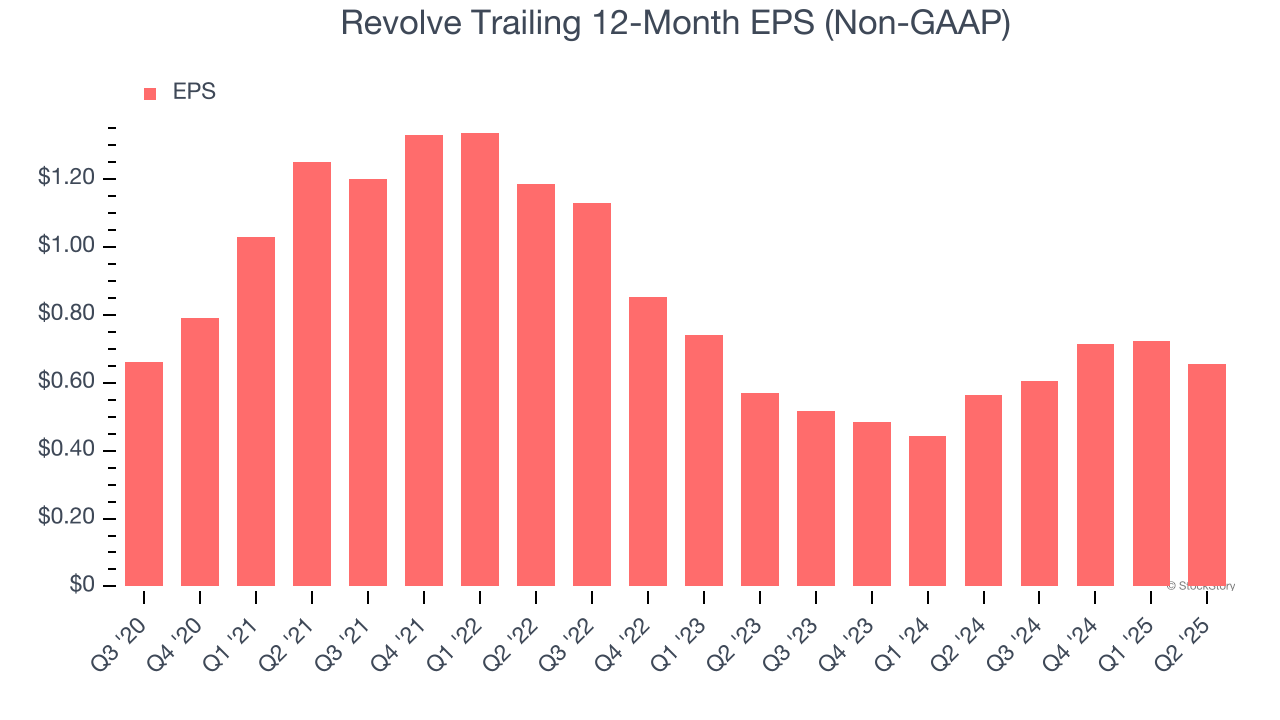

3. EPS Trending Down

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Revolve, its EPS declined by 18% annually over the last three years while its revenue grew by 3.8%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

We see the value of companies helping consumers, but in the case of Revolve, we’re out. With its shares lagging the market recently, the stock trades at 23.3× forward EV/EBITDA (or $22.50 per share). At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.