Shareholders of Arhaus would probably like to forget the past six months even happened. The stock dropped 45.1% and now trades at $10.42. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Arhaus, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.Despite the more favorable entry price, we don't have much confidence in Arhaus. Here are three reasons why there are better opportunities than ARHS and a stock we'd rather own.

Why Is Arhaus Not Exciting?

With an aesthetic that features natural materials such as reclaimed wood, Arhaus (NASDAQ: ARHS) is a high-end furniture retailer that sells everything from sofas to rugs to bookcases.

1. Less Negotiating Power with Suppliers

Arhaus is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage. On the other hand, it can grow faster because it’s working from a smaller revenue base and has more white space to build new stores.

2. Operating Margin Falling

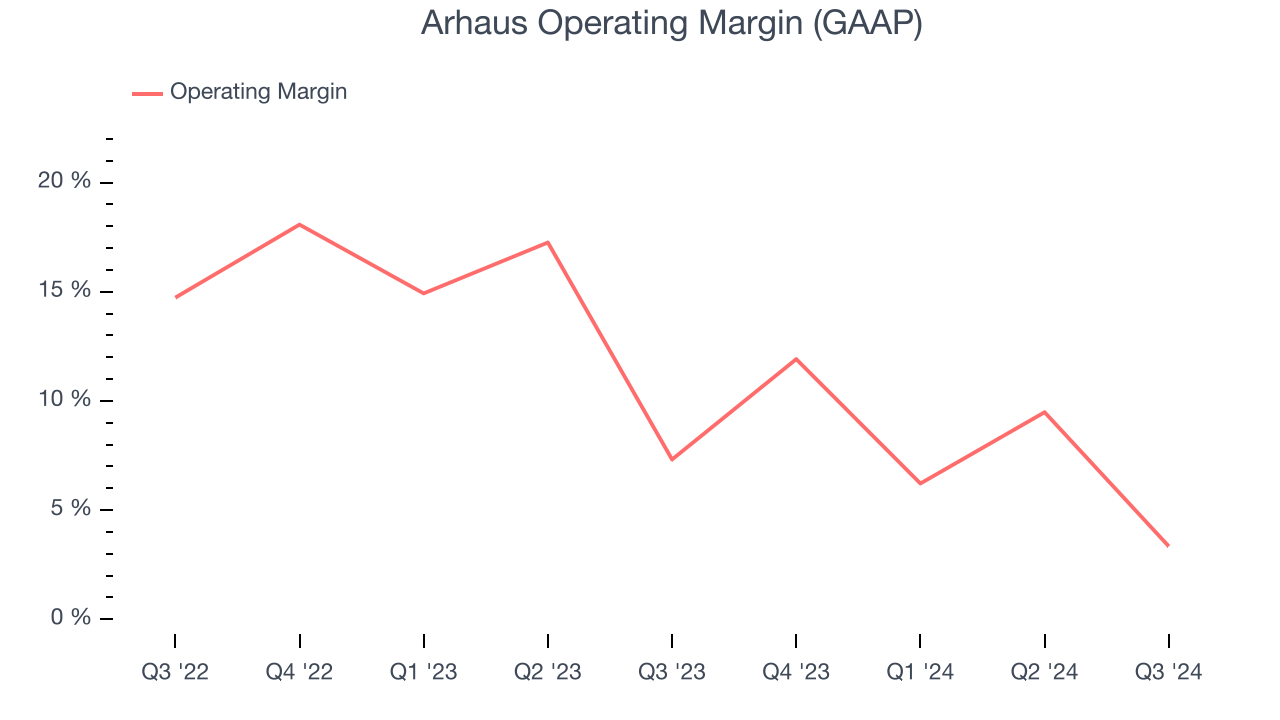

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Looking at the trend in its profitability, Arhaus’s operating margin decreased by 6.6 percentage points over the last year. Even though its historical margin is high, shareholders will want to see Arhaus become more profitable in the future. Its operating margin for the trailing 12 months was 7.8%.

3. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Arhaus’s five-year average ROIC was 2%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+. Its returns suggest it historically did a mediocre job investing in profitable growth initiatives.

Final Judgment

Arhaus isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 20.7x forward price-to-earnings (or $10.42 per share). This valuation tells us a lot of optimism is priced in - we think there are better investment opportunities out there. We’d suggest looking at Wabtec, a leading provider of locomotive services benefiting from an upgrade cycle.

Stocks We Like More Than Arhaus

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.