Let’s dig into the relative performance of H&E Equipment Services (NASDAQ: HEES) and its peers as we unravel the now-completed Q3 specialty equipment distributors earnings season.

Historically, specialty equipment distributors have boasted deep selection and expertise in sometimes narrow areas like single-use packaging or unique lighting equipment. Additionally, the industry has evolved to include more automated industrial equipment and machinery over the last decade, driving efficiencies and enabling valuable data collection. Specialty equipment distributors whose offerings keep up with these trends can take share in a still-fragmented market, but like the broader industrials sector, this space is at the whim of economic cycles that impact the capital spending and manufacturing propelling industry volumes.

The 10 specialty equipment distributors stocks we track reported a slower Q3. As a group, revenues were in line with analysts’ consensus estimates.

Thankfully, share prices of the companies have been resilient as they are up 9.6% on average since the latest earnings results.

H&E Equipment Services (NASDAQ: HEES)

Founded after recognizing a growth trend along the Mississippi River and opportunities developing in the earthmoving and construction equipment business, H&E (NASDAQ: HEES) offers machinery for companies to purchase or rent.

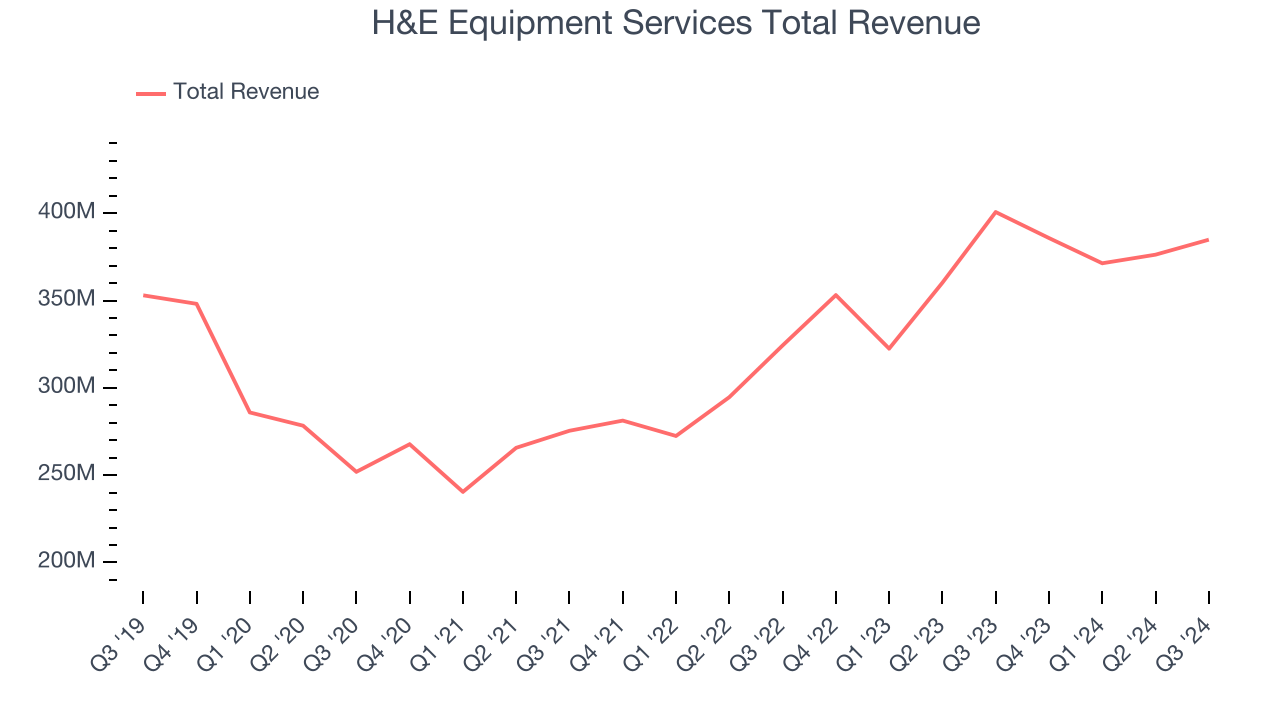

H&E Equipment Services reported revenues of $384.9 million, down 4% year on year. This print fell short of analysts’ expectations by 0.9%. Overall, it was a softer quarter for the company with a significant miss of analysts’ adjusted operating income and EPS estimates.

“Industry fundamentals in the third quarter continued to trail year-ago measures,” said Brad Barber, chief executive officer of H&E Rentals.

Interestingly, the stock is up 6.3% since reporting and currently trades at $60.20.

Read our full report on H&E Equipment Services here, it’s free.

Best Q3: Richardson Electronics (NASDAQ: RELL)

Founded in 1947, Richardson Electronics (NASDAQ: RELL) is a distributor of power grid and microwave tubes as well as consumables related to those products.

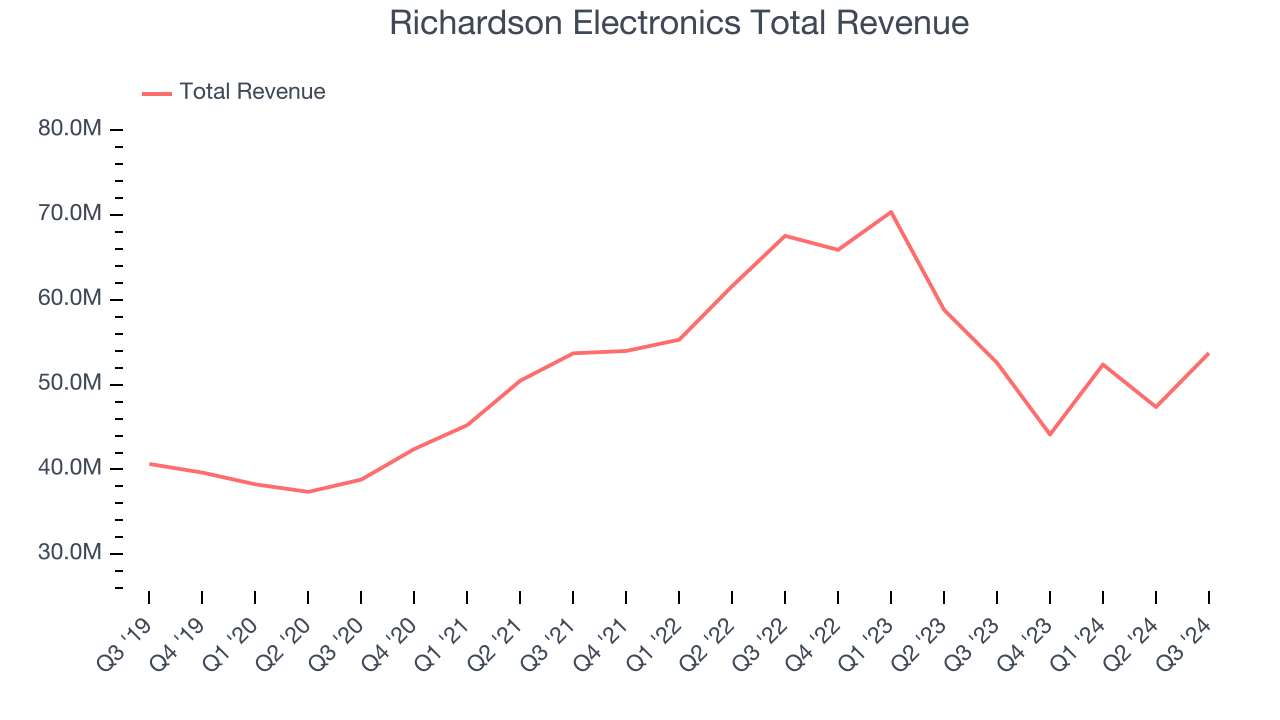

Richardson Electronics reported revenues of $53.73 million, up 2.2% year on year, outperforming analysts’ expectations by 8.7%. The business had an incredible quarter with a solid beat of analysts’ EPS and EBITDA estimates.

Richardson Electronics achieved the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 8.1% since reporting. It currently trades at $13.94.

Is now the time to buy Richardson Electronics? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Alta (NYSE: ALTG)

Founded in 1984, Alta Equipment Group (NYSE: ALTG) is a provider of industrial and construction equipment and services across the Midwest and Northeast United States.

Alta reported revenues of $448.8 million, down 3.7% year on year, falling short of analysts’ expectations by 6.5%. It was a disappointing quarter as it posted and a significant miss of analysts’ adjusted operating income estimates.

Alta delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 1.5% since the results and currently trades at $7.91.

Read our full analysis of Alta’s results here.

SiteOne (NYSE: SITE)

Known for distributing John Deere tractors and LESCO turf care products, SiteOne Landscape Supply (NYSE: SITE) provides landscaping products and services to professionals, including irrigation, lighting, and nursery supplies.

SiteOne reported revenues of $1.21 billion, up 5.6% year on year. This print topped analysts’ expectations by 1.4%. However, it was a slower quarter as it produced full-year EBITDA guidance missing analysts’ expectations.

The stock is up 7.8% since reporting and currently trades at $154.07.

Read our full, actionable report on SiteOne here, it’s free.

Hudson Technologies (NASDAQ: HDSN)

Founded in 1991, Hudson Technologies (NASDAQ: HDSN) specializes in refrigerant services and solutions, providing refrigerant sales, reclamation, and recycling.

Hudson Technologies reported revenues of $61.94 million, down 19% year on year. This result came in 6.3% below analysts' expectations. All in all, it was a slower quarter for the company.

Hudson Technologies had the slowest revenue growth among its peers. The stock is down 21.8% since reporting and currently trades at $5.94.

Read our full, actionable report on Hudson Technologies here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.