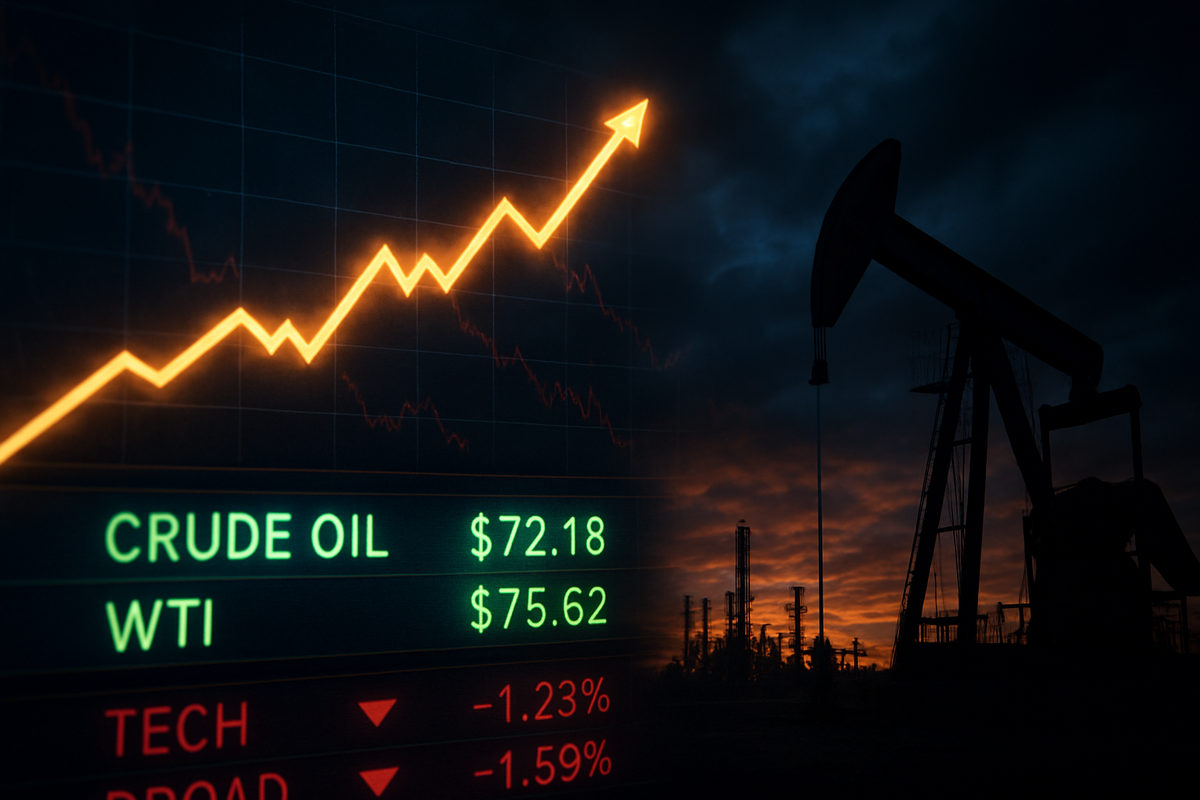

As the final trading days of 2025 unfold, a stark divergence has emerged on Wall Street: energy prices are climbing steadily while the broader equity markets succumb to a wave of year-end selling. While the S&P 500 and Nasdaq Composite have retreated from their autumn highs, crude oil has found a second wind, with Brent crude pushing past $61 per barrel and West Texas Intermediate (WTI) nearing $58. This decoupling highlights a growing "risk-off" sentiment where investors are fleeing high-growth sectors in favor of the tangible, albeit volatile, security of the energy complex.

The immediate implications are clear: the "Santa Claus rally" that many anticipated has been replaced by a defensive rotation. As inflation remains stickier than the Federal Reserve’s targets—hovering near 2.7%—and geopolitical tensions flare across multiple continents, the energy sector is acting as a rare sanctuary. However, for the broader market, the combination of rising fuel costs and falling stock prices creates a "double squeeze" on consumer sentiment and corporate margins as the calendar turns to 2026.

Geopolitical Friction and OPEC+ Discipline Drive the Surge

The current spike in oil prices is not a result of a sudden boom in global demand, but rather a confluence of supply-side shocks and calculated production maneuvers. Throughout December 2025, a series of geopolitical escalations have reintroduced a significant risk premium into the market. U.S. military strikes against ISIS targets in Nigeria—a critical producer of 1.5 million barrels per day—coupled with intensified Saudi Arabian airstrikes in Yemen, have left traders wary of sudden disruptions. Furthermore, aggressive rhetoric from Tehran regarding a "full-scale war" with Western interests has placed the Strait of Hormuz back at the center of global energy anxiety.

Leading up to this moment, the market had been bracing for a supply glut in 2026. However, during the early December OPEC+ ministerial meetings, the alliance led by Saudi Arabia and Russia executed a strategic pivot. The eight core members agreed to suspend all planned production increases for the first quarter of 2026, effectively signaling that they would prioritize price stability over regaining market share. This "firm pause" on output hikes surprised many analysts who expected the group to let more oil flow to counter non-OPEC production growth.

Initial market reactions were swift. While the tech-heavy indices began their slide in mid-December, the energy sector decoupled on December 22nd, following reports of the OPEC+ production freeze. Since then, oil has climbed nearly 8%, even as the broader market has shed 4% of its value. This divergence is being fueled by institutional investors who are closing out profitable positions in tech and crypto to hedge their portfolios with energy futures and large-cap oil equities.

Winners and Losers in a Fragmented Market

The primary beneficiaries of this year-end shift are the "Supermajors" and large-cap domestic producers. ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) have seen their share prices trend upward against the market tide, bolstered by their disciplined capital expenditure and robust dividend yields. Occidental Petroleum (NYSE: OXY) has also outperformed, as its heavy focus on U.S. shale production makes it a preferred vehicle for investors looking to avoid the complexities of overseas logistics during times of maritime tension. These companies are entering 2026 with strengthened balance sheets and the ability to fund massive buyback programs even if the broader economy cools.

Conversely, the losers in this environment are the high-valuation growth stocks that dominated the first half of 2025. Nvidia (NASDAQ: NVDA) and Tesla (NASDAQ: TSLA) have faced significant selling pressure as investors lock in gains. The logic is twofold: rising oil prices act as a "tax" on the consumer, potentially slowing the adoption of expensive tech and EVs, while the Fed’s "higher for longer" interest rate stance—driven by sticky energy-related inflation—reduces the present value of future earnings for these growth giants.

The financial sector is also feeling the heat, particularly those with heavy exposure to the digital asset space. Coinbase (NASDAQ: COIN) has struggled as a crackdown by China’s central bank on virtual currency speculation sent Bitcoin tumbling below $87,000. When combined with the broader market's "risk-off" mood, crypto-linked firms are seeing the liquidity that fueled their 2025 gains evaporate in favor of the "old economy" energy trade.

A Return to Defensive Fundamentals

The current market slide is more than just year-end profit-taking; it represents a fundamental shift in the 2025 narrative. For much of the year, the market was driven by the "AI Revolution" and the expectation of a soft landing with rapid rate cuts. However, as 2026 approaches, that optimism is being tempered by the reality of a fragmented global trade environment. The rise in oil prices alongside a market dip is a classic "stagflationary" signal that hasn't been seen with this intensity since 2022.

This event fits into a broader trend of "energy security" becoming a primary driver of national policy. The recent infrastructure attacks in the Russia-Ukraine conflict have proven that energy assets remain the primary targets in modern warfare, ensuring that a geopolitical premium will likely remain embedded in oil prices for the foreseeable future. Furthermore, the Federal Reserve's leadership transition—with names like Kevin Warsh and Kevin Hassett being discussed—has added a layer of monetary uncertainty that makes the predictable cash flows of energy companies even more attractive compared to the speculative nature of tech.

Historically, when oil prices rise during a market downturn, it often precedes a period of economic consolidation. Investors are looking back at the 1970s and the early 2000s as precedents where energy outperformed for years while the rest of the market moved sideways. This "sector rotation" suggests that the era of "easy money" and tech dominance may be yielding to a more commodity-centric investment cycle.

The Road to 2026: Pivots and Scenarios

Looking ahead to the first quarter of 2026, the market faces two distinct paths. In the short term, the OPEC+ production pause should keep a floor under oil prices, potentially pushing Brent toward the $70 mark if Middle Eastern tensions do not subside. For energy companies, this provides a window to maximize free cash flow. However, if these high energy prices persist, they may eventually destroy demand, leading to a sharper economic slowdown that could force the Fed to cut rates regardless of inflation—a move that would be seen as a "emergency pivot" rather than a planned easing.

Strategic adaptations are already underway. Many industrial firms are increasing their hedging activities to lock in current fuel prices, fearing a further spike in the new year. Meanwhile, the energy sector itself is pivoting toward "maximum sustainable production capacity" assessments, as mandated by the new OPEC+ framework. This transparency could lead to a more stable, albeit higher-priced, energy market in the long run, but the transition period will be marked by extreme volatility.

The most likely scenario for the coming months is a "bumpy transition." Investors should prepare for a market where the energy sector acts as a volatility dampener for diversified portfolios. However, the risk remains that a significant escalation in the Iran-Israel conflict or a sudden collapse in Chinese demand could send oil prices in either direction with violent speed, further destabilizing an already jittery equity market.

Final Assessment: A Cautious Horizon

The final week of 2025 serves as a potent reminder that the global economy remains tethered to fossil fuels, despite the rapid advancements in technology and renewable energy. The core takeaway for investors is that the "Goldilocks" environment of low inflation and high growth has hit a significant roadblock. Energy is no longer just a sector; it is once again a primary risk factor that dictates the direction of the entire market.

Moving forward, the market will likely remain in a state of "cautious observation." The key indicators to watch in the coming months will be the official appointment of the new Federal Reserve Chair and the actual production numbers coming out of the OPEC+ alliance in January. If the "energy-up, market-down" trend persists into the new year, it will signal a deeper structural shift in the global economy that requires a complete re-evaluation of 2026 investment strategies.

This content is intended for informational purposes only and is not financial advice.