Artificial intelligence (AI) bubble fears are back in the headlines. After a massive run in AI stocks, investors are wondering whether valuations are too stretched or whether earnings growth is strong enough to justify the hype. The market is no longer blindly chasing every AI name and is becoming more selective.

Instead of betting only on the flashy AI model builders, money is quietly rotating toward the companies that make the entire ecosystem work. One of them is Vertiv (VRT). It powers the physical backbone of AI data centers, providing uninterrupted power systems, advanced cooling, thermal management, and integrated infrastructure that keep servers running nonstop without a hiccup.

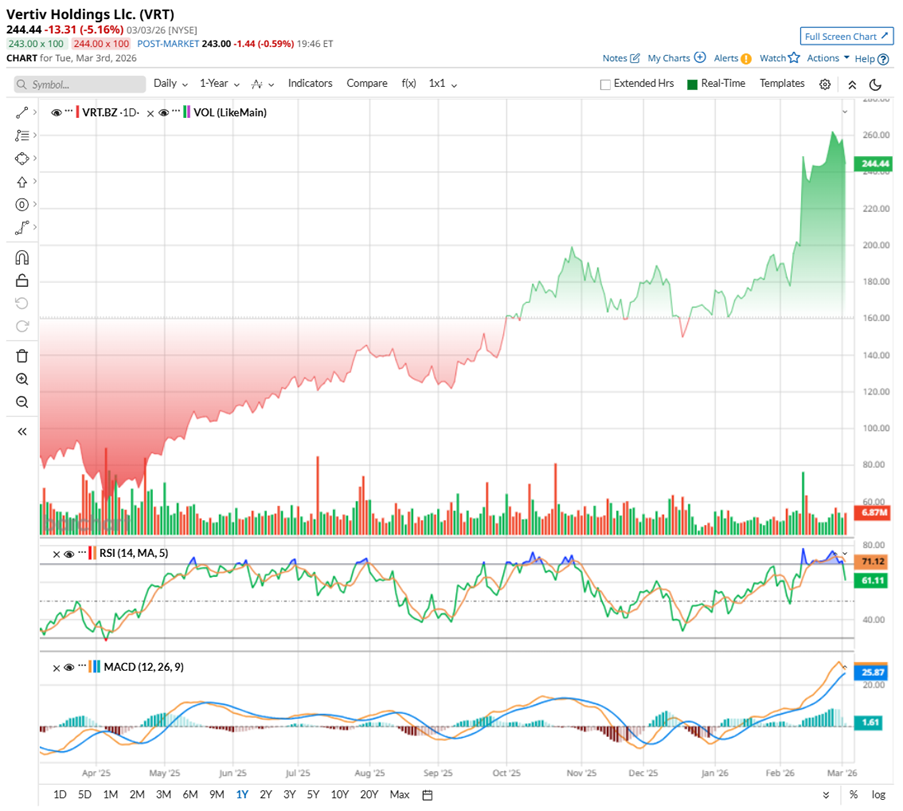

As AI demand surges, data centers need more capacity, more efficiency, and faster buildouts. Vertiv is benefiting directly, with strong order growth to prove it. Investors have responded enthusiastically, sending the stock up 50% already in 2026 — and we are only just into March.

After such a sharp rally, should investors still buy VRT stock now?

About Vertiv Stock

Headquartered in Westerville, Ohio, Vertiv provides the essential infrastructure that keeps today’s digital economy running smoothly. The company combines hardware, software, analytics, and ongoing services to ensure critical applications operate continuously and efficiently.

Its portfolio includes power systems, thermal management solutions, and IT infrastructure designed to support data centers, communication networks, and commercial and industrial facilities. From large cloud environments to the edge of the network, Vertiv helps customers scale operations with reliability and performance. The company serves clients in more than 130 countries worldwide.

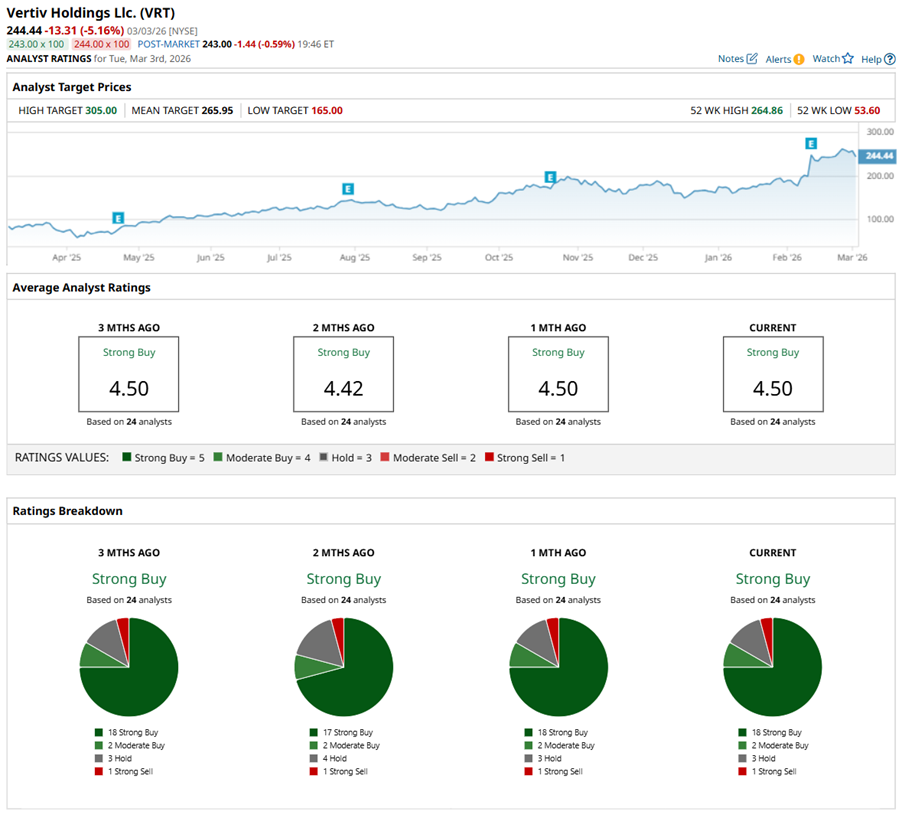

Shares of Vertiv have been on a remarkable run. Over the past 52 weeks, the data center infrastructure specialist has soared 184%, turning heads across Wall Street. The momentum only picked up in recent months, with the stock climbing 100% in the last six months and rising 54% on a year-to-date (YTD) basis. VRT stock touched a peak of $264.86 on Feb. 25, capping off an explosive stretch.

A big catalyst came on Feb. 11, when shares jumped 24% in a single session after a stronger-than-expected fourth-quarter report. That surge briefly pushed the stock into overbought territory. Since then, the heat has cooled, with the 14-day RSI easing back to around 61 — a healthier level that suggests momentum without extreme excess.

The MACD oscillator continues to signal bullishness. The MACD line is trending upward and has crossed above the signal line, indicating strengthening upside momentum. Meanwhile, the histogram remains in positive territory, suggesting that buying pressure still outweighs selling pressure for now.

Valuation-wise, VRT stock carries a premium price tag. The stock trades at about 39.7 times forward adjusted earnings and 9.1 times sales — both above sector averages and its own historical medians. The market is already pricing in strong growth. For long-term investors who believe AI infrastructure spending has years of runway ahead, that premium may feel justified. But more cautious buyers might prefer to wait for dips for a better entry point.

There is also a modest income angle. Vertiv has paid dividends for five years and raised them for three consecutive years. Its latest quarterly payout of $0.0625 per share translates to an annualized dividend of $0.25 per share. With a forward payout ratio near 4%, there is room for future increases.

Vertiv Rises After Its Q4 Report

Vertiv reported Q4 results on Feb. 11, signaling that the AI-driven demand for cooling and power infrastructure is accelerating. At first glance, the numbers looked mixed. Revenue came in at $2.88 billion, just shy of Wall Street’s projections. But step back and the bigger picture tells a stronger story. The top line climbed 23% year-over-year (YOY). Non-GAAP EPS landed at $1.36, comfortably ahead of estimates and up 37% annually.

Digging deeper, product revenue — which makes up 82% of total sales — rose 23% to $2.36 billion. Service revenue, the remaining 18%, grew 20% annually to $519.5 million. Plus, profitability impressed even more. Adjusted operating profit jumped 33% to $668.1 million, with operating margin expanding 170 basis points to 23.2%.

Meanwhile, orders in Q4 surged 252% YOY and 117% sequentially, with backlog swelling to $15 billion, up 109% from last year and 57% from the prior quarter.

The balance sheet was also resilient. Cash and cash equivalents rose to $1.72 billion, operating cash flow rose to $1 billion, and adjusted free cash flow (FCF) reached $909.9 million. Long-term debt edged slightly lower.

Investors loved the report, and shares jumped.

Looking ahead, management struck a confident tone. For fiscal 2026, revenue is projected between $13.25 billion and $13.75 billion, with organic growth of 27% to 29%. Adjusted operating profit is expected between $2.98 billion and $3.1 billion, with margins in the 22% to 23% range. Non-GAAP EPS is guided to be $5.97 to $6.07, and FCF could be somewhere between $2.1 billion and $2.3 billion.

For Q1 fiscal 2026, management expects revenue between $2.5 billion and $2.7 billion, with organic sales growth in the 18% to 26% range. Adjusted operating profit is projected between $475 million and $515 million, translating to operating margins between 18.5% and 19.5%. Non-GAAP EPS is guided between $0.95 and $1.01, signaling that strong AI-driven momentum is set to continue into the new year.

Meanwhile, analysts predict that Vertiv’s Q1 EPS will jump 56% YOY to $1.00, while revenue is expected to be around $2.64 billion. Looking ahead, EPS is projected to rise 46% YOY to $6.15 in fiscal 2026, then rise by 32% annually to $8.10 in fiscal 2027.

What Do Analysts Expect for VRT Stock?

After Vertiv’s stellar report for fiscal 2025 and Q4, multiple brokerages rushed in to adjust their price targets on VRT stock. For instance, JPMorgan analyst Stephen Tusa raised the price target to $305 from $225 and kept an “Overweight” rating.

Meanwhile, Bank of America analyst Andrew Obin reiterated his “Buy” rating and lifted VRT stock’s price target to $277 from $250. Backed by strong order growth and insights from the company’s 10-K filing, Obin believes momentum will carry into 2026. He projects orders to rise 5% to $18.6 billion — enough to meaningfully expand backlog. The analyst also pointed to CEO Giordano Albertazzi’s confidence in a deep pipeline, plus strategic deals with Nvidia (NVDA) and Caterpillar (CAT) as additional growth drivers.

Overall, Wall Street gives VRT stock a “Strong Buy” consensus rating. Out of the 24 analysts covering the stock, 18 suggest a “Strong Buy,” two recommend a “Moderate Buy,” three analysts have a “Hold” rating, and one rates it a “Strong Sell.”

Based on the mean target price of $265.95, VRT stock has potential upside of 6% from current levels. The Street-high target price of $305 implies that the stock could rally as much as 22% in the next 12 months.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Trade the Deep Value and Dubious Option Pricing in Microsoft Stock with This 1 Great Options Strategy

- Why the Charts Say It Might Be Time for a Big Short on Google Stock

- The Smart Money Is Flocking to This Cybersecurity Stock Amid Iran Conflict. 1 Aggressive Way to Trade It Now.

- The VIX Spikes as Investors Panic: 3 ETFs to Trade Market Fear Now