Allentown, Pennsylvania-based Air Products and Chemicals, Inc. (APD) provides atmospheric gases, process and specialty gases, equipment, and related services. Valued at $61.4 billion by market cap, the company develops, engineers, builds, owns, and operates some of the world's largest industrial gas projects, including gasification projects for producing high-value power, fuels, and chemicals.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and APD perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the specialty chemicals industry. APD operates in over 50 countries, allowing it to tap into diverse markets and offer a wide range of products. The company's strong focus on research and development has led to technological advancements in areas like cryogenics and hydrogen fuel cells, giving it a competitive edge in the market.

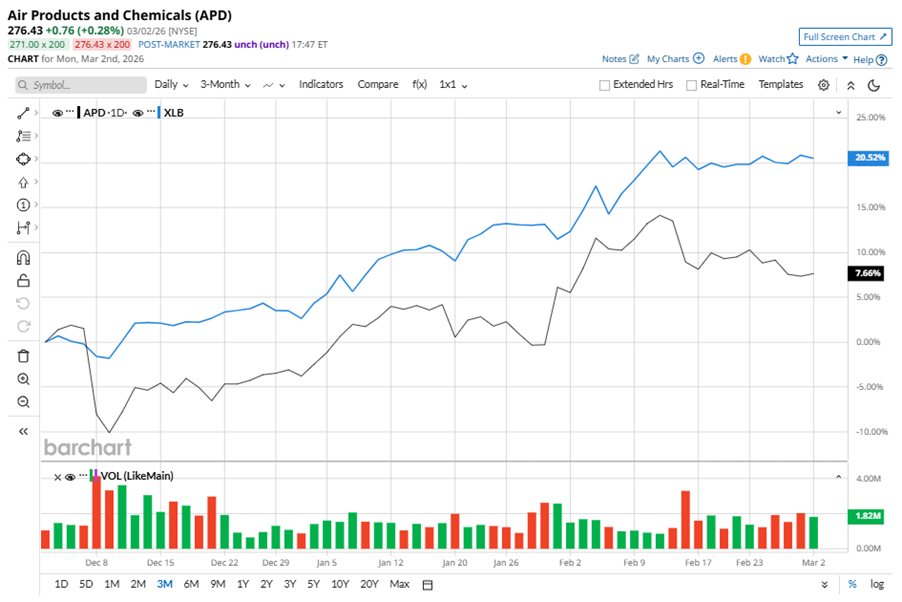

Despite its notable strength, APD slipped 14% from its 52-week high of $321.47, achieved on Mar. 3, 2025. Over the past three months, APD stock gained 7.7%, underperforming the Materials Select Sector SPDR Fund’s (XLB) 20.5% rise during the same time frame.

Shares of APD climbed 11.9% on a YTD basis but fell 12.6% over the past 52 weeks, underperforming XLB’s YTD 17.4% gains and 20% returns over the last year.

To confirm the bullish trend, APD has been trading above its 200-day moving average since early February, with minor fluctuations. The stock is trading above its 50-day moving average since early January.

On Jan. 30, APD shares closed up more than 6% after reporting its Q1 results. Its adjusted EPS came in at $3.16, up 10.5% from the year-ago quarter. The company’s sales increased 5.8% year over year to $3.1 billion.

In the competitive arena of specialty chemicals, Linde plc (LIN) has taken the lead over APD, showing resilience with a 19.5% uptick on a YTD basis and 9.1% gains over the past 52 weeks.

Wall Street analysts are reasonably bullish on APD’s prospects. The stock has a consensus “Moderate Buy” rating from the 23 analysts covering it, and the mean price target of $301.52 suggests a potential upside of 9.1% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart