DaVita Inc. (DVA) is a leading healthcare provider specializing in kidney care services, including dialysis treatments for patients with chronic kidney failure. Headquartered in Denver, Colorado, it operates outpatient centers worldwide. The company has a market capitalization of $9.94 billion.

DaVita’s stock has been under pressure over the past year due to rising costs, exacerbated by a ransomware attack that resulted in a data breach affecting 2.7 million individuals. Over the past 52 weeks, the stock has declined 18.2%. However, after reporting strong quarterly results, it is up 24% year-to-date (YTD). DaVita’s shares had reached a 52-week low of $101 on Jan. 14, but are up 39.4% from that level.

On the other hand, the broader S&P 500 Index ($SPX) has gained 14% and 1.3% over the same periods, respectively, indicating that while the stock has underperformed the broader market over the past year, it has outperformed YTD. Next, we compare the stock with its own sector. The State Street Health Care Select Sector SPDR ETF (XLV) has increased 7.2% over the past 52 weeks and 1.9% YTD, exhibiting the same trend.

On Feb. 2, DaVita reported its fourth-quarter and fiscal 2025 results. As the results were better than expected, the company’s stock rose 21.2% intraday on Feb. 3. Its Q4 revenue increased 9.9% year-over-year (YOY) to $3.62 billion, which is based on a 9% growth in dialysis patient service revenues to $3.40 billion. With the expiration of the Affordable Care Act, DaVita expects some headwinds this year and the next. However, this is expected to be offset by the elimination of the cyber-incident impact observed in 2025.

For the current quarter, Wall Street analysts expect DaVita’s EPS to increase 20.5% YOY to $2.41 on a diluted basis. EPS is expected to increase 31.4% annually to $14.16 for fiscal 2026, followed by a 19.4% improvement to $16.90 in fiscal 2027. The company has a solid record of topping consensus estimates in three of the four trailing quarters.

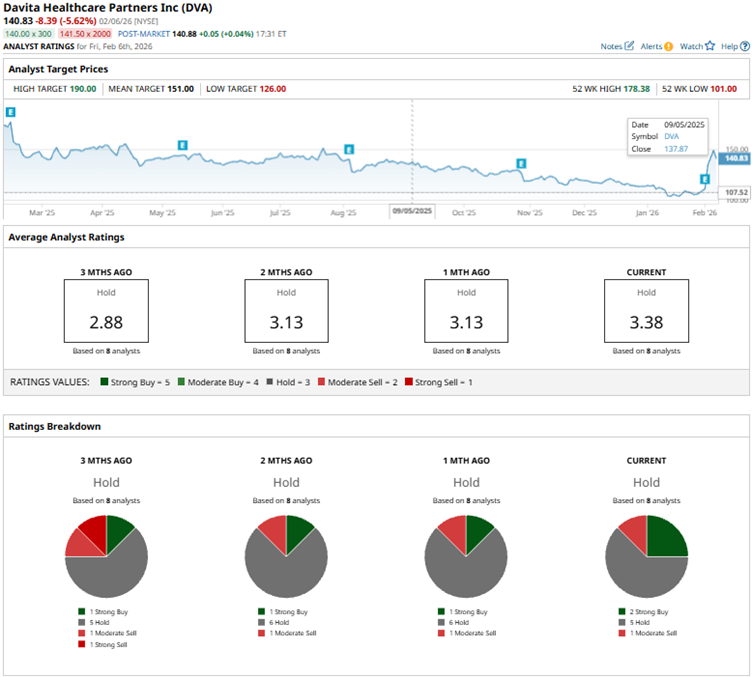

Among the eight Wall Street analysts covering DaVita’s stock, the consensus is a “Hold.” That’s based on two “Strong Buy” ratings, five “Holds,” and one “Moderate Sell.” The ratings configuration has become slightly more bullish than a month ago, with the number of “Strong Buy” ratings increasing from one to two.

Post DaVita’s Q4 earnings results, analysts at UBS maintained a “Buy” rating and a $190 price target on the stock. The company is optimistic about achieving 2% long-term growth in dialysis volume by improving patient outcomes and reducing mortality. Key strategies include boosting GLP-1 medication use, cutting missed treatments, and deploying proven new technologies.

DaVita’s mean price target of $151 indicates an 7.2% upside over current market prices. Moreover, the Street-high UBS-given price target of $190 implies a potential upside of 34.9%.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Down 31% in a Month, Is SHOP Stock a Buy Before Q4 Earnings?

- MicroStrategy Stock Is Outperforming the S&P 500 by the Largest Margin in 2 Years. Should You Buy the Dip or Run Away?

- Stop Worrying About the Software Armageddon and Buy These 5 Stocks Now

- Option Volatility And Earnings Report For February 9 - 13