Artificial intelligence (AI) is no longer just powering chatbots and cloud software. It’s beginning to drive cars, too. Autonomous vehicles (AVs), which once seemed like a futuristic fantasy, are now steadily becoming part of everyday transportation. Among companies leaning hard into this shift is Uber Technologies (UBER), which is rapidly expanding its robotaxi ambitions. Although Uber’s latest quarterly results disappointed some investors due to an earnings miss, management’s growing focus on autonomy may be the more important story shaping its long-term outlook.

On its earnings call, management revealed plans to have robotaxis operating in 15 cities by year-end, underscoring the company's determination to lead in autonomy. CEO Dara Khosrowshahi expressed strong confidence that autonomous vehicles would ultimately benefit the entire mobility sector. He also described robotaxis as a meaningful growth driver in markets where they’re already active, specifically highlighting San Francisco, Atlanta, and Austin, Texas, as early examples of traction.

For now, autonomous vehicles represent just 0.1% of global rideshare trips, whether on Uber’s platform or elsewhere, a tiny slice of today’s market. But the CEO made it clear he sees something much bigger ahead, emphasizing that AV technology could unlock a “multitrillion-dollar opportunity” for Uber over time. So, with management making such bold long-term bets despite near-term earnings pressure, should investors scoop up Uber shares now?

About Uber Stock

Since launching in 2010, Uber has become a familiar name in ride-hailing, making it possible to book a trip with just a few taps on a phone. What began in San Francisco has expanded into a global platform, with more than 72 billion trips completed and counting. Over time, the company has broadened its focus beyond rides to include food delivery and freight services.

By expanding into multiple areas of transportation and logistics, Uber has become a regular part of how many people move around cities and receive goods. Its platform connects riders, drivers, couriers, and businesses, reflecting how digital services are increasingly shaping everyday urban transportation and delivery networks. And now, Uber is sharpening its focus on getting autonomous vehicles all the way to customers’ doorsteps.

To make that happen, Uber is leaning into a partnership-driven strategy to expand its robotaxi footprint. Most recently, the company teamed up with EV manufacturer Lucid Group (LCID) and self-driving technology firm Nuro, Inc., with plans to help deploy at least 20,000 robotaxis across global markets, a clear step beyond small-scale trials.

Also, the company works with Alphabet's (GOOG) (GOOGL) Waymo and May Mobility, both active players in autonomous driving. In addition, chip giant Nvidia (NVDA) provides the high-performance computing technology that helps power advanced self-driving systems. Together, these alliances underline Uber's efforts to build a broad network of partners to support its long-term robotaxi expansion.

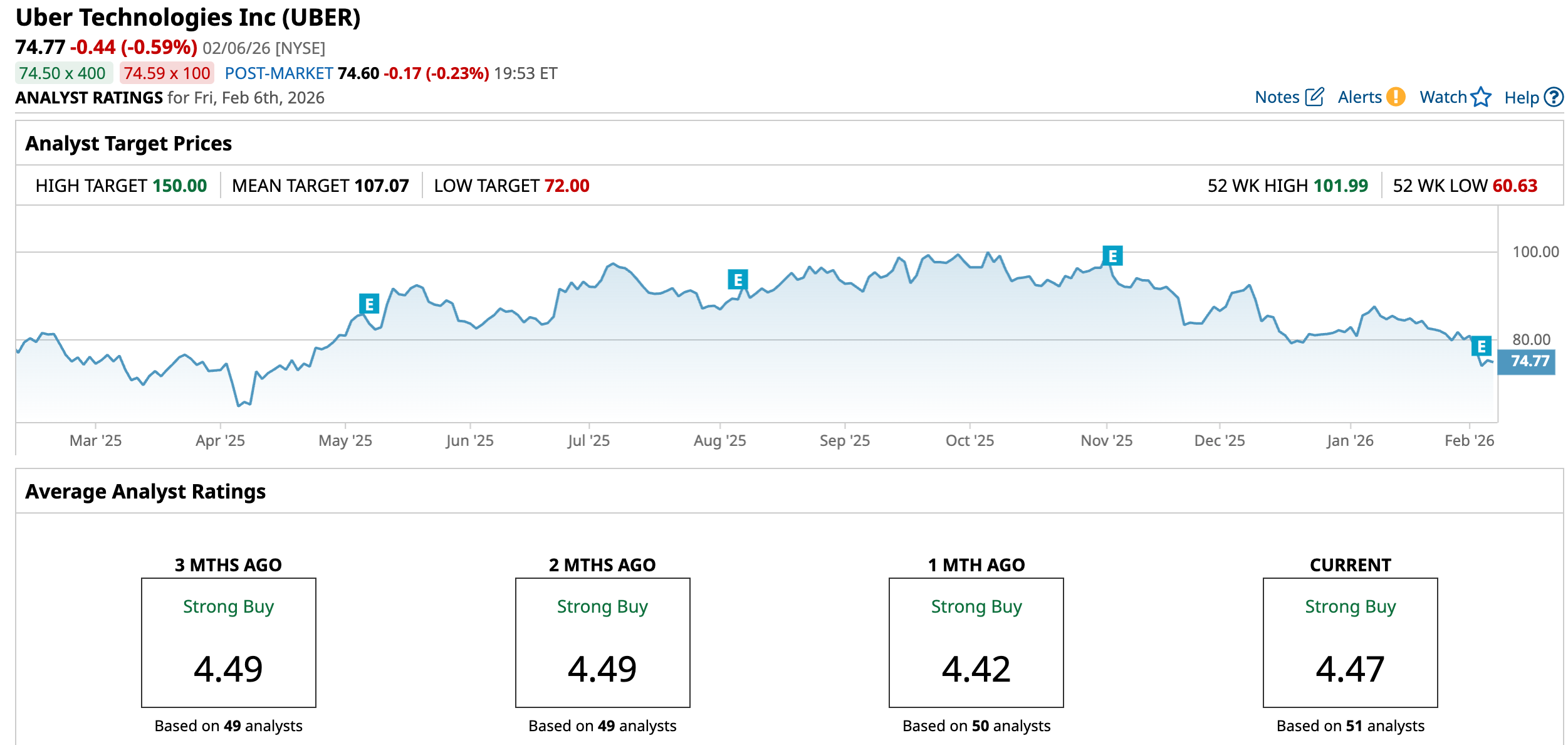

Currently commanding a market capitalization of roughly $155.3 billion, shares of this ride-hailing giant have posted a respectable return of 6.83% over the past year, edging past the broader S&P 500 Index ($SPX), which has climbed almost 14% over the same period. So far in 2026, however, the ride-hailing stock has hit a bump, slipping nearly 8.5%.

Much of the recent volatility followed its latest quarterly results, which failed to impress Wall Street. At the same time, investors are also keeping a close eye on rising costs tied to Uber’s long-term push into autonomous vehicle technology, spending that could weigh on near-term profitability even as it aims to power future growth.

A Look Inside Uber’s Q4 Financial Performance

When Uber released its fiscal 2025 fourth-quarter results on Feb. 4, investors got a report that showed strong demand but softer profitability, and the market responded with caution, sending the stock down 5.2% that day. Revenue for the final quarter of 2025 rose a healthy 20% year-over-year (YOY) to $14.37 billion, narrowly topping Wall Street’s $14.34 billion estimate and signaling that activity across Uber’s platform remains robust.

Much of that growth was driven by its core segments. The mobility business, which includes ride-hailing, brought in $8.2 billion, up 19% from a year ago, while delivery revenue took an even greater leap of 30% YOY to $4.9 billion. Still, earnings didn’t quite meet expectations. Adjusted EPS for the quarter came in at $0.71, a 27% increase YOY but below the Street’s $0.79 forecast.

On a GAAP basis, net income totaled $296 million, a sharp drop from $6.88 billion a year earlier. Results were affected by a $1.6 billion net pre-tax headwind tied to revaluations of equity investments, along with higher taxes and the company’s efforts to offer more affordable rides to grow bookings and attract new users.

Operationally, however, momentum remained strong. Total trips surged 22% YOY to 3.8 billion during the quarter, fueled by 18% growth in Monthly Active Platform Consumers. Gross bookings also rose an impressive 22% to $54.1 billion, highlighting continued engagement across the platform.

Looking ahead to the first quarter of fiscal 2026, Uber expects growth to remain solid, forecasting gross bookings of $52 billion to $53.5 billion, which would represent 17% to 21% YOY growth on a constant-currency basis. Furthermore, the company guided for non-GAAP EPS of $0.65 to $0.72, implying 37% YOY growth at the midpoint, along with adjusted EBITDA of $2.37 billion to $2.47 billion.

How Are Analysts Viewing Uber Stock?

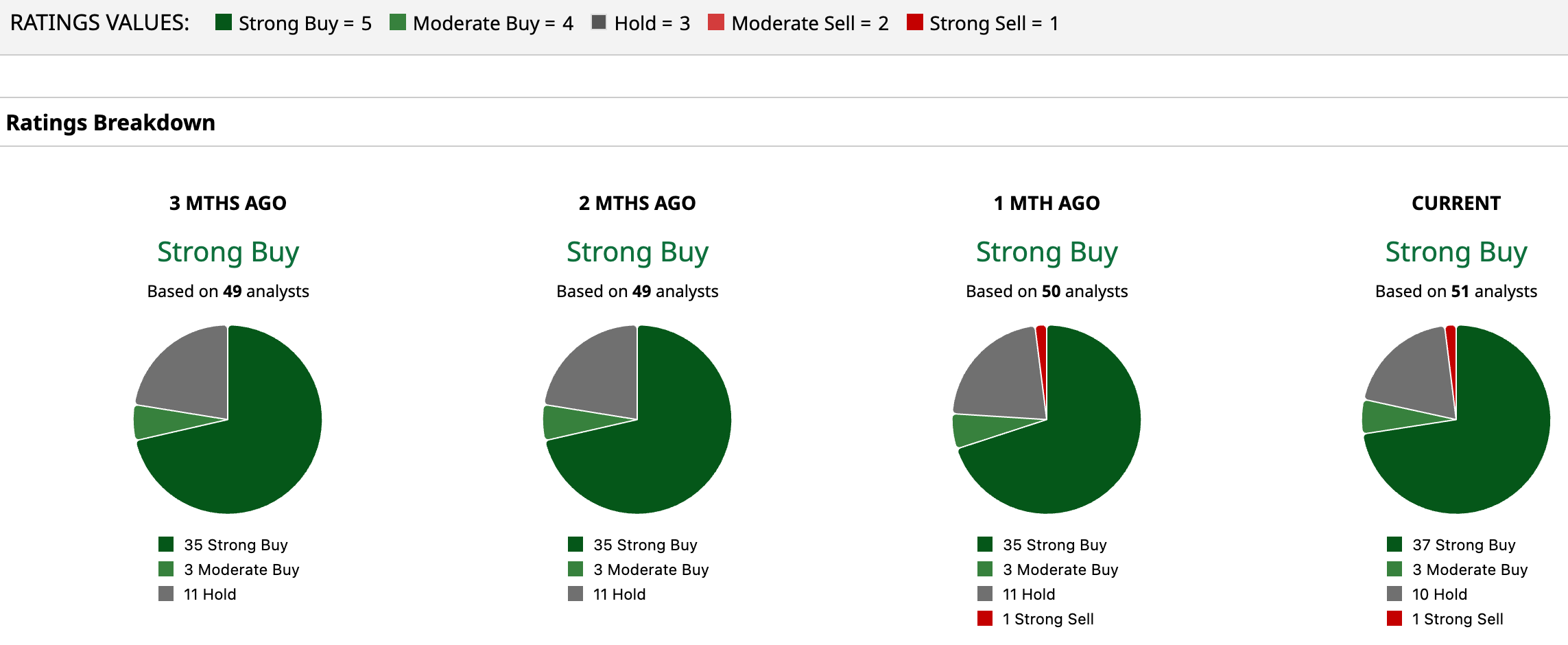

Although investors were less than thrilled with the company’s latest quarterly results, Wall Street’s overall stance on Uber remains firmly optimistic. The stock currently holds a consensus “Strong Buy” rating, suggesting analysts largely see recent weakness as short-term noise rather than a break in the company’s long-term growth trajectory.

Out of 51 analysts covering the name, 37 rate it a “Strong Buy,” three recommend a “Moderate Buy,” 10 suggest “Hold,” and just one analyst has a “Strong Sell” rating. The average price target of $107.07 points to roughly 43% upside from current levels, while bullish Street target of $150 implies the shares could surge 100% if Uber’s growth strategy plays out as expected.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Should You Buy Uber Stock Now for a ‘Multitrillion-Dollar’ Opportunity in Robotaxis?

- 3 Oversold Software Stocks You Should Buy on the Dip Now

- Tower Semiconductor Just Struck a New AI Deal with Nvidia. Should You Buy TSEM Stock Here?

- The Saturday Spread: Reducing Uncertainty in an Uncertain World (AMZN, CHWY, EXPE)