The Walt Disney Company (DIS) has just turned a new page in its 103-year history, naming Josh D’Amaro as its next Chief Executive Officer effective Mar. 18, succeeding long-time leader Robert A. Iger in a unanimous board decision. D’Amaro, a 28-year Disney veteran and the architect of the company’s expansive theme parks and experiences division, takes the helm at a pivotal moment for the entertainment giant, one shaped by slowing box office growth, the ongoing shift to streaming profitability, and strategic bets on parks, AI, and global content.

D’Amaro lately served as chairman of Disney Experiences division, which generates about $36 billion in annual revenue and roughly 60% of Disney’s profits, even as the company’s film, TV, and sports businesses have struggled. The leadership transition also includes the promotion of Dana Walden to Disney’s first-ever companywide Chief Creative Officer, underscoring a dual focus on operational strength in experiences and renewed creative discipline across Disney’s media portfolio.

With investor sentiment mixed following the leadership change, is now the time for a strategic buy, a cautious hold, or a sell signal for DIS shares?

About The Walt Disney Company Stock

The Walt Disney Company is an iconic entertainment and media conglomerate that operates across film and television production, streaming services, theme parks and resorts, sports networks, and consumer products. Headquartered in Burbank, California, Disney’s portfolio includes globally recognized brands such as ABC, ESPN, Marvel, Pixar, and Lucasfilm, and it distributes content through its flagship platforms like Disney+, Hulu, and ESPN+.

Leveraging nearly a century of creative storytelling and diversified experiences, Disney has grown into one of the world’s leading entertainment companies with a market cap of $189.6 billion.

Over the past year, DIS has struggled to deliver positive returns for shareholders as its share price has trended downward amid mixed operational results and strategic uncertainty. Disney’s stock has underperformed broader markets and many sector peers, closing the last session at $105.35, around 18.36% below its 52-week high of $124.69, reached in June 2025.

Disney’s total return over the past 12 months has been negative, with a 4.79% decline, while the year-to-date (YTD) slump is 7.5%.

While segments like streaming and parks have shown improvement, with streaming and theme parks generating strong revenue, these gains have often been overshadowed by weaknesses in Disney’s traditional media businesses. The entertainment division, including TV and movies, has faced declining operating income and softer revenue, which has dampened investor enthusiasm and pressured the share price. Notably, the stock slumped as much as 7.4% on Feb. 2, following the latest earnings release.

Compounding this performance backdrop is the ongoing leadership transition at the top of the company. Uncertainty around CEO succession and strategic direction amid Bob Iger’s planned exit and the appointment of Josh D’Amaro continues to weigh on sentiment.

The stock is trading at a modest premium compared to industry peers at 15.84 times forward earnings.

Mixed Financial Performance

Disney reported its fiscal first-quarter (ended Dec. 27, 2025) earnings on Feb. 2. For the quarter, total revenues were $26 billion, up about 5% year-over-year (YOY). However, total segment operating income declined 9% to $4.6 billion from $5.1 billion a year earlier, reflecting margin pressure across segments. Its adjusted EPS was $1.63, down from $1.76 in the year-ago quarter, but topped estimates.

Across Disney’s major business segments, performance was varied. In Entertainment, which includes film, television, and related media, revenue increased about 7% YOY, but operating income fell sharply by 35% as higher programming, production, and marketing expenses more than offset revenue gains.

Disney’s streaming business (Disney+, Hulu and related services) delivered solid growth with revenues up around 11% to approximately $5.3 billion. Operating income in this unit rose significantly by 72% YOY to roughly $450 million as price increases and bundling strategies improved margins.

The Parks and Experiences (Experiences) division was a standout, posting record quarterly revenue of about $10 billion, driven by increases in attendance and guest spending. Experiences also contributed the bulk of the company’s operating profit, with segment operating income up about 6% YOY.

The Sports segment posted slight revenue growth (around 1% YOY) but operating income declined sharply (about 23%), partly due to the impact of a temporary carriage dispute with YouTube TV and other cost pressures.

For guidance, Disney reaffirmed expectations for double-digit adjusted earnings per share growth for full-year fiscal 2026 and improved operating margins in streaming.

Analysts remain optimistic as they predict EPS to be around $6.57 for fiscal 2026, up 11% YOY, before surging by another 10.5% annually to $7.26 in fiscal 2027.

What Do Analysts Expect for Disney Stock?

Recently, UBS reiterated its “Buy” rating on Walt Disney with a $138 price target. The firm remains confident in Disney’s outlook, citing improving direct-to-consumer profitability and continued momentum in the Experiences segment from new cruise capacity and attractions.

Plus, Bernstein SocGen reiterated an “Outperform” rating on Walt Disney with a $129 price target.

On the other hand, BofA Securities lowered its price target on Walt Disney to $125 from $140 but maintained a “Buy” rating, citing near-term segment pressures despite confidence in the company’s long-term outlook.

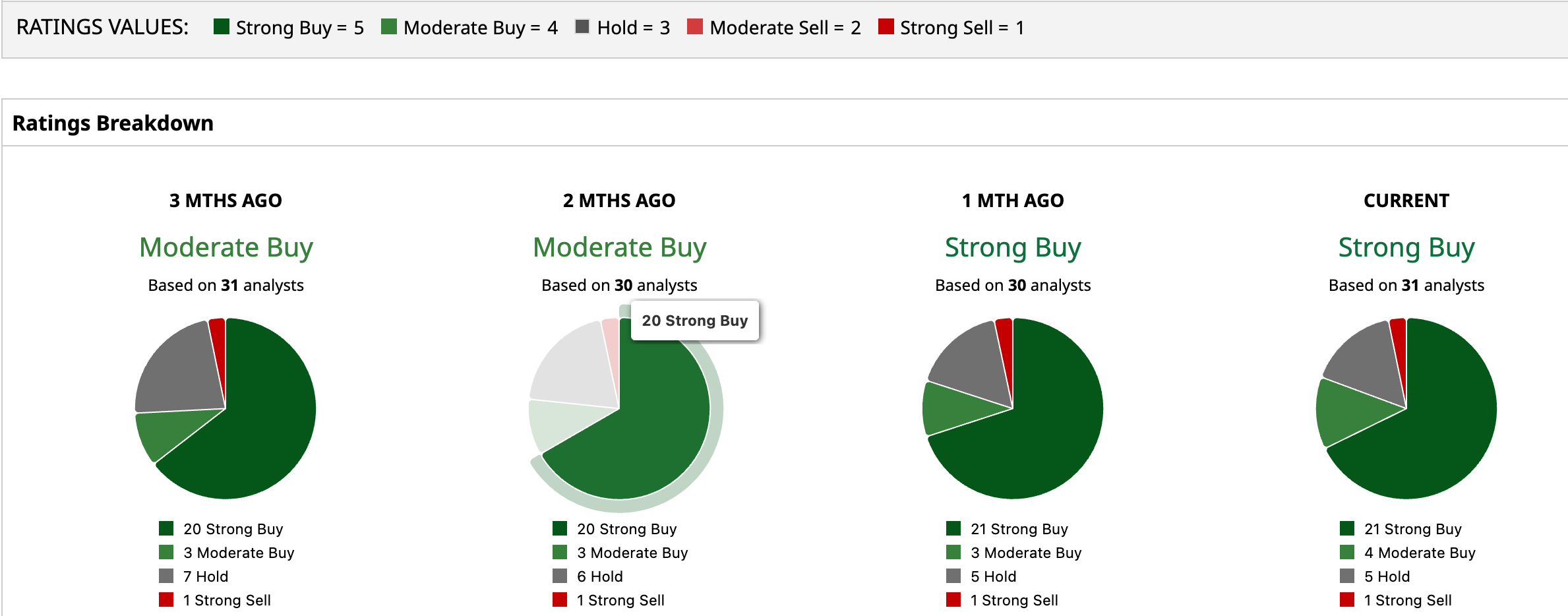

Wall Street is majorly bullish on DIS. Overall, DIS has a consensus “Strong Buy” rating. Of the 31 analysts covering the stock, 21 advise a “Strong Buy,” four suggest a “Moderate Buy,” five analysts are on the sidelines, giving it a “Hold” rating, and one recommends a “Strong Sell.”

DIS’ average analyst price target of $133.70 signals an upside potential of 26.8%. The Street-high target price of $160 suggests that the stock could rally as much as 51.75%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Nio Says Profitability Is Just Around the Corner. Should You Buy NIO Stock Here?

- As Analysts Forecast 50% Upside, Is Now the Time to Buy the Dip in AMD?

- Is There a Light at the End of the Tunnel for Qualcomm Stock? What Options Data, Technicals Tell Us.

- This Overlooked Biotech Giant Could Surprise Investors This Quarter