Microsoft (MSFT) is entering a new chapter in its artificial intelligence (AI) strategy—one defined less by partnership and more by independence. After investing nearly $14 billion in OpenAI and tightly integrating its models into Azure, Microsoft 365 Copilot, GitHub, and other flagship products, the company is now openly pursuing what it calls “true self-sufficiency” in AI. That ambition goes beyond incremental diversification. It signals a structural shift toward developing in-house frontier models, expanding proprietary AI chips like the Maia accelerator, and reducing reliance on a single external supplier for its most critical technology layer.

So as Microsoft doubles down on “true self-sufficiency,” the core question for investors becomes clear: Is this strategic shift a calculated step toward deeper competitive advantage and long-term value creation, or does it add another layer of risk to its growth story? And more importantly, should you be adding to your MSFT position now—or waiting for clearer evidence that the strategy will pay off? Let’s take a closer look!

About Microsoft Stock

Microsoft is a dominant force in the technology sector, boasting a diverse portfolio spanning software, cloud computing, AI, gaming, and hardware. Notably, the company is among the pioneers targeting the AI market through its partnership and substantial investments in OpenAI. MSFT has a market cap of $2.98 trillion, making it the fourth most valuable public company in the world.

Shares of the tech giant have slumped 18% on a year-to-date (YTD) basis. There are two main drivers behind those losses: the company’s FQ2 earnings report and souring sentiment toward the software sector. MSFT stock took a hit in late January after the tech giant reported higher-than-expected spending and slower cloud sales growth, stoking investor fears that its AI investments may take longer than anticipated to pay off. The stock was also caught in a software sector sell-off amid concerns that AI could disrupt the industry.

Microsoft Moves Toward “True Self-Sufficiency” in AI

Microsoft’s AI chief, Mustafa Suleyman, told the Financial Times last week that the tech giant is striving for “true self-sufficiency” in AI. That means developing its own powerful models and steadily reducing its dependence on OpenAI, even as the two companies maintain their partnership. Essentially, the company aims to move beyond the “powered by someone else” model.

Suleyman told the outlet that the strategic shift followed the restructuring of its partnership with OpenAI in October 2025. The deal converted Microsoft’s $13.75 billion investment into a 27% stake in OpenAI Group PBC, valued at roughly $135 billion. Under the pact, Microsoft’s intellectual property rights for both models and products were extended through 2032, including post-Artificial General Intelligence (AGI) models. In addition, Bloomberg reported that Microsoft will remain entitled to receive 20% of OpenAI’s revenue. Meanwhile, OpenAI gained the flexibility to source computing power beyond Azure and seek new investors, while Microsoft secured the right to independently pursue AGI, either on its own or with third-party partners.

Microsoft’s flagship AI product is Microsoft 365 Copilot, serving as an “AI-first” productivity assistant integrated across the Microsoft 365 ecosystem. It combines large language models (LLMs) with organizational data from Microsoft Graph, including emails, chats, and documents, to provide context-aware assistance. Microsoft 365 Copilot is actively boosting the company’s top and bottom lines. In the most recent quarter, revenue in the Productivity and Business Processes segment rose 16% year-over-year (YoY) to $34.1 billion, fueled by growth in Microsoft 365 Commercial Cloud, which was driven in turn by Microsoft 365 E5 and Microsoft 365 Copilot. During the FQ2 earnings call, CEO Satya Nadella said that companies are now paying for 15 million Microsoft 365 Copilot subscriptions. The key point is that Microsoft 365 Copilot primarily relies on OpenAI’s advanced LLMs, hosted on Microsoft’s Azure OpenAI Service. And that dependence on a “single supplier” began to look like a vulnerability, potentially prompting the company to develop its most advanced technology in-house.

Suleyman said, “We have to develop our own foundation models, which are at the absolute frontier, with gigawatt-scale compute and some of the very best AI training teams in the world.” The company is investing heavily in collecting and organizing the vast datasets needed to train advanced systems. “That’s our true self-sufficiency mission,” Suleyman added. He also said the company’s in-house models are expected to launch “sometime this year.” Microsoft’s AI chief noted that the company aims to capture a larger share of the enterprise market by developing “professional-grade AGI”—advanced AI tools capable of handling everyday tasks for knowledge workers.

Meanwhile, the company seems to have begun its AI “self-sufficiency” push even before the restructuring of its partnership with OpenAI was announced. In August 2025, Microsoft AI unveiled MAI-1-preview, describing it as “an in-house mixture-of-experts model” that was “pre-trained and post-trained on ~15,000 NVIDIA H100 GPUs,” with plans to integrate it into select Copilot text applications. The company is also pushing for AI hardware “self-sufficiency,” having recently introduced its Maia 200 accelerator, the second generation of its in-house processors. Some of the first units were slated for Microsoft’s superintelligence team, where they would generate data to help improve the next generation of AI models. The chips will also power the Copilot assistant for businesses and AI models, including OpenAI’s latest, which the company rents to cloud customers.

Beyond its core AI “self-sufficiency” push, Microsoft is also cutting back on its dependence on OpenAI in other ways. The company has expanded its AI supplier base, hosting models from xAI, Meta, Mistral, and Black Forest Labs in its data centers. It has also recently started using models from the startup Anthropic for coding and within its Microsoft 365 productivity suite.

Should You Bet on MSFT Stock?

Microsoft’s pursuit of “true self-sufficiency” marks a major shift from being OpenAI’s primary distributor to becoming its direct competitor in the development of “frontier” AI models. This strategy aims to give Microsoft full-stack control over its AI ecosystem, from the chips and data centers to the underlying intelligence, eliminating the risk of being “powered by someone else.” The move is generally viewed as a strategic, long-term positive for MSFT stock.

First, it allows Microsoft to control its own “AI destiny” while reducing reliance on a single external partner. Second, Microsoft can reduce the licensing fees it pays to OpenAI by deploying its own models, thereby improving its profit margins. Finally, in-house models can allow Microsoft to tailor AI solutions specifically for corporate clients, potentially increasing its market share in the enterprise AI market.

However, there are also risks, as developing proprietary “frontier” models requires massive investment in infrastructure, meaning elevated capex—something that recently weighed on MSFT stock. Moreover, Microsoft has said it remains constrained by limited AI computing capacity, meaning it must allocate resources between its internal AI development initiatives and the numerous external customers relying on its cloud services for AI workloads. Microsoft CFO Amy Hood said that had the company allocated all of its newest GPU chips to Azure, the growth rate would have exceeded 40% in FQ2.

Putting it all together, I believe the potential long-term benefits of Microsoft’s push for “true self-sufficiency” in AI outweigh the associated risks. And considering where MSFT stock is trading after the post-earnings selloff, it is a real gift for long-term investors.

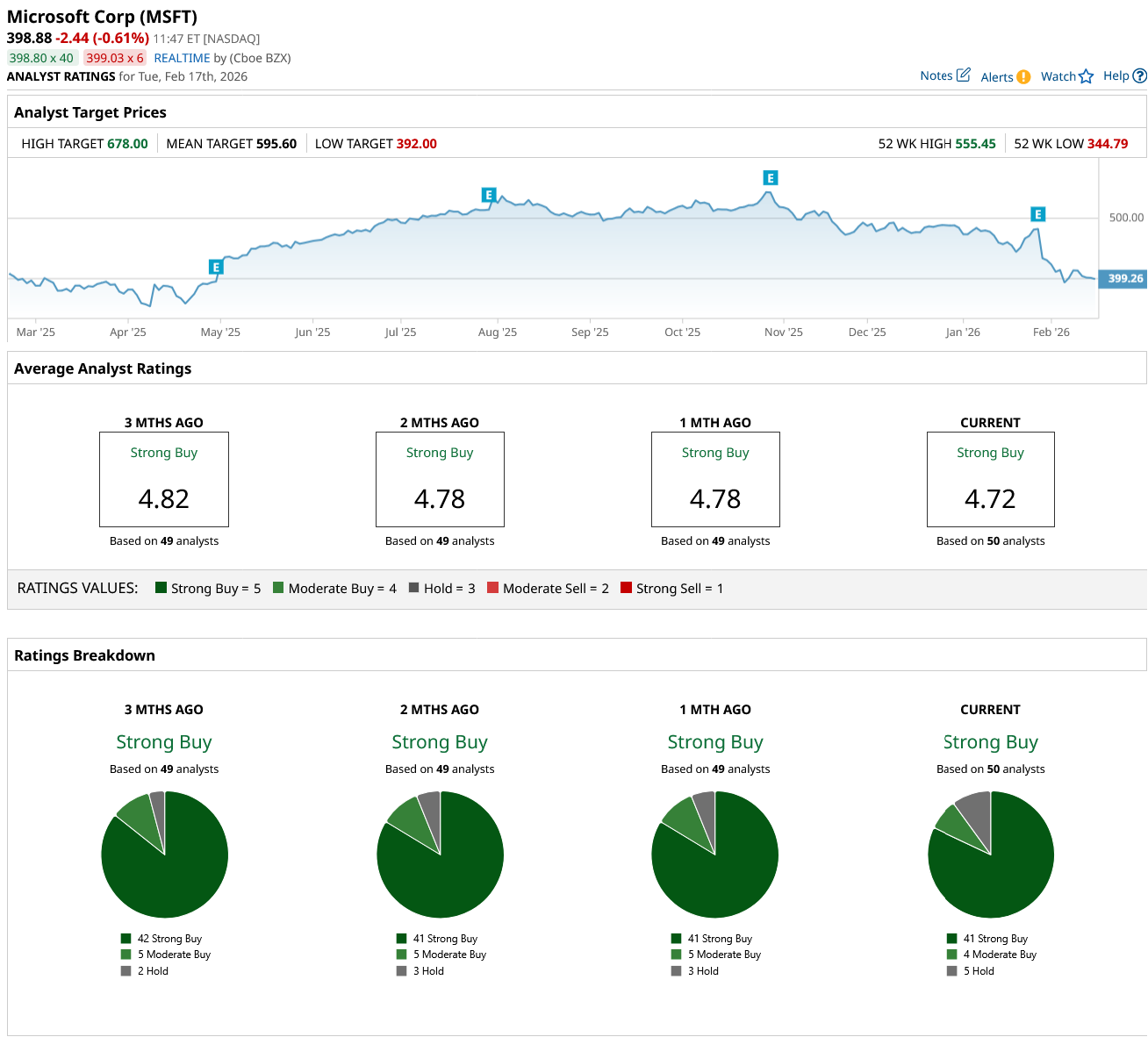

Wall Street analysts remain highly bullish on MSFT stock, as reflected in its consensus “Strong Buy” rating. Among the 50 analysts covering the stock, 41 rate it a “Strong Buy,” four assign a “Moderate Buy” rating, and the remaining five recommend holding. The average price target for MSFT stock is $595.60, representing 48.4% upside potential from Friday’s closing price.

On the date of publication, Oleksandr Pylypenko had a position in: MSFT . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart