The so-called software Armageddon has arrived, and it has not tiptoed in. Fears that advanced artificial intelligence (AI) models from OpenAI and Anthropic could automate vast swaths of enterprise applications have triggered an aggressive sector-wide selloff. Jefferies Financial Group (JEF) captured the mood bluntly, dubbing the moment a “SaaSapocalypse.”

The carnage shows up clearly on the scoreboard. The iShares Expanded Tech-Software Sector ETF (IGV) has fallen 21.69% year-to-date (YTD). Within that turbulence, Salesforce (CRM), the world’s #1 AI CRM, has watched its stock sink 28.38% in 2026.

However, seasoned voices have challenged the prevailing narrative. Wedbush Securities analyst Dan Ives has argued that investors have overstated the immediacy of the threat and underestimated the adaptability of established platforms. And in this backdrop, Salesforce has continued to execute with discipline.

Recently, the company secured a landmark $5.6 billion contract with the U.S. Army, reinforcing its enterprise credibility. In addition, it delivered a quarterly report that surpassed earnings expectations, demonstrating that operational momentum has persisted despite macro and sector headwinds.

Now, Salesforce is scheduled to release its fourth-quarter and full-year fiscal 2026 results on Wednesday, Feb. 25, after the market closes. All eyes are going to turn to the earnings results to assess whether Salesforce can transform Q3 momentum into tangible gains and navigate sector challenges.

About Salesforce Stock

The San Francisco, California-based Salesforce delivers cloud-based customer relationship management (CRM) powered by AI. With a market cap of roughly $173.7 billion, the company unifies data through its platform, including Agentforce, enabling AI agents, workflow automation, actionable insights, and seamless management of sales, service, marketing, and commerce operations.

Over the past 52 weeks, CRM stock has plunged 42.48%, and in the past three months, it has dropped 21.09%. Yet Salesforce is not alone in the slump. The entire software sector is in a rut, with the IGV ETF down 22.41% over 52 weeks and 22.53% in the past three months.

From a valuation standpoint, CRM stock is trading at 18.97 times forward adjusted earnings, sitting below both the industry average and its own five-year historical multiple. The compression signals a potentially attractive entry point for investors who see value in the company’s growth trajectory.

Salesforce also pays an annual dividend of $1.66 per share, which equates to a 0.90% yield. It paid its most recent quarterly dividend of $0.42 per share on Jan. 8 to shareholders of record as of Dec. 18, 2025.

Salesforce Surpasses Q3 Earnings

On Dec. 3, 2025, Salesforce unveiled its Q3 2026 earnings, wherein revenue climbed 8.6% YOY to $10.3 billion, topping analyst projections of $10.28 billion. Adjusted EPS surged 34.9% to $3.25, beating Street estimates of $2.86. Investors responded positively, lifting the stock 1.7% on announcement day and an additional 3.7% the following session.

Beyond the top and bottom lines, Salesforce demonstrated exceptional strength across its forward-looking metrics. Its Q3 current remaining performance obligations (cRPO) increased 11% year-over-year (YOY) to $29.4 billion, signaling a healthy pipeline and durable revenue visibility.

Momentum stemmed largely from Agentforce and Data 360, which together generated nearly $1.4 billion in annual recurring revenue (ARR), a 114% YOY gain. With over 9,500 paid Agentforce agreements and 3.2 trillion tokens processed, Salesforce continues to solidify its position as a leader in building the Agentic Enterprise.

Encouraged by these results, Salesforce’s management has raised fiscal year 2026 revenue guidance to a range of $41.45 billion to $41.55 billion, representing 9% to 10% YOY growth. They also project adjusted EPS for fiscal 2026 in the range of $11.75 to $11.77.

Meanwhile, analysts currently expect Q4 2026 EPS to decline 3.6% YOY to $2.14, while for the full fiscal year 2026, the bottom line is projected to grow 13.1% to $8.92. Looking ahead to fiscal year 2027, analysts anticipate EPS to rise 9.3% to $9.75.

What Do Analysts Expect for Salesforce Stock?

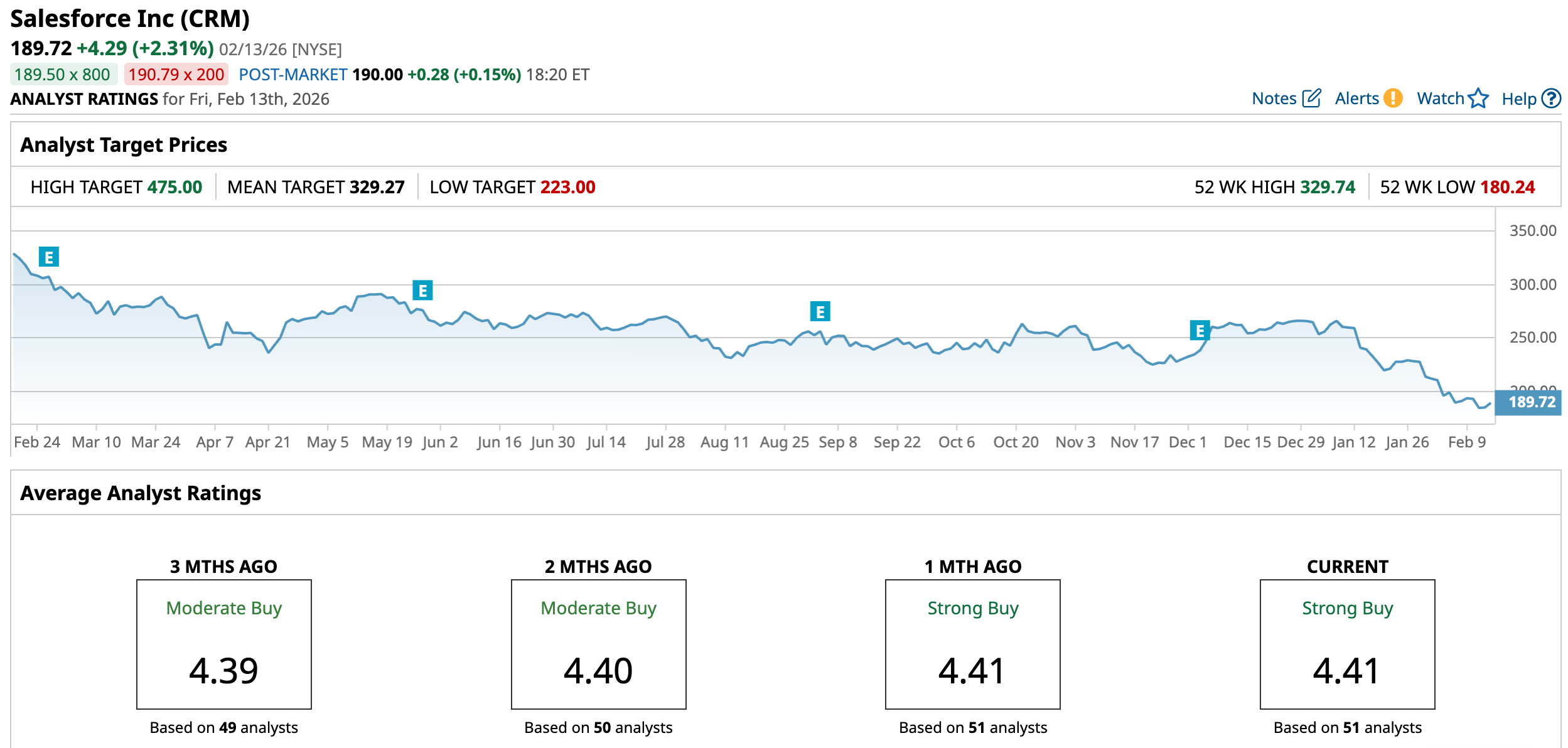

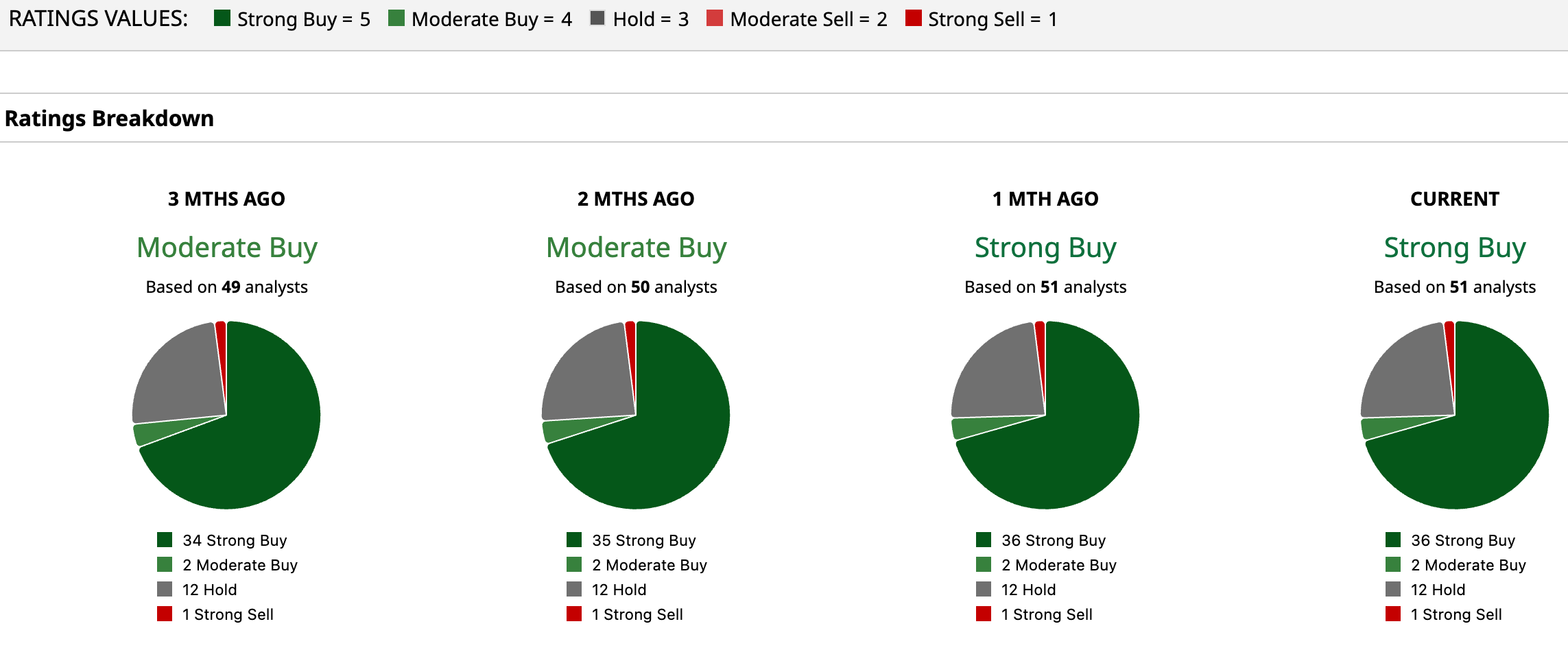

Wall Street has currently assigned CRM stock a “Strong Buy” overall rating, reflecting widespread optimism among analysts about Salesforce’s growth prospects and market positioning. Among 51 analysts covering the stock, 36 recommend “Strong Buy,” two suggest “Moderate Buy,” 12 advise “Hold,” and one issues a “Strong Sell.”

Nevertheless, the average price target of $329.27 represents potential upside of 73.6%. Meanwhile, the Street-high target at $475 indicates a gain of 150.4% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart