Networking and communications technology solutions provider Cisco (CSCO) will report its second-quarter earnings for fiscal 2026 today, after the market closes. Shares of the company have been a beneficiary of the AI trade, rising 38% over the past year. However, investors should curb their enthusiasm about the fact that this uptick can sustain, as Cisco was once touted to be the biggest gainer from the dot-com boom era, as the thesis was that its networking equipment would be at the core of the internet infrastructure buildout.

Well, that didn't play out, as the company currently trades at a market cap of $342.9 billion, lower than the market cap figure at its peak of $536.4 billion 26 years ago.

Cisco's Q2 Expectations

Coming back to the present times, what are investors expecting from the company's Q2 2026 earnings then?

Notably, the Street expects Cisco's earnings and revenue to be $1.02 per share and $15.11 billion for the quarter. While the earnings would represent an annual growth rate of 8.5%, the revenue figure, if hit, will mark a year-over-year (YoY) growth of 7.9%. This may seem modest, yet the anticipated growth rates are much ahead of Cisco's performance over the last 10 years. The period saw the company growing its revenue and earnings at CAGRs of just 1.52% and 0.75%, respectively.

Meanwhile, the company expects revenue and EPS to be in the range of $15 billion to $15.2 billion and $1.01 to $1.03, respectively.

Q1 Recap

Exciting growth may have eluded Cisco, but it always boasts of a robust set of financials. That was reinforced by its showing in Q1 when it reported a beat on both the revenue and earnings front. While revenues for the quarter ended Oct. 25 came in at $14.9 billion (+7.5% YoY), earnings were up by 10% in the same period to $1 per share, exceeding the Street estimate of $0.98 by a whisker.

Remaining performance obligations, or RPO, a key metric used to track demand for a company's products and services, were at $42.9 billion. This was up 7% from the prior year, with product RPO up 10% and service RPO up 4%.

However, net cash flow from operating activities declined by 12.3% on an annual basis to $3.2 billion, as Cisco closed the October 2025 quarter with a cash balance of $8.4 billion. Although this was above its short-term debt levels of $6.7 billion, the figure was almost 80% of its cash balance.

The company also declared a dividend of $0.41 per share, which was paid on Jan. 21, 2026. Moreover, the stock offers a dividend yield of 1.93%, higher than the sector median of 1.07%, with the company raising dividends consecutively over the past 14 years.

Finally, for the guidance for fiscal 2026, Cisco is forecasting revenues to be between $60.2 billion and $61 billion, while earnings are expected to be between $4.08 and $4.14.

Can Cisco Seize the AI Day?

Cisco had it all going for it at the turn of the century with the Internet boom. However, it was unable to capitalize on the same. So, what is it doing so that it does not miss the AI train as well? Let's see.

For starters, the $28 billion acquisition of data intelligence platform Splunk has been a pivotal move. As the largest transaction in Cisco's 40-year history, it forms the foundation of the company's shift from a primarily hardware-focused networking provider to a leader in AI-driven software and security solutions. Splunk specializes in analyzing “machine data,” which is the vast, unstructured streams generated by servers, routers, applications, and sensors across an enterprise's digital environment.

AI workloads are notoriously intensive and intricate. Splunk's AI-Ready PODs integration enables organizations to monitor critical metrics such as GPU temperature, utilization rates, and latency in large language model (LLM) responses. While Cisco owns the networking layer, Splunk provides the deep analytics layer, creating a powerful combination.

Beyond Splunk, Cisco is undertaking a broader strategic realignment, moving from simply supplying network infrastructure to delivering solutions specifically to what customers actually require. A central piece of this evolution is Silicon One, the company's programmable ASIC architecture designed specifically for networking applications.

Silicon One offers a unified, software-programmable platform that spans the full network stack, from front-end internet traffic to the high-speed back-end fabrics that interconnect AI GPUs. Unlike legacy fixed-function chips, Silicon One can often be updated through software to adapt to new standards or requirements, avoiding costly hardware replacements. In fact, Cisco states that its latest G300 series can reduce job completion time by as much as 28%.

Demand for Silicon One remains robust, with the company guiding for $3 billion in AI infrastructure revenue for fiscal 2026—roughly 50% year-over-year growth in that segment. In addition, Cisco is expected to confirm during the upcoming earnings call that it has shipped its one-millionth Silicon One chip in the second quarter.

Thus, with an existing legacy in network equipment, Cisco is being innovative while also being aware of its weaknesses and looking to alleviate them with strategic acquisitions, consequently brightening its prospects of being a genuine winner in the massive AI infrastructure buildout.

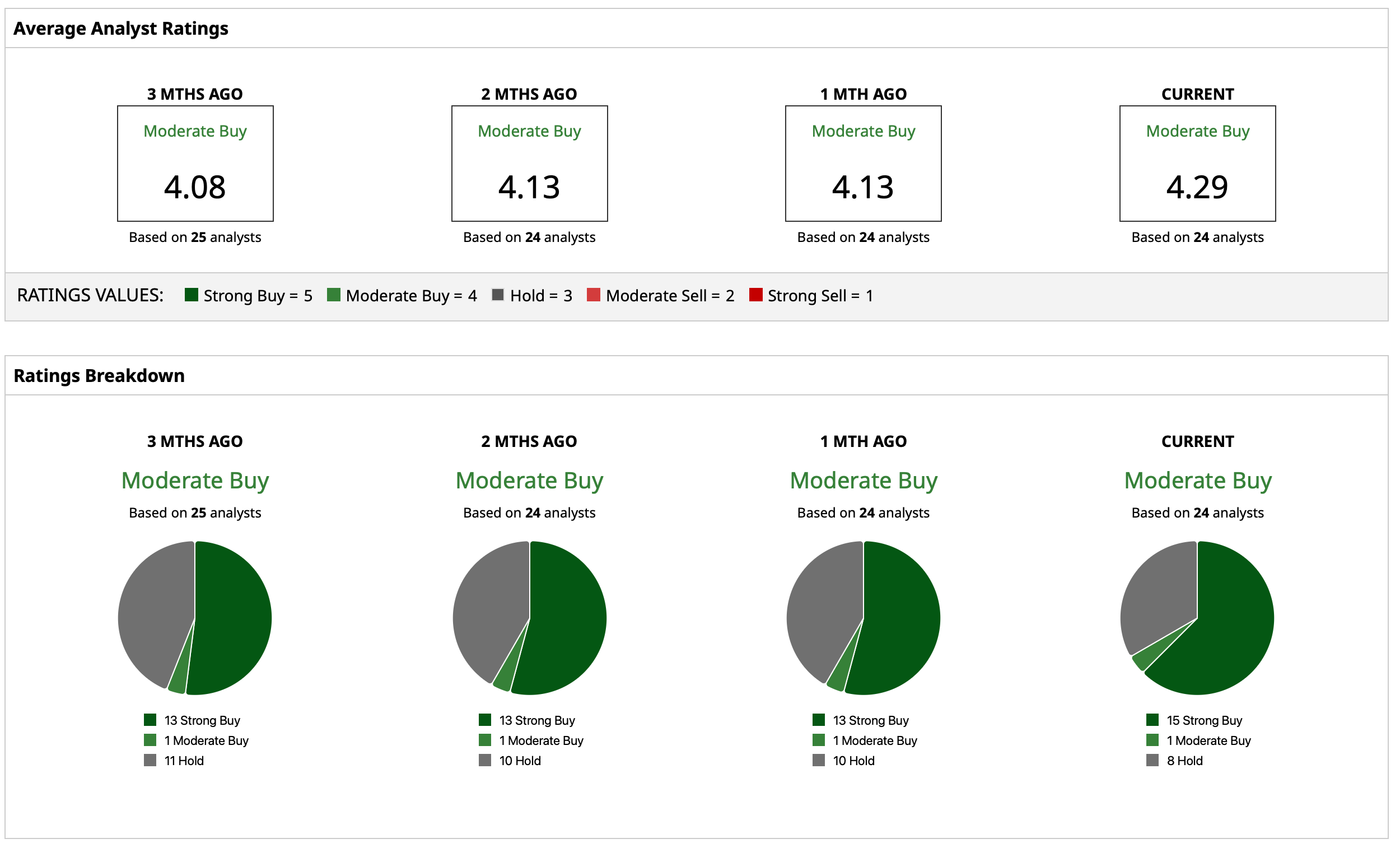

Analyst Opinion on CSCO Stock

Overall, analysts have deemed the CSCO stock to be a “Moderate Buy,” with a mean target price that reflects limited upside potential from current levels. The high target price of $100 indicates an upside potential of about 16% from current levels. Out of 24 analysts covering the stock, 15 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and six have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart