Qualcomm’s (QCOM) post-earnings slump has revived a harsh thesis that QCOM has no bottom in sight for 2026, and the market is trading it that way. After its Feb. 4 report, the stock gave up roughly two years of gains and slipped back toward 2020 levels, even though it delivered about $12.25 billion in quarterly revenue. That headline number could not overcome the cautious outlook, and HSBC has warned that calling a clear bottom in 2026 may simply not be realistic yet.

This tension becomes even clearer when set against what is happening across chips more broadly. Omdia expects global semiconductor revenue to surpass $1 trillion in 2026, with about 30.7% year-over-year (YoY) growth driven by AI-hungry memory and logic demand. Within that surge, computing and data storage are projected to climb roughly 41.4% year over year to more than $500 billion.

Qualcomm sits right in the uncomfortable middle of these two stories. If semiconductors are really marching toward the $1 trillion mark in 2026, the key question is whether QCOM ultimately rides that surge or keeps lagging while Wall Street keeps searching for a bottom. Let’s dive in.

QCOM’s Compressed Yet Costly Profile

Qualcomm is a semiconductor company based in San Diego, California, that designs wireless chips, connectivity solutions, and licensing technology for smartphones, cars, and AI devices. QCOM offers an annual forward dividend of $3.56 per share, which translates to a 2.61% yield that may look comforting as the share price slides.

At this morning's price of about $140, the stock is down 18% year-to-date (YTD) and lower by 19% over the past 52 weeks.

Their equity of $147B now trades at a 14.01x forward P/E versus a 23.95x sector median and a 3.05x PEG versus 1.54x, signaling discounted pricing and doubts about near-term earnings momentum.

QCOM reported its latest fiscal first-quarter numbers on Feb. 4, delivering a profit of $3 billion for shareholders. Per-share profit came in at $2.78 on a GAAP basis, reflecting the earnings attributable to common equity after standard expenses. This result was supplemented by adjusted earnings of $3.50 per share once stock-based compensation and other one-off items were stripped out to give a cleaner view of ongoing profitability.

The chipmaker posted revenue of $12.25 billion in that period. This narrowly missed the $12.28 billion that eight analysts surveyed by Zacks had penciled in. Qualcomm also previously reported earnings per share of $2.80 for the quarter ending Dec. 25, reinforcing that the current trend line is not deteriorating from a low base but from a healthier one.

QCOM’s Quiet Data Center Bet

Qualcomm is pushing a series of targeted moves in AI infrastructure and data center connectivity. The company has launched an AI solution center in Riyadh through a partnership with Saudi firm Humain. This project will deploy up to 200 megawatts of AI data center racks powered by Qualcomm hardware starting in 2026.

This initiative is built around the Qualcomm AI200 and AI250 platforms. These are designed to deliver strong computing output for every dollar spent and for every unit of power consumed, which suits large-scale AI inference.

Qualcomm is also expanding its intellectual property and data center capabilities through acquisition. It initially set out a roughly $2.5 billion deal to buy UK-based Alphawave Semi, a high-speed connectivity chip specialist, with closing targets for the first quarter of 2026.

That transaction has now been completed around one quarter earlier than planned. It shows execution speed around what management views as strategic technology.

Following the deal, Alphawave Semi’s chief executive and co-founder, Tony Pialis, has been put in charge of Qualcomm’s data center business. This move brings dedicated high-speed connectivity expertise directly into Qualcomm’s leadership structure.

Analyst Expectations Versus a Falling Tape

Wall Street’s numbers on Qualcomm tell a mixed story that fits the “no bottom in sight” mood. For the March 2026 quarter, analysts see EPS dropping to $1.94 from $2.35 a year earlier, flagging a 17.45% YoY decline that fits the “no bottom in 2026” narrative.

Qualcomm’s own guidance is brighter on the surface, with management projecting EPS between $2.45 and $2.65 and revenue in a $10.2–$11 billion range for the fiscal second quarter.

The full-year picture does not completely ease those worries. For the fiscal year ending September 2026, the average earnings estimate stands at $9.61 per share, below the prior year’s $10.07. That works out to an expected earnings decline of 4.57% for the year.

Even with that cooling earnings profile, one notable voice, Bernstein, argues that the company is positioned to benefit from steady AI-related spending and gradually improving sector conditions, even if 2026 is bumpy.

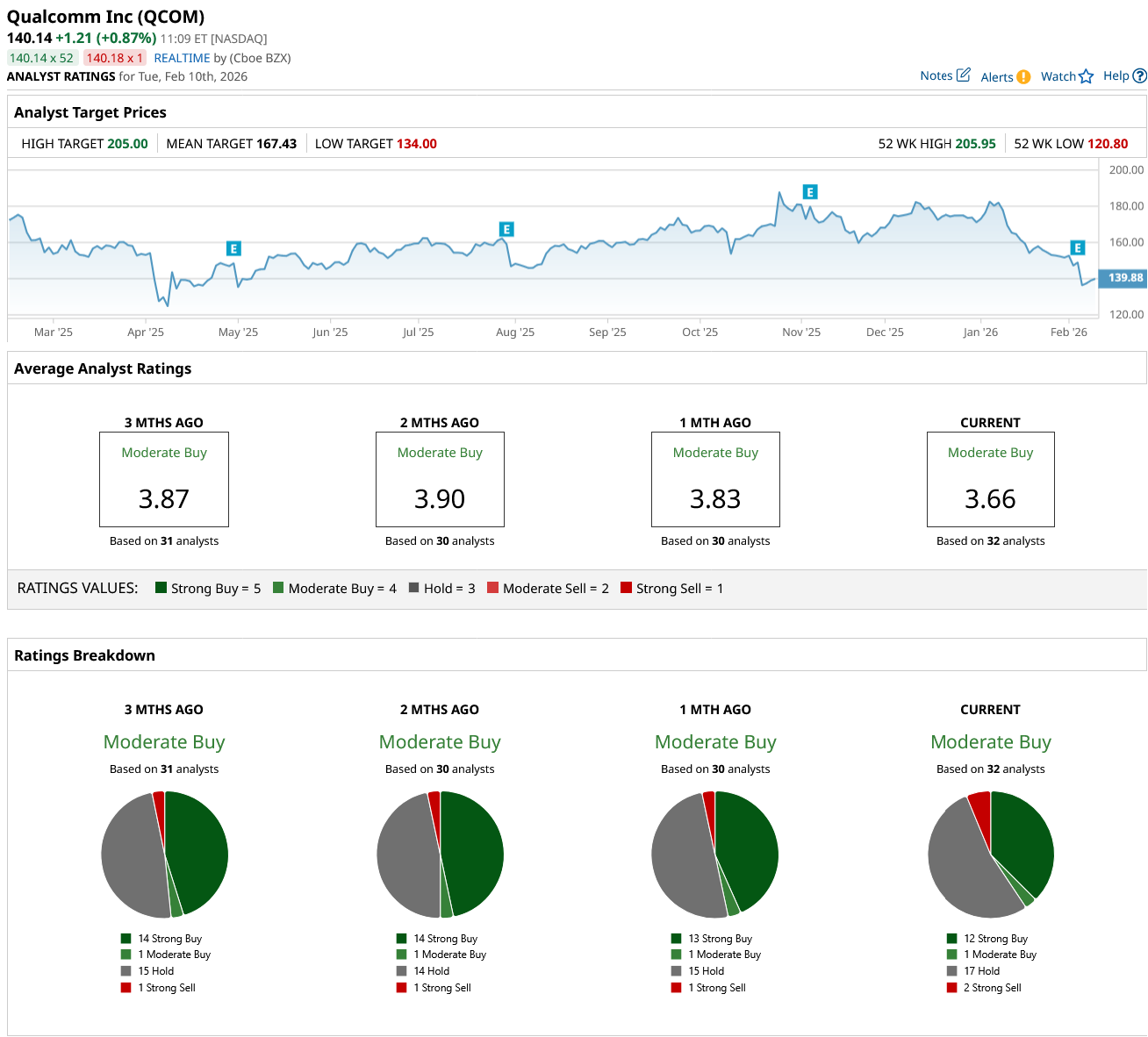

The consensus stance on the stock remains constructive rather than outright bearish. A group of 32 analysts collectively land on a “Moderate Buy” recommendation, reflecting a view that the earnings dip is manageable. The average target of $167.43 suggests roughly 22% upside from the recent price, indicating that analysts still see meaningful recovery potential.

Conclusion

Wall Street’s message on QCOM is clear enough. The near-term earnings path looks shaky, and the market is no longer willing to simply overlook that uncertainty. The stock’s slide, softer 2026 growth profile, and handset-heavy exposure help explain why more “sell” calls are surfacing even as management leans harder into AI and data centers. More downside or sideways action still looks more likely than a clean rebound until memory constraints ease and fundamentals clearly improve. Until that turn shows up in the numbers, caution still looks more realistic than bravado.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart