With a market cap of $94.9 billion, Royal Caribbean Cruises Ltd. (RCL) is a global vacation leader operating 69 ships across more than 1,000 destinations on all seven continents through its brands Royal Caribbean, Celebrity Cruises, Silversea, and a joint venture with TUI Cruises. With expanding private destinations and upcoming entry into river cruising, the company is building a connected vacation ecosystem that turns unforgettable trips into lifelong travel experiences.

Shares of the Miami, Florida-based company have outperformed the broader market over the past 52 weeks. RCL stock has returned 31.6% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 15.6%. Moreover, shares of the company are up 24.8% on a YTD basis, compared to SPX’s 1.7% rise.

Focusing more closely, shares of the cruise operator have outpaced the State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) 4.2% gain over the past 52 weeks.

Despite reporting weaker-than-expected Q4 2025 adjusted EPS of $2.80 and revenue of $4.26 billion, shares of RCL climbed 18.7% on Jan. 29. The company delivered strong full-year 2025 results, with adjusted EPS of $15.64 on $17.9 billion in revenue, both above guidance, driven by record WAVE season demand, nearly two-thirds of 2026 capacity already booked at record rates, and upbeat 2026 adjusted EPS guidance of $17.70 - $18.10, implying a 23% CAGR under the Perfecta program. Additional confidence came from the long-term growth catalysts such as the Discovery Class ships and the expansion of Celebrity River Cruises to 20 vessels by 2031.

For the fiscal year ending in December 2026, analysts expect RCL’s adjusted EPS to grow 15.7% year-over-year to $18.09. The company's earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing on another occasion.

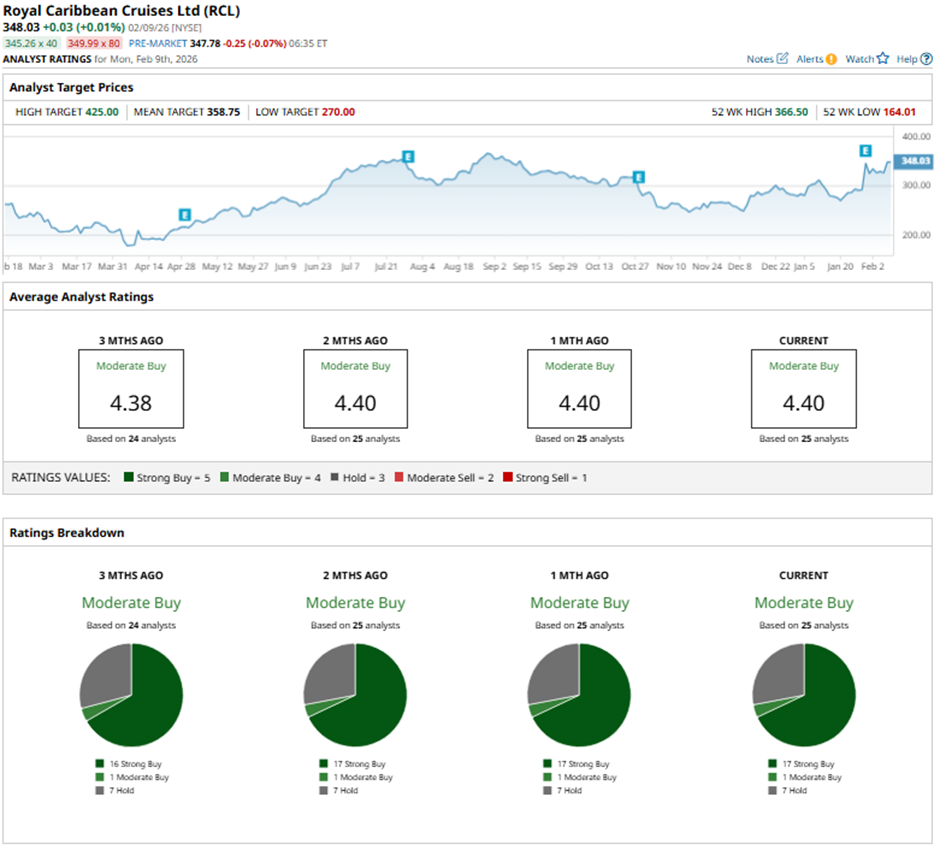

Among the 25 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 17 “Strong Buy” ratings, one “Moderate Buy,” and seven “Holds.”

On Jan. 30, TD Cowen analyst Kevin Kopelman reiterated a “Buy" rating on Royal Caribbean and set a price target of $350.

The mean price target of $358.75 represents a premium of 3.1% to RCL's current levels. The Street-high price target of $425 implies a potential upside of 22.1% from the current price levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.