The main points of discussion on an early morning financial television show had to do with trade, tariffs, and a name that starts with T.

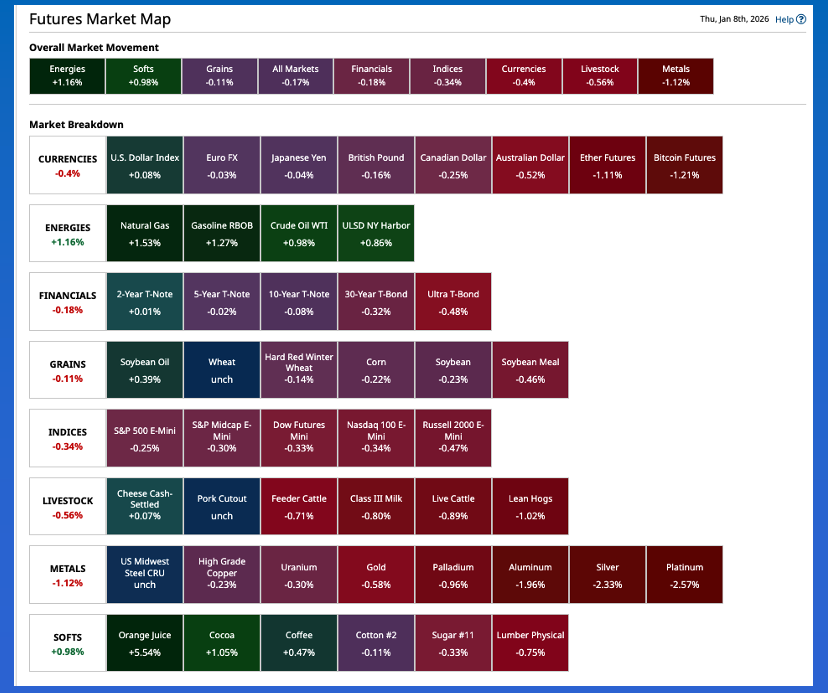

Overnight trade saw the commodity complex in general under pressure, with only Energies and Softs higher.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.The common theme of the Grains sector overnight was “quietly lower” as traders show more interest in other sectors for fundamental reasons.

Morning Summary: If one were to have a drinking game of taking a shot of their favorite beverage every time the name starting with T was mentioned, they would’ve been staggering within the first 15 minutes of this morning’s financial television program. The 3 big issues were the US president calling for a 50% increase in defense spending, pushing it to $1.5 trillion, a move that will likely shut the US government down later this month. But hey, US defense company stocks are rallying, so there’s that. This was followed by a discussion on global trade with the Global Trade Chair for BCG, a global consulting firm, whose latest findings showed international trade not only grew during 2025 but is expected to see more of the same this year. That being said, one highlight (lowlight?) was the “US is becoming a slower-growing trade hub…Impact on GDP yet to be determined”. The third topic was the US Supreme Court possibly ruling the US president’s executive orders creating tariffs on nearly every other country unconstitutional. However, as I said in an interview Wednesday, the US president has shown no interest in acknowledging court rulings or that silly little thing called Congress, so I don’t see a change in trade policy coming any time soon.

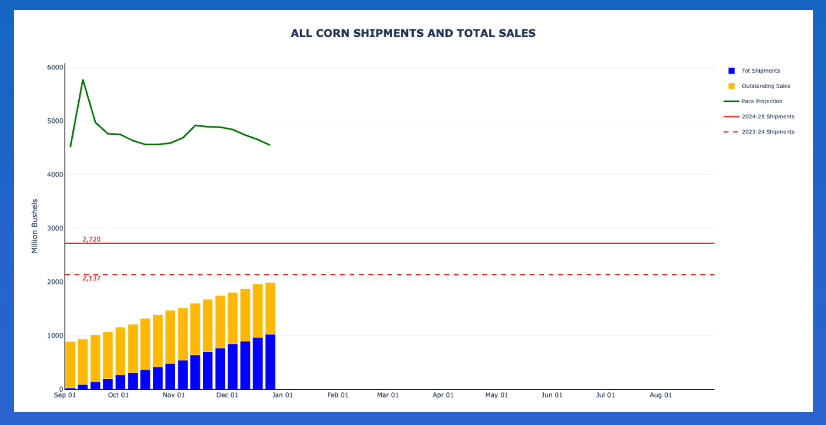

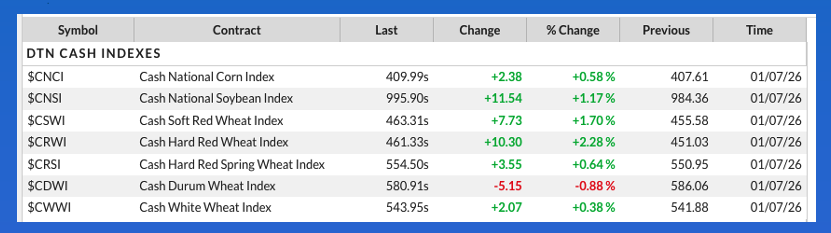

Corn: The corn market was quietly higher early Thursday morning, and when I say “quietly”, the March issue (ZCH26) is showing trade volume of fewer than 10,000 contracts as of this writing. March posted a 1.0 cent trading range overnight and was sitting 1.25 cents lower. Those who tend to lean to the bearish side will point out the contract was on its session low to start the day, while die-hard bulls will counter with, “Yeah, but the contract is only 1.0 cent off its session high!” Fundamentally, there isn’t much change to talk about, though we will get the next round of weekly export sales and shipments numbers later Thursday morning, this one for the week ending Thursday, January 1. This means the reports are finally up to date, again just ahead of the next expected US government shutdown following the January 30 budget deadline. While export demand for US corn was still running strong with the previous update, the trend is for the pace projection based on reported shipments to decrease. The National Corn Index ($CNCI) came in at $4.10 last night putting national average basis at 36.75 cents under March futures as compared to last Friday’s final figure of 37.25 cents under March.

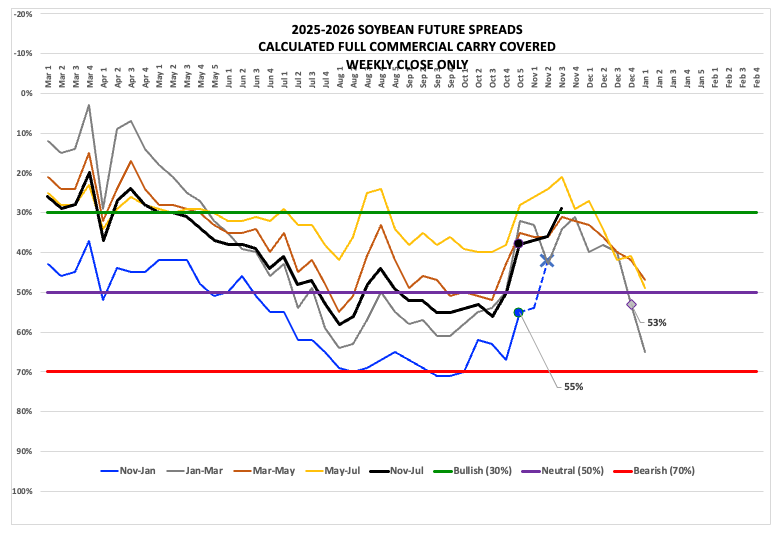

Soybeans: The soybean market was also quietly lower to start the day, breaking the pattern that we’ve seen so far this year of quietly higher overnight trade. The March issue (ZSH26) was sitting 3.5 cents lower at this writing after sliding as much as 5.5 cents while registering 16,000 contracts changing hands. The only thing this indicates is the world’s largest buyer was likely doing something else, including watching long-term weather forecasts for Brazil. Something else I mentioned in one of Wednesday’s interviews was the fact the coffee market’s forward curve was still in backwardation (inverted) indicating a bullish supply and demand situation. And with Brazil the world leader in production and exports of coffee, and the crop being a weather derivative, we could ask the question if there is some general concern over Brazilian weather as the country moves deeper into its summer season[i]. A look at weekly closes for the March-May soybean futures spread and we see it covered 42.5% calculated full commercial carry at Wednesday’s close as compared to last Friday’s settlement covering 47%, the largest percent covered since 52% on Friday, October 17. This tells us the commercial side of the soybean market remains comfortable with Brazil’s 2026 production potential, for now.

Wheat: The wheat sub-sector was quietly mixed pre-dawn Thursday. As of this writing the HRW market was showing a small loss, the HRS market a small gain, and SRW mostly unchanged, all three on light trade volume. Starting with HRW we see the March issue posted a 3.5-cent trading range on trade volume of 1,600 contracts and was sitting 1.0 cent lower, and 0.5 cent off its session low at this writing. There isn’t much we can read into this, so let’s move on to HRS where we see the March issue up 3.75 cents on trade volume of fewer than 100 contracts. Right. All it would take is one sell order to change things, so again, let’s move on. March SRW was near unchanged after posting a 3.0-cent trading range, up 2.0 cents to down 1.0 cent while registering fewer than 4,000 contracts changing hands. What stands out to me with the sub-sector is the two winter National Cash Indexes ($CSWI) ($CRWI) have gained roughly 10.0 cents through early January – a seasonal move – but continue to run well below previous 5-year end of January low prices established last year. Based on the Law of Supply and Demand this tells us market fundamentals remain bearish.

[i] Acknowledging the two crops – coffee and soybeans – are grown in different parts of the country.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart