Meta Platforms (META) and Microsoft (MSFT) are two of the most dominant forces shaping the future of technology, driving innovation across artificial intelligence (AI), cloud computing, virtual reality, and digital advertising. Microsoft, a decades-old powerhouse, has built a legacy through its diversified product portfolio, giving it a stable foundation and recurring revenue strength.

Meta, on the other hand, is a newer disruptor, rapidly evolving from a social media giant into a leader in AI-driven content, digital ads, and the metaverse. As we look over to the next decade, which company offers the stronger long-term growth story for the next 10 years? Let’s find out.

The Case for Meta Platforms

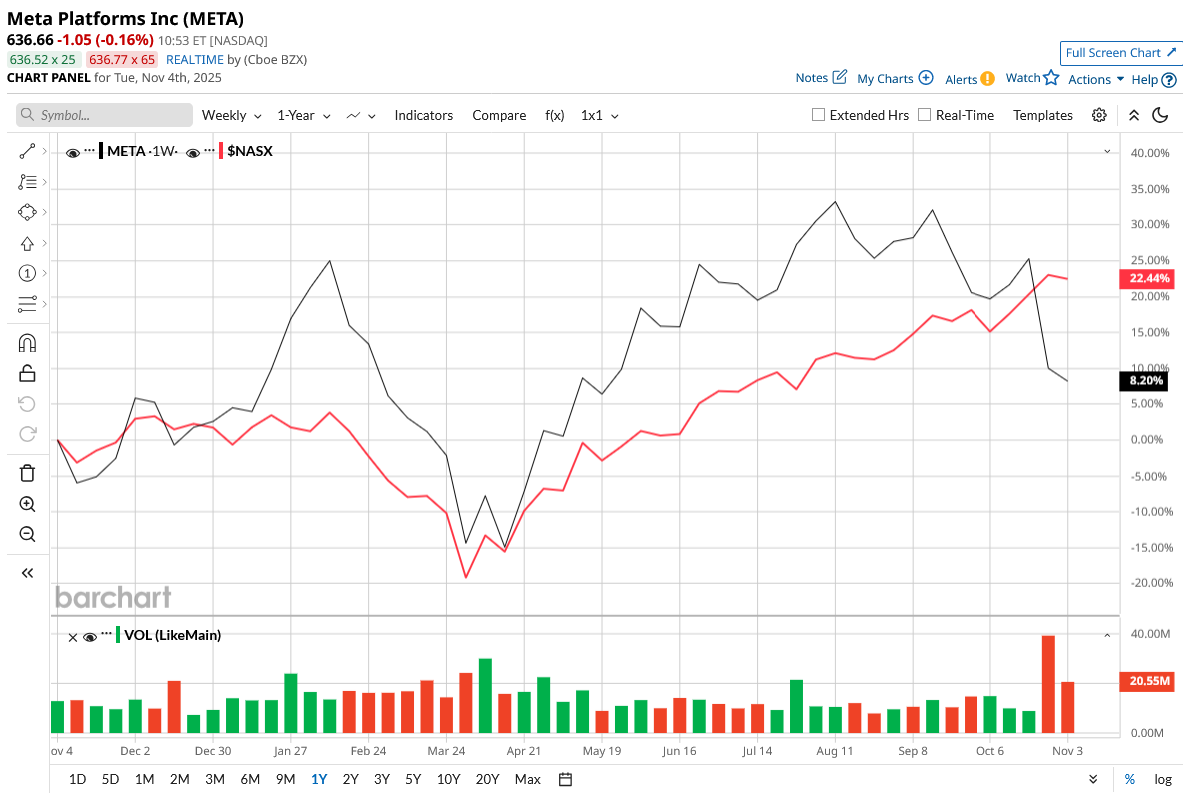

Valued at $1.6 trillion, Meta Platforms (formerly Facebook) is a tech company that builds social media, messaging, and virtual reality products. Its main platforms include Facebook, Instagram, WhatsApp, and Threads, which connect billions of people worldwide. Meta reported its third-quarter earnings on Oct. 29. META stock has gained 8.5% year-to-date (YTD), underperforming the tech-heavy Nasdaq Composite Index’s ($NASX) gain of 22.4%.

Meta's global reach continues to rise at an alarming rate. As of September, more than 3.5 billion individuals used at least one of its social media apps daily. Instagram has surpassed 3 billion monthly active users, cementing its position as one of the world's most popular social media networks. Threads, Meta's newest social platform, continues to impress, with 150 million daily active users and consistent engagement.

In the third quarter, the FoA segment, which comprises all its social media platforms, saw a 26% jump in revenue to $50.8 million. Advertising revenue of $50.1 billion rose 26%, driven by a 14% rise in ad impressions and a 10% rise in average ad prices.

Reality Labs, its metaverse segment’s revenue jumped 74% to $470 million, supported by AI glasses and Quest headset sales. The segment continues to post operating losses, which stood at $4.4 billion in Q3. However, CEO Mark Zuckerberg believes the investment in the metaverse will eventually pay off. Total revenue jumped 26% to $51.2 billion, while adjusted earnings per share rose 20.2% to $7.25. The company continues to invest aggressively in infrastructure, spending $19.4 billion on capital expenditures, primarily for servers, data centers, and network capacity. Free cash flow remained strong at $10.6 billion, and Meta returned value to shareholders through $3.2 billion in stock buybacks and $1.3 billion in dividends. Meta ended the quarter with $44.4 billion in cash and $28.8 billion in debt, a formidable balance sheet to sustain its significant AI and hardware expenditures.

Zuckerberg sees Meta standing at the threshold of what could be the company’s most transformative decade. The path is ambitious, integrating its apps into a unified AI system, expanding computation for the age of superintelligence, and developing products that combine the digital and physical worlds.

What Does Wall Street Say About META Stock?

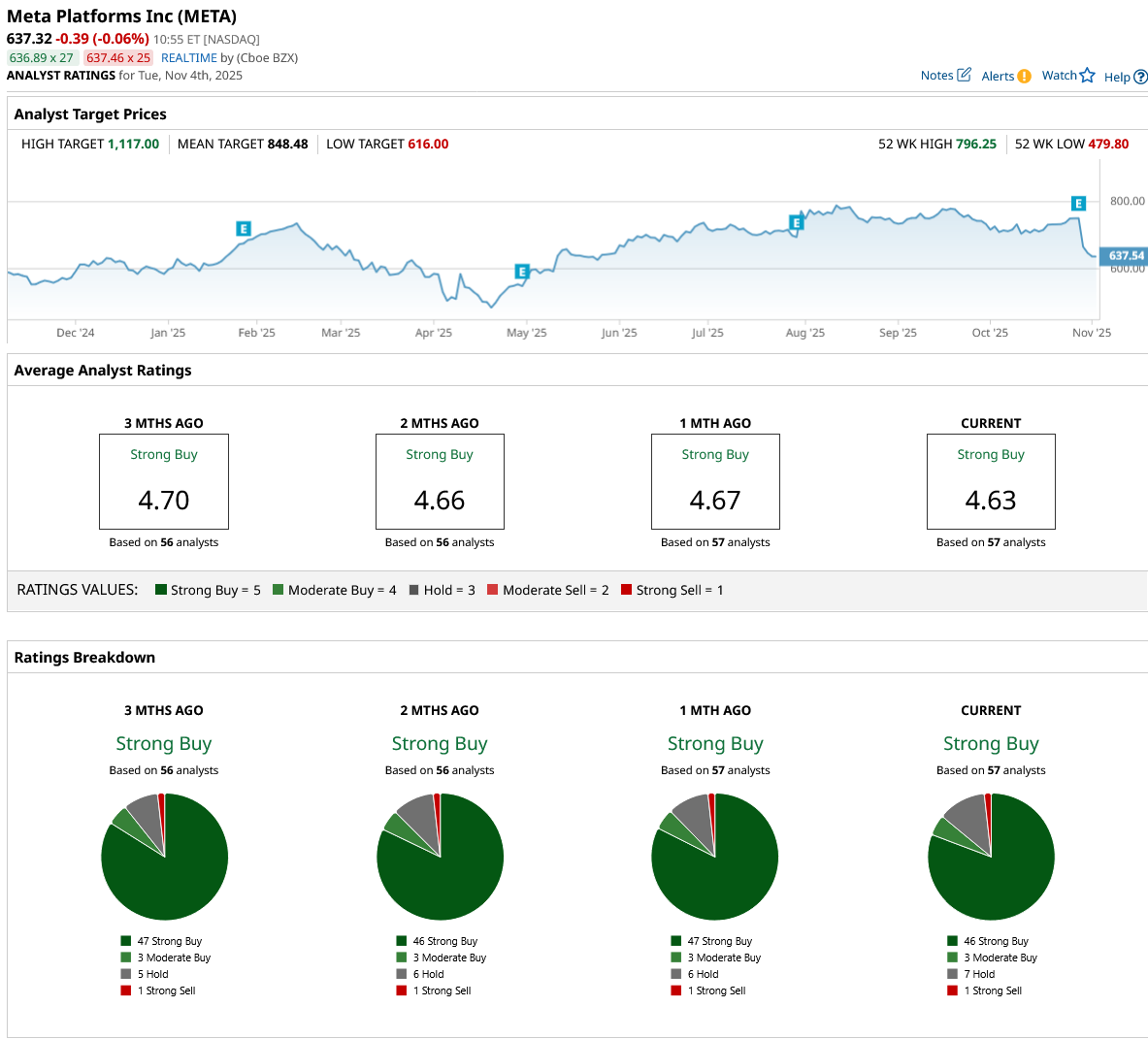

Overall, the consensus for META stock is a “Strong Buy.” Among the 57 analysts covering the company, 46 give it a “Strong Buy” rating, three recommend a “Moderate Buy,” seven suggest holding, and one rates it a “Strong Sell.” The average price target of $848.48 indicates a potential 33.1% upside from current levels. Meanwhile, the high price target of $1,117 implies the stock could surge by as much as 75.2% over the next year.

The Case for Microsoft

Valued at $3.8 trillion, Microsoft is bigger than Meta and has been in the game longer. It creates software, hardware, and cloud services. It is most recognized for legacy products such as Windows, Microsoft 365 (Office), and Azure, its cloud computing platform. Furthermore, it also creates AI tools, developer platforms, and enterprise software for organizations and owns LinkedIn, GitHub, and Xbox.

Microsoft released its first quarter of fiscal 2026 earnings on Oct. 29. MSFT stock has surged 22% YTD.

In the first quarter, Microsoft reported revenue of $77.7 billion, up 17% year-over-year (YoY), with earnings climbing 21%, reaching $4.13. Gross margin came in at 69%, just marginally lower than the previous year due to strong AI-related investments. Capital expenditures totaled $34.9 billion, primarily to build its AI and cloud infrastructure. These investments, mostly in data centers, GPUs, CPUs, and AI engineering expertise, are reshaping Microsoft's cost structure while already producing substantial rewards. Management noted that roughly half of this spending was allocated to short-lived assets such as GPUs and CPUs, with the remainder supporting long-lived data center facilities expected to yield profits for 15 years or more.

A highlight of the quarter was the company’s new definitive agreement with OpenAI. Under the new terms, Microsoft has exclusive Azure rights and revenue sharing through 2030, with an extended model and IP rights until 2032. OpenAI has already contracted an additional $250 billion of Azure services, while Microsoft’s investment in the company has returned roughly 10x.

Unsurprisingly, Microsoft's cloud empire continues to drive its financial engine. Microsoft Cloud revenue reached $49.1 billion, up 25% YoY. Azure and other cloud services climbed by an astonishing 39%, thanks to demand from commercial clients and AI partnerships such as OpenAI. The Intelligent Cloud sector recorded revenue of $30.9 billion, up 27%.

Microsoft’s balance sheet remains among the strongest in the tech industry, with $102 billion in cash, equivalents, and short-term investments. Despite higher capital expenditures, free cash flow increased 33% to $25.7 billion. This enabled the company to repay $10.7 billion to shareholders in dividends and buybacks. Management noted that AI infrastructure spending will increase further, citing historic demand signals and a growing $392 billion commercial RPO, which is up 51% YoY. The company expects its capacity to remain limited through the end of fiscal 2026, given the rapid, worldwide expansion of AI adoption.

What Does Wall Street Say About MSFT Stock?

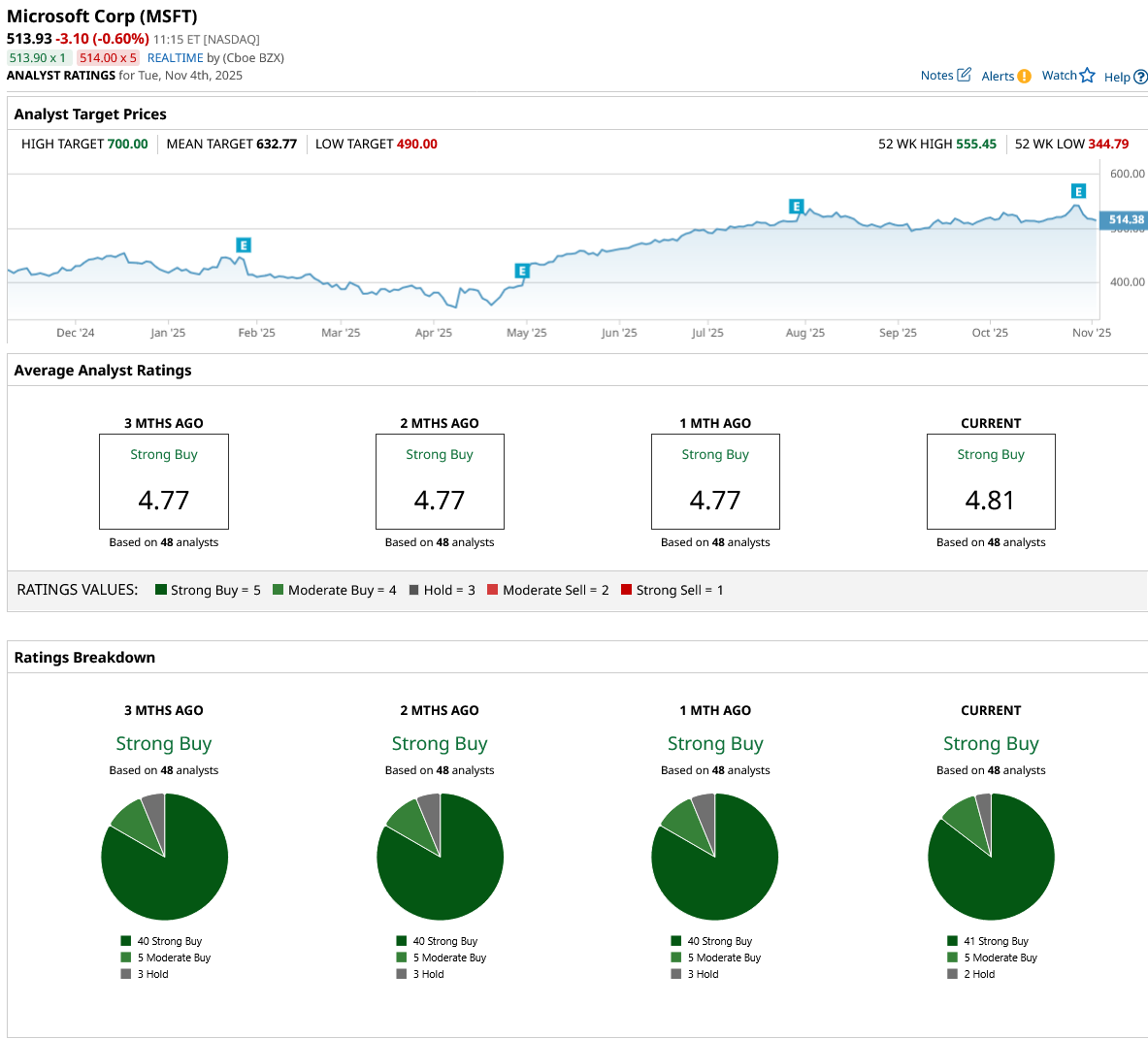

On Wall Street, MSFT stock is a “Strong Buy.” Of the 48 analysts covering the stock, 41 rate it a “Strong Buy,” five rate it a “Moderate Buy,” and two say it is a “Hold.” The average analyst target price of $632.77 suggests the stock has upside potential of 23.1% from current levels. Plus, its high target price of $700 implies that the stock could rise as much as 36.2% from current levels.

META vs. MSFT: Which Is the Better Buy for the Next Decade?

I believe, in the long run, MSFT stock is the stronger buy. While Meta is innovating in AI and the metaverse, Microsoft’s diversified business, spanning cloud computing, productivity software, and AI integration through Azure and OpenAI, gives it a more stable growth foundation. It positions MSFT to outperform over the next decade.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Bitcoin’s Weekly Structure Shows Signs of a Failed Auction. It’s a Warning for the Long-Term Trend.

- Core Scientific Just Got a New Street-High Price Target. Should You Buy CORZ Stock Here?

- Top 100 Stocks to Buy: Two Penny Stocks Moved Up 51 Spots. Should You Buy Either?

- Apple Stock Is Still ‘Expensive’ But This 1 Catalyst Could Change the Game, According to Analysts