Disney (DIS) released its fiscal Q4 2025 earnings yesterday, Nov. 13, following which the stock plunged nearly 8% to fall below its 200-day moving average. The stock is on track to underperform the S&P 500 Index ($SPX) this year—something it did in three of the last four years. In this article, we’ll explore whether 2026 would be any different for the entertainment giant, beginning with a snapshot of its Q4 earnings.

Disney Reported Mixed Earnings

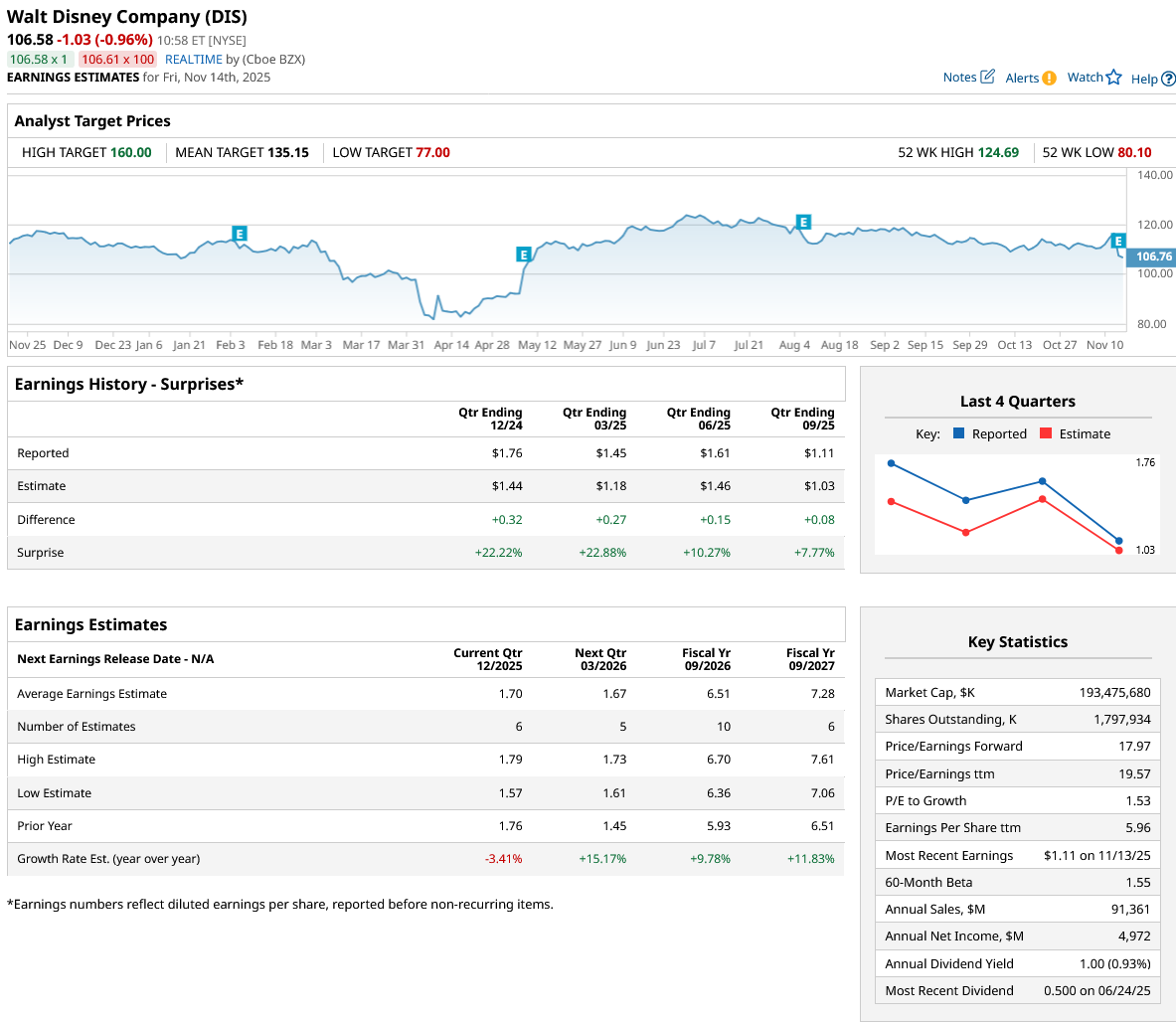

Disney reported a mixed set of numbers for fiscal Q4. Its revenues came in at $22.46 billion, which were slightly lower than the corresponding quarter last year and fell short of the $22.75 billion that analysts were modeling. Its adjusted earnings per share (EPS) also fell 3% to $1.11 but were ahead of Street estimates.

To be sure, Disney faced tougher comparisons in the quarter, as it had a much stronger theatrical slate last year and also benefited from political advertisements ahead of the 2024 U.S. presidential elections. Still, the results fell short of clearing the low bar, and even the dividend and share buyback hike failed to lift sentiments.

Disney Has Been a Story of Three Moving Parts

Disney’s recent earnings show the continuation of the past trend, where the business has been a mix of three parts. On the one hand, we have the Experiences segment, housing its theme parks, which continues to do well. Streaming has also been a success story and generated an operating income of $352 million in Q4 and $1.3 billion in the full fiscal year. To put that in context, before Bob Iger took over as the CEO in late 2022, that business was losing around $4 billion on an annualized basis.

The second moving part of the Disney story has been the Linear TV business, which is in a structural, if not a terminal, decline. While previously there were reports that Disney might consider exiting Linear TV, the company has categorically denied such a possibility, as that business complements its streaming content.

Then we have the movie franchise, which tends to blow hot and cold. Last year was actually excellent for that business with releases like Moana 2 and Inside Out 2—the latter was not only the most successful at the box office in 2024 but was the fourth biggest successful animated movie ever. It was a welcome break for Disney after an underwhelming box office performance in the previous two years. However, the company lost its magic this year as titles like Snow White and Tron: Ares disappointed.

As I have stated multiple times previously, the importance of successful and popular movies cannot be understated and goes way beyond the box office contributions to Disney’s earnings. In-house, quality movies add to Disney’s streaming content and make the offering even more valuable for subscribers. These also increase Disney’s connection with its customer base, which eventually transforms into higher traffic at its theme parks, which are the company’s cash flow engine.

Disney Stock 2026 Forecast: Can Things Get Any Better?

While I have been disappointed with Disney’s price action—as would be other bulls—I remain optimistic about the stock for 2026 and used the post-earnings dip to add more to my existing positions. To begin with, the company has a reasonably strong movie slate with titles like Avatar: Fire and Ash, Toy Story 5, and the live-action Moana set to release in the fiscal year 2026. The company’s parks—both domestic and international—continue to do reasonably well with growth in bookings as well as average spending. While there were concerns about stringent U.S. immigration policies, macroeconomic slowdown, and competition from the opening of Comcast’s (CMCSA) Epic Universe theme park in Florida taking a toll on Disney’s U.S. parks, that segment has held its ground quite well. Disney’s streaming business should also continue its good run in 2026 and beyond as its margins ramp up.

Meanwhile, while Disney has guided for double-digit earnings growth in fiscal year 2026, it would be a back-heavy year for the company as it still faces tough comps in the fiscal first quarter.

DIS Stock Is a Buy despite the Challenges

Disney does face some headwinds, both in the short and long term. In the near term, it needs to sort out the YouTube partnership. Over the medium to long term, Linear TV decline would continue to weigh on Disney’s earnings. The company also needs to do succession planning, as Iger has said that he would step down after his contract expires next year. Finally, for entertainment companies like Disney, artificial intelligence (AI) could be more of a threat than an opportunity, and during the earnings call, the company said that it is working with AI companies to protect its intellectual property (IP).

However, at a forward price-to-earnings multiple of 17.7x, the risk-reward looks favorable for Disney, and I would expect DIS stock to deliver decent double-digit returns in 2026, unless, of course, we see a major fall in broader markets.

On the date of publication, Mohit Oberoi had a position in: DIS . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Joby Aviation’s Military Ambitions Are Taking to the Skies. Should You Buy JOBY Stock Here?

- Where Will the Bleeding End for Bitcoin Bulls? Our Top Chart Strategist Maps Out BTC’s Next Move.

- Cisco Delivered Strong, But Lower Free Cash Flow and FCF Margins - Has CSCO Stock Peaked?

- I’m Old Enough to Remember When a 500-Point-Drop in the Dow Jones Was a Crisis. Now It’s Just a Warning.